Collections and Debt Recovery Templates

★★★★★4.7from 280+ reviews· Trusted by 20M+ businesses

Get paid faster with ready-to-use demand letters, promissory notes, and payment extension agreements for every stage of the collection process.

WordEditable onlinePDF51+ collections and debt recovery templates

Other Finance & Accounting categories

Collection notices and demand letters

Debt agreements and extensions

More collections and debt recovery templates

250K+Clients

20M+Free users

20+Years

190+Countries

10,000+Law firms

50M+Downloads

Trusted across review platforms

- Capterra★★★★☆4.649 reviews

- G2★★★★☆4.713 reviews

- GetApp★★★★☆4.649 reviews

- Google Play★★★★☆4.6179 ratings

- Google Reviews★★★★☆4.567 reviews

Frequently asked questions

What is the difference between debt collection and debt recovery?

Debt collection typically refers to the ongoing process of pursuing overdue payments — sending notices, making calls, and setting up payment plans. Debt recovery usually implies a more formal effort to reclaim money after normal collection attempts have failed, often involving legal action or a third-party agency. In practice the terms are used interchangeably in most business contexts.

When should I send a formal demand letter instead of a collection notice?

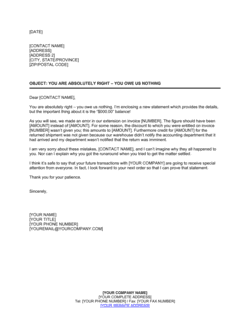

Send a demand letter when you have already sent one or more collection notices without result and are genuinely prepared to escalate — either through legal proceedings or by engaging a collection agency. A demand letter signals that the goodwill phase is over. Sending it too early can damage a customer relationship unnecessarily; sending it too late wastes time and may allow a limitation period to lapse.

Is a promissory note legally binding?

Yes. A signed promissory note is generally enforceable as a written promise to repay a specific sum under agreed terms. Courts in most jurisdictions treat it as sufficient evidence of a debt obligation. To maximize enforceability, the note should identify both parties, state the principal amount, set a repayment date or schedule, and be signed by the borrower. Consider having a lawyer review notes involving large sums or unusual terms.

Can I charge interest on an overdue invoice without a written agreement?

In many jurisdictions you can charge statutory late-payment interest without a prior written agreement, but the rate is often lower than what a contract would permit. Having a written credit policy or invoice terms that state your interest rate gives you a stronger contractual basis and removes ambiguity. Check applicable law for the statutory rate in your jurisdiction.

What happens if a debtor ignores all collection notices?

If a debtor fails to respond to notices and demand letters, your options typically include referring the account to a collection agency, filing a claim in small claims court (for amounts within the relevant limit), commencing a civil lawsuit, or — if you hold a promissory note — enforcing the note as a debt instrument. Document every attempt made before escalating, as that record strengthens your legal position.

Does an agreement to compromise debt release the debtor from the full balance?

Yes, a properly executed compromise agreement releases the remaining balance once the agreed reduced amount is paid. Before signing, confirm that you prefer a partial recovery now over pursuing the full amount through legal action. Note that forgiven debt may have tax implications for both parties — consult a tax adviser if the forgiven amount is material.

How long do I have to collect a business debt?

Limitation periods vary by jurisdiction and by the type of debt — typically between two and six years from the date payment was due, though some jurisdictions allow longer. An acknowledgment of debt signed by the debtor can reset the clock. If you are approaching a limitation period, take formal legal action or obtain a written acknowledgment before it lapses.

What is a subordination agreement in the context of debt?

A subordination agreement changes the priority order in which creditors are repaid. A subordinated creditor agrees to be paid after a senior creditor — typically a bank or primary lender — in the event of default or insolvency. Lenders often require subordination from secondary creditors as a condition of extending credit.

Collections and Debt Recovery vs. related documents

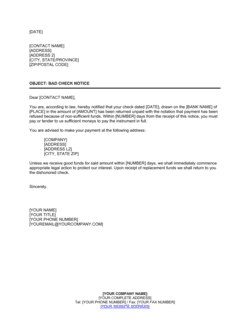

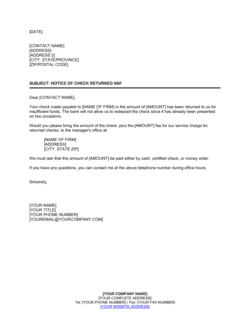

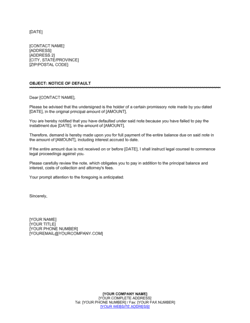

A collection letter is typically part of a series of escalating notices reminding a debtor that a balance is overdue — tone escalates with each round. A demand letter is a single, formal final notice asserting a legal right to payment and warning that legal action follows. Use collection letters early in the cycle; use a demand letter when you are genuinely prepared to sue or refer the account to a collection agency.

A promissory note is a short, unconditional written promise by the borrower to repay a specific sum. A loan agreement is a fuller bilateral contract that covers both parties' obligations, covenants, representations, and events of default. Promissory notes suit straightforward loans between known parties; loan agreements are better for complex or high-value lending with multiple conditions.

An extension agreement keeps the full debt intact but gives the debtor more time or a restructured payment schedule. A compromise agreement settles the debt for a reduced amount in exchange for prompt payment. Use extension when the debtor is willing but temporarily unable to pay; use compromise when full collection is unlikely and a partial recovery is preferable to a legal dispute.

A credit application is the form a customer completes to request credit — it captures the information you need to decide. A credit policy is an internal document that governs how your business evaluates those applications, sets limits, and handles delinquencies. Both are necessary: the policy drives consistency; the application generates the data.

Key clauses every Collections and Debt Recovery contains

Most collections and debt recovery documents share a core set of clauses — the specifics vary by document type, but these elements appear across the category.

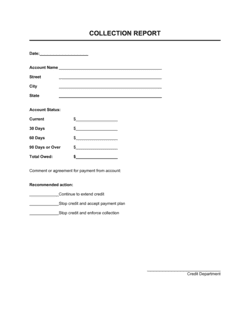

- Identification of parties and debt. Names the creditor, the debtor, and states the amount owed and the origin of the obligation.

- Payment terms. Specifies when payment is due, whether in a lump sum or installments, and acceptable payment methods.

- Interest and late fees. States the rate charged on overdue balances and how fees accrue if payment is delayed.

- Notice and cure period. Gives the debtor a defined window — often 10 to 30 days — to pay or respond before escalation.

- Acceleration clause. Makes the full outstanding balance immediately due if the debtor misses a scheduled payment.

- Default and remedies. Defines what constitutes default and what actions the creditor may take — including legal proceedings or referral to a collection agency.

- Acknowledgment of debt. A statement signed by the debtor confirming the debt exists and the amount is correct, which resets limitation periods in many jurisdictions.

- Governing law and jurisdiction. Names the jurisdiction whose laws govern the agreement and where disputes will be resolved.

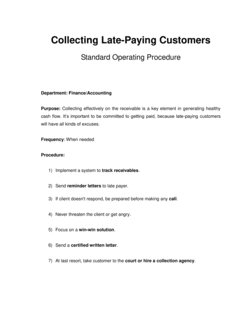

How to write a collections or debt recovery document

Effective collections documents follow a clear escalation logic — each step produces a written record and moves the matter closer to resolution.

1

Establish your collections policy first

Document the internal rules — when notices go out, who approves escalation, and when accounts are referred externally — before individual cases arise.

2

Identify the debtor and verify the balance

Confirm the full legal name of the debtor, the exact amount owed, the invoice or agreement reference, and the original due date.

3

Choose the right document for the stage

Match the document to where the account stands: early notice for a new delinquency, demand letter for a final warning, extension agreement if the debtor is negotiating.

4

State the debt clearly and specifically

Identify the amount, the date it became due, and any interest or fees accrued — vague figures invite disputes.

5

Set a firm deadline

Give the debtor a specific date by which payment or a response is expected — open-ended deadlines are routinely ignored.

6

Describe the consequences of non-payment

State plainly what happens next: credit reporting, referral to collections, or legal action — without threatening anything you aren't prepared to follow through on.

7

Send via traceable delivery and keep copies

Use certified mail, courier, or a documented email trail so you can prove the notice was sent and received.

8

Document every communication

Log every letter, call, and response in the account file so the full history is available if the matter goes to court or a collection agency.

At a glance

- What it is

- Collections and debt recovery documents are the formal letters, agreements, and notices that businesses use to recover money owed to them — from a first reminder through final legal demand. They establish a documented paper trail that protects your right to collect and strengthens your position if the matter escalates to legal action.

- When you need one

- Any time a customer or counterparty has an overdue balance, disputes a charge, or needs a formal payment arrangement, a written collections document puts your claim on record and signals that you intend to enforce it.

Which Collections and Debt Recovery do I need?

The right document depends on where the debt sits in the collection cycle and what outcome you're pursuing — formal notice, a payment arrangement, a written obligation, or a final demand.

Your situation

Recommended template

Setting internal rules for how your team pursues overdue accounts

Establishes consistent procedures so every overdue account is handled the same way.Giving a small business debtor advance notice before collections begin

Satisfies notice obligations and gives the debtor a final chance to pay voluntarily.Warning a delinquent customer that collections start in 10 days

Creates a clear deadline and documents the final pre-collection warning.A customer can't pay in full and needs a structured repayment plan

Formalizes new payment terms so both parties have a binding written record.Both parties agree to settle a debt for less than the full amount

Documents the negotiated settlement and releases the balance upon payment.Issuing a formal demand on an unpaid promissory note

Formal demand is typically required before legal action on a note can proceed.Creating a written loan obligation between a business and a borrower

A signed promissory note is the foundational document evidencing the debt.A borrower requests extra time to repay an existing promissory note

Documents the extension request formally so the lender can respond in writing.Glossary

- Creditor

- The party owed money under a debt obligation.

- Debtor

- The party that owes money and is obligated to repay it.

- Promissory note

- A written, unconditional promise by one party to pay a specific sum to another by a set date or on demand.

- Acceleration clause

- A contract provision that makes the entire outstanding balance immediately due if the debtor misses a scheduled payment.

- Default

- Failure to meet the terms of a debt obligation — most commonly, failure to make a payment when due.

- Limitation period

- The maximum time a creditor has to take legal action to recover a debt before the claim is barred by law.

- Debt compromise

- An agreement to settle a debt for less than the full amount owed, typically in exchange for immediate payment.

- Subordination

- An arrangement where one creditor agrees to be repaid only after another, higher-priority creditor has been paid in full.

- Acknowledgment of debt

- A signed statement by the debtor confirming that a debt exists and the amount is correct; often resets the limitation period.

- Delinquent account

- An account where payment is overdue beyond the agreed terms.

- Credit note

- A document issued by a seller reducing the amount a buyer owes, typically due to a return, error, or adjustment.

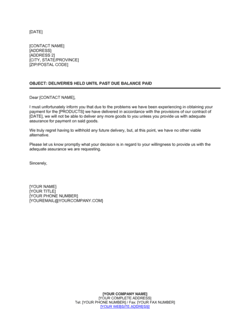

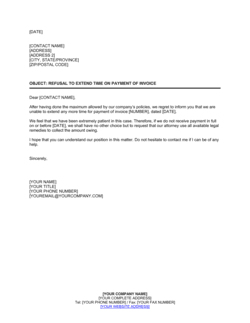

- Demand letter

- A formal final notice requiring payment by a specific date and warning of legal or collection action if unpaid.

What is a collections and debt recovery document?

A collections and debt recovery document is any letter, notice, agreement, or policy a business uses to formally pursue money it is owed — from an initial overdue reminder through a final legal demand. These documents serve two purposes simultaneously: they give the debtor a structured opportunity to pay or negotiate, and they create the written record a creditor needs if the matter escalates to a collection agency, small claims court, or civil litigation.

The category spans a wide range of document types. Collection notices alert a debtor that an account is overdue and state the consequences of continued non-payment. Demand letters are formal final notices issued when earlier reminders have been ignored. Promissory notes establish the debt obligation itself — a signed written promise to repay a specific sum. Debt agreements (extensions, compromises, and subordinations) restructure what is owed or how it will be paid when the original terms can no longer be met. Credit management documents — applications, policies, memos, and limit notices — sit upstream of collections and help businesses avoid bad debt in the first place.

When you need a collections or debt recovery document

The moment a customer misses a payment date, a business faces a choice: follow up informally and hope for the best, or issue a formal written notice and start building a paper trail. Informal follow-up is faster; formal documentation is safer. Most businesses that handle significant receivables need both a written collections policy and a library of ready-to-use notices and agreements.

Common triggers:

- A customer invoice is 30, 60, or 90 days past due with no payment received

- A borrower misses a scheduled payment on a promissory note

- A debtor requests more time to pay and you need to formalize new terms

- You are considering settling a debt for less than the full amount

- A new customer applies for credit terms and you need to evaluate their eligibility

- You need to notify a debtor that their account is being referred to a collection agency

- A lender requires existing creditors to subordinate their claims before extending new credit

- You want to establish a consistent internal policy so every overdue account is handled the same way

Skipping formal documentation rarely saves time — it loses it. Without a written record of notices sent, deadlines given, and agreements reached, creditors find it difficult to enforce their rights in court, negotiate effectively with collection agencies, or prove that a debtor was given fair opportunity to resolve the balance. A complete set of collections templates removes the friction from every stage of the process and keeps every communication legally sound.

Award-winning platform

- Great Place to Work 2025

- BIG Award — Product of the Year 2025

- Smartest Companies 2025

- Global 100 Excellence 2026

- Best of the Best 2025