Business Insurance Templates

★★★★★4.7from 280+ reviews· Trusted by 20M+ businesses

Plan coverage, file claims, and manage employee benefits with ready-to-use insurance documents.

WordEditable onlinePDF10+ business insurance templates

Other Finance & Accounting categories

Employee benefits and coverage

Liability and executive coverage

250K+Clients

20M+Free users

20+Years

190+Countries

10,000+Law firms

50M+Downloads

Trusted across review platforms

- Capterra★★★★☆4.649 reviews

- G2★★★★☆4.713 reviews

- GetApp★★★★☆4.649 reviews

- Google Play★★★★☆4.6179 ratings

- Google Reviews★★★★☆4.567 reviews

Frequently asked questions

What types of insurance does a small business typically need?

Most small businesses need at minimum: general liability insurance, commercial property insurance, and workers' compensation if they have employees. Professional services firms also typically carry professional liability (errors and omissions) insurance. Businesses with company vehicles need commercial auto coverage. The right mix depends on industry, location, and contractual requirements from clients or landlords.

Is a business insurance checklist legally required?

A checklist itself is not a legal requirement, but it is a practical tool that helps ensure you meet the coverage obligations that are required — by lease agreements, client contracts, lenders, or state law. Using a structured checklist reduces the risk of discovering a gap only after an incident has occurred.

How soon after an incident do I need to file a notice of insurance claim?

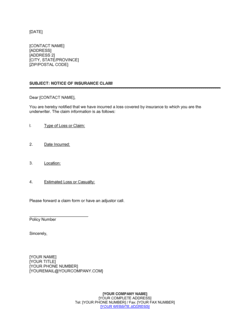

Most commercial insurance policies require notice "as soon as practicable" or within a specific number of days — commonly 30 to 60 days of the event. Review your policy language carefully. Filing late can give the insurer grounds to deny the claim, even when the loss itself is clearly covered.

Can a business use a template insurance agreement instead of the insurer's policy form?

Standard insurance policies are issued on the insurer's own forms, which are filed with and approved by state regulators. A template insurance agreement is best used as a supplemental or summary document — for example, between a business and a vendor who is providing coverage, or to memorialize coverage terms agreed upon outside a standard form. For primary coverage, always work from your insurer's issued policy.

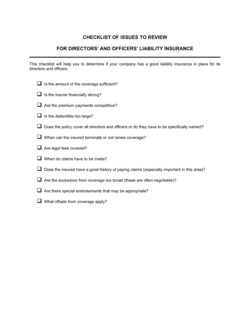

What is directors and officers (D&O) insurance and when does a business need it?

D&O insurance protects company directors and officers from personal financial liability when they are sued for alleged wrongful acts in their leadership roles — decisions that harm shareholders, creditors, employees, or regulators. It is typically needed when a company has outside investors, an independent board, significant debt, or operates in a regulated industry. The D&O checklist helps boards evaluate their specific exposure areas.

How do I add a landlord as an additional insured on my liability policy?

Most commercial leases require tenants to name the landlord as an additional insured on their general liability policy. To do this, contact your insurer or broker with the landlord's full legal name and address and request an additional insured endorsement. Use a formal written request letter — such as the template in this folder — to document the request and create a paper trail for both parties.

What is key employee life insurance and does my business need it?

Key employee life insurance — also called key-person insurance — is a policy the business owns on a critical employee or founder. If that person dies, the business receives the payout to fund recruitment, offset revenue loss, or satisfy lenders. It is most relevant for small businesses or startups where one or two individuals generate a disproportionate share of revenue or relationships.

How should a business communicate a change in health benefits to employees?

Benefits changes should be communicated in writing, with enough advance notice for employees to adjust their plans — 30 days is a common minimum, though open enrollment windows and plan terms may require longer. A formal written announcement that states exactly what is changing, the effective date, and what action (if any) employees need to take reduces confusion and protects the business if an employee later claims they were not informed.

Business Insurance vs. related documents

An insurance agreement is a formal contract between the insured and the insurer defining policy terms, coverage limits, and exclusions. An insurance certificate (also called a certificate of insurance or COI) is a one-page summary document issued to a third party as proof that coverage exists. You sign an insurance agreement with your insurer; you hand a certificate to a client or landlord. Both may be needed in the same business relationship.

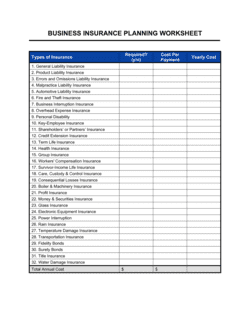

A checklist confirms whether required policy types are in place — it's a pass/fail audit tool. A planning worksheet is used earlier in the process to compare coverage options, record premium quotes, and map coverage gaps. Use the worksheet when selecting or renewing policies; use the checklist to verify the result afterward.

A notice of insurance claim is the first document you file after an insured event — it alerts the insurer that a claim is coming. A proof of loss is the formal, sworn statement submitted later that quantifies the actual loss and supports the payment request. Insurers typically require the notice within days of an incident; proof of loss deadlines are longer but strictly enforced.

General liability insurance covers bodily injury, property damage, and advertising injury claims brought by third parties. Directors and officers (D&O) insurance covers personal liability claims against company leadership for alleged wrongful acts in their management role — decisions, omissions, and breaches of duty. Most businesses need both; the D&O checklist helps evaluate the latter independently.

Key clauses every Business Insurance contains

Business insurance documents — agreements, claim notices, and coverage requests — share a set of core elements that determine their legal and administrative effectiveness.

- Named insured and additional insureds. Identifies every party whose interests the policy protects — omitting a party from this list means they are not covered.

- Coverage type and policy number. Specifies the exact insurance product (general liability, D&O, key-person life, etc.) and the insurer's policy reference.

- Coverage limits and deductibles. States the maximum the insurer will pay per occurrence and in aggregate, and the amount the insured absorbs first.

- Effective dates. Defines when coverage starts and ends; gaps between policies can leave a business exposed for events that occur in between.

- Exclusions. Lists events or conditions the policy does not cover — understanding exclusions prevents claim denials.

- Notice requirements. Specifies the time window and format in which the insured must report an incident to the insurer; missing deadlines can void a claim.

- Premium and payment terms. States the cost of coverage and the schedule for payments; lapsed premium is the most common reason coverage is cancelled.

- Subrogation clause. Allows the insurer to pursue a third party that caused the insured's loss after the insurer has paid the claim.

How to build a business insurance plan

Selecting and documenting business insurance coverage is a repeatable process — here are the steps that keep most businesses properly protected.

1

Inventory your risks

List the assets, people, liabilities, and revenue streams your business depends on — each category points to a specific coverage need.

2

Identify required coverage

Check lease agreements, client contracts, lender requirements, and local regulations to determine which policies are mandatory, not optional.

3

Use a planning worksheet to compare policies

Record coverage types, limits, deductibles, and annual premiums side by side before committing to any insurer.

4

Run a coverage checklist before binding

Confirm that general liability, property, workers' compensation, professional liability, and any industry-specific policies are all addressed.

5

Execute an insurance agreement

Sign the formal policy document with your insurer and retain a copy alongside a summary of all active policies and their renewal dates.

6

Set up employee benefit enrollment

Issue benefit enrollment forms to new hires and communicate changes to existing staff using a formal benefits change announcement.

7

Document incidents and file claims promptly

Use a notice of insurance claim as soon as an insured event occurs, then follow the claim checklist to gather all required supporting documentation.

8

Review coverage annually

Re-run the checklist each year — revenue growth, new contracts, new employees, and acquired assets all change your coverage needs.

At a glance

- What it is

- Business insurance templates are pre-structured documents that help companies plan, request, administer, and document commercial insurance coverage. They cover everything from initial planning worksheets and coverage checklists to formal claim notices and employee benefit enrollment forms.

- When you need one

- Anytime a business is selecting new coverage, onboarding an employee with benefit eligibility, filing a claim, or communicating an insurance change to staff, a standardized template keeps the process accurate and defensible.

Which Business Insurance do I need?

The right template depends on where you are in the insurance lifecycle — planning coverage, administering employee benefits, or responding to a claim event. Match your situation below.

Your situation

Recommended template

Starting to evaluate which business insurance policies you need

Provides a structured overview of policy types and coverage considerations for any business.Building a coverage plan and comparing policy options systematically

A fillable worksheet that organizes coverage categories, limits, and costs side by side.Conducting a quick audit of all active business insurance policies

A line-by-line checklist confirming required coverage types are in place and current.An incident occurred and you need to notify your insurer formally

Documents the claim event with the details insurers require to open a file.Preparing all documentation before submitting a full insurance claim

Ensures nothing is missing before submission, reducing back-and-forth with the insurer.Reviewing coverage needs for board members and senior executives

Covers D&O-specific exposure areas unique to directors and officers liability.A new employee is starting and needs benefits coverage immediately

Formally requests same-day or accelerated enrollment before the standard waiting period.Your landlord requires to be named on your liability policy

Addresses the landlord's additional insured request in writing with all required details.Glossary

- Named insured

- The person or entity specifically listed on the insurance policy as the primary covered party.

- Additional insured

- A third party added to someone else's insurance policy, giving them limited coverage under that policy.

- Premium

- The amount a business pays — monthly or annually — to maintain an insurance policy.

- Deductible

- The amount the insured must pay out of pocket before the insurance company begins paying a claim.

- Coverage limit

- The maximum dollar amount an insurer will pay for a covered loss, either per occurrence or in total over the policy period.

- Exclusion

- A specific condition, event, or type of loss that the insurance policy does not cover.

- Endorsement

- A written amendment to an insurance policy that adds, removes, or modifies coverage terms.

- Subrogation

- The insurer's right to pursue a third party that caused a loss after the insurer has paid the insured's claim.

- Proof of loss

- A formal, sworn statement submitted to an insurer that documents the details and dollar amount of a claimed loss.

- Occurrence policy

- A policy that covers events that occur during the policy period, regardless of when the claim is filed.

- Claims-made policy

- A policy that covers claims filed during the policy period, regardless of when the underlying event occurred.

- Key-person insurance

- Life or disability insurance owned by a business on a critical employee, with the business as beneficiary.

What is a business insurance template?

A business insurance template is a pre-structured document that helps a company plan, request, administer, or respond to commercial insurance coverage. Templates in this category span the full insurance lifecycle: planning worksheets that map coverage needs before a policy is selected, checklists that audit existing coverage, formal agreements that document policy terms, claim notices that alert insurers to a loss event, and employee-facing forms that handle benefit enrollment and benefit changes.

Business insurance itself is the collection of policies a company carries to transfer financial risk — from property damage and liability claims to employee injury and executive wrongdoing — to an insurance carrier in exchange for a regular premium. The specific policies a business needs depend on its industry, size, assets, workforce, and contractual obligations. Most businesses carry at minimum general liability and property insurance; many also need workers' compensation, professional liability, directors and officers (D&O), or key-person life insurance.

Having the right documents does not replace having the right policies, but it makes the entire process more defensible. A written claim notice filed on time preserves your right to collect; a properly completed planning worksheet ensures you didn't overlook a coverage gap; a formal enrollment request for a new employee ensures they are covered from their first day.

When you need a business insurance template

Any time your business is making a decision about coverage — starting, changing, or claiming — a standardized template keeps the process accurate and creates a paper trail. Common triggers:

- A startup founder is choosing which commercial policies to purchase before signing a lease or taking on clients

- A business owner receives a rate increase from their insurer and needs to communicate it internally or respond formally

- An employee is hired and needs immediate enrollment in the company health or life insurance plan

- A landlord requires the tenant to name them as an additional insured on the tenant's liability policy

- An incident occurs on company premises and the business must notify the insurer within the policy's required window

- A company's board is assessing whether existing D&O coverage is adequate for new investors or a funding round

- HR is communicating an open-enrollment change or benefits reduction to all employees

- A business planning to enter the insurance industry needs a formal business plan structure

Skipping proper documentation is rarely noticed until something goes wrong — and at that point the cost is high. A missed claim notice deadline can void an otherwise valid claim. An undocumented coverage gap discovered after a loss leaves the business holding the full financial exposure. The templates in this folder exist to close those gaps before they become problems.

Award-winning platform

- Great Place to Work 2025

- BIG Award — Product of the Year 2025

- Smartest Companies 2025

- Global 100 Excellence 2026

- Best of the Best 2025