- Creditor

- The party owed money — the business or individual who issued the original invoice or extended credit.

- Debtor

- The party who owes the outstanding amount and to whom the collection letter is addressed.

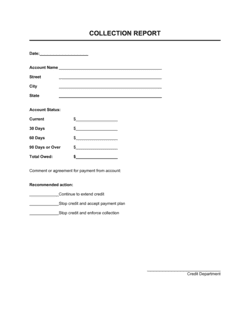

- Outstanding Balance

- The total unpaid amount owed as of the date of the letter, including any principal, accrued interest, and applicable fees.

- Accrued Interest

- Interest that has accumulated on an unpaid balance from the original due date to the date of the letter, calculated at the contractually or legally specified rate.

- Net 30 / Net 60

- Payment terms stating that the full invoice amount is due 30 or 60 days after the invoice date — the starting reference point for calculating how overdue a balance is.

- Certified Mail

- A postal service option that provides a tracked delivery receipt and proof of delivery, creating a documented record that the debtor received the letter.

- Charge-Off

- An accounting action where a creditor writes an uncollectible debt off its books as a loss — does not eliminate the legal obligation but signals the debt has been deemed unlikely to be recovered internally.

- Debt Validation

- Under the US Fair Debt Collection Practices Act, a debtor's right to request written verification of the debt within 30 days of receiving an initial collection notice from a third-party collector.

- Statute of Limitations

- The maximum period after which a creditor can no longer sue to collect a debt — varies by debt type and jurisdiction, typically ranging from 3 to 10 years.

- Collection Agency

- A third-party company engaged to recover debts on a creditor's behalf, typically in exchange for a percentage of the recovered amount ranging from 25% to 50%.

- Payment in Full

- Remittance of the entire outstanding balance — principal, interest, and fees — in a single transaction, satisfying the debt completely.

- Default

- The failure to pay a debt when it becomes due, triggering the remedies specified in the original agreement or applicable law.