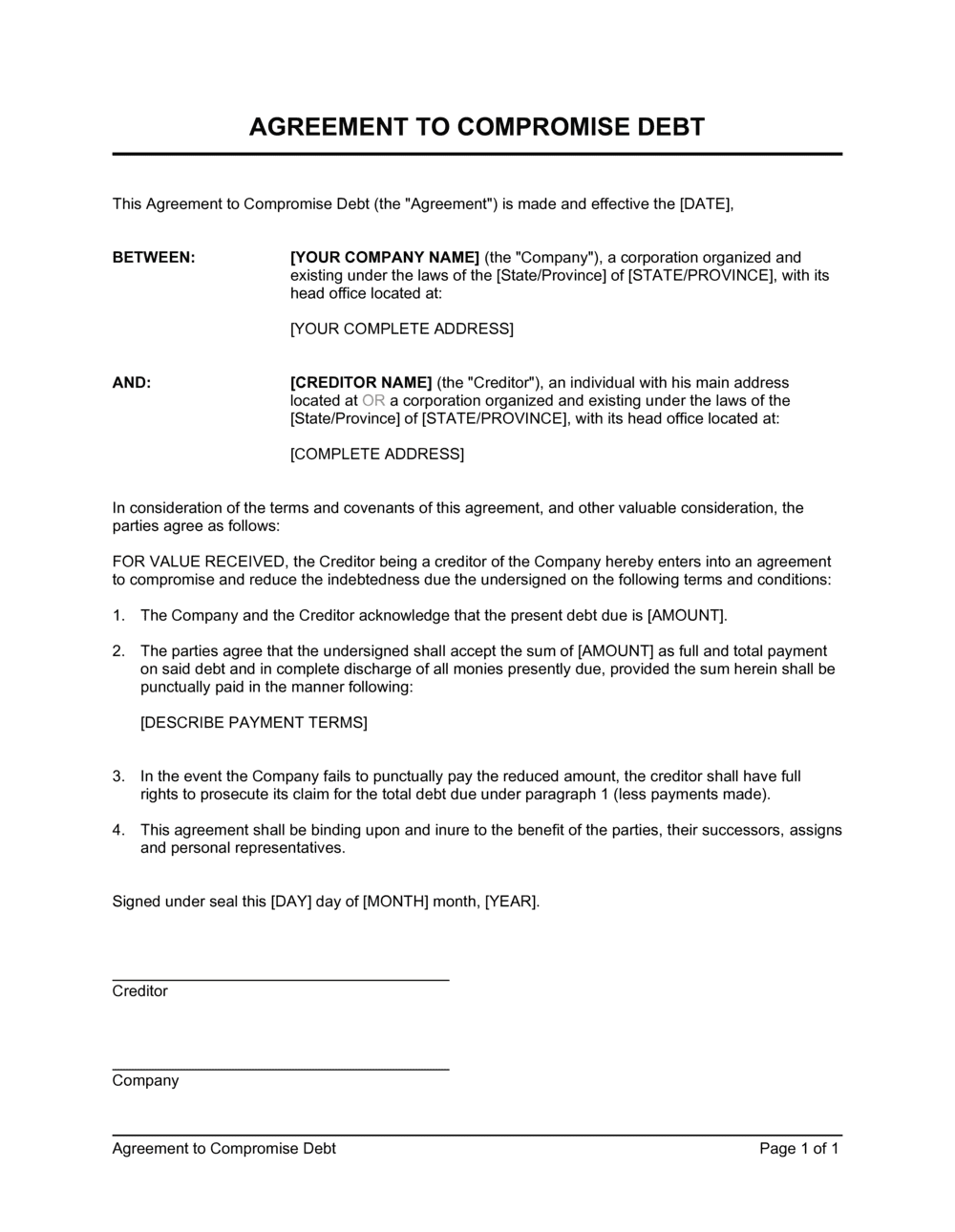

- Compromise of Debt

- A mutual agreement in which a creditor accepts less than the full amount owed as complete satisfaction of the debt, extinguishing the remaining balance.

- Creditor

- The party to whom money is owed — a lender, supplier, or service provider holding an outstanding receivable.

- Debtor

- The party who owes the debt and is seeking to settle it for less than the full outstanding amount.

- Accord and Satisfaction

- A common-law doctrine under which a disputed or unliquidated debt is discharged when the creditor accepts a lesser amount offered in full settlement.

- Mutual Release

- A provision in which both parties agree to release each other from all claims, obligations, and liabilities arising from the original debt after the compromise payment is made.

- Deficiency Balance

- The portion of the original debt that remains after a partial payment — extinguished by the agreement once the compromise amount is paid in full.

- Consideration

- Something of value exchanged between parties to make a contract binding — in a debt compromise, the creditor's release of the remaining balance is the consideration for the debtor's agreed payment.

- Default Clause

- A provision specifying what constitutes a missed or late payment under the compromise agreement and what remedies the creditor retains if the debtor defaults.

- Novation

- The substitution of a new obligation for an existing one — a compromise agreement creates a novation when it replaces the original debt terms with the new settlement terms.

- Forbearance

- A creditor's agreement to refrain from taking legal action to collect a debt for a defined period, often a condition the debtor must meet through timely payments under the compromise.

- Deed of Release

- A formal document, sometimes separate from the compromise agreement, that evidences the creditor's surrender of all remaining claims once the settlement amount has been paid.