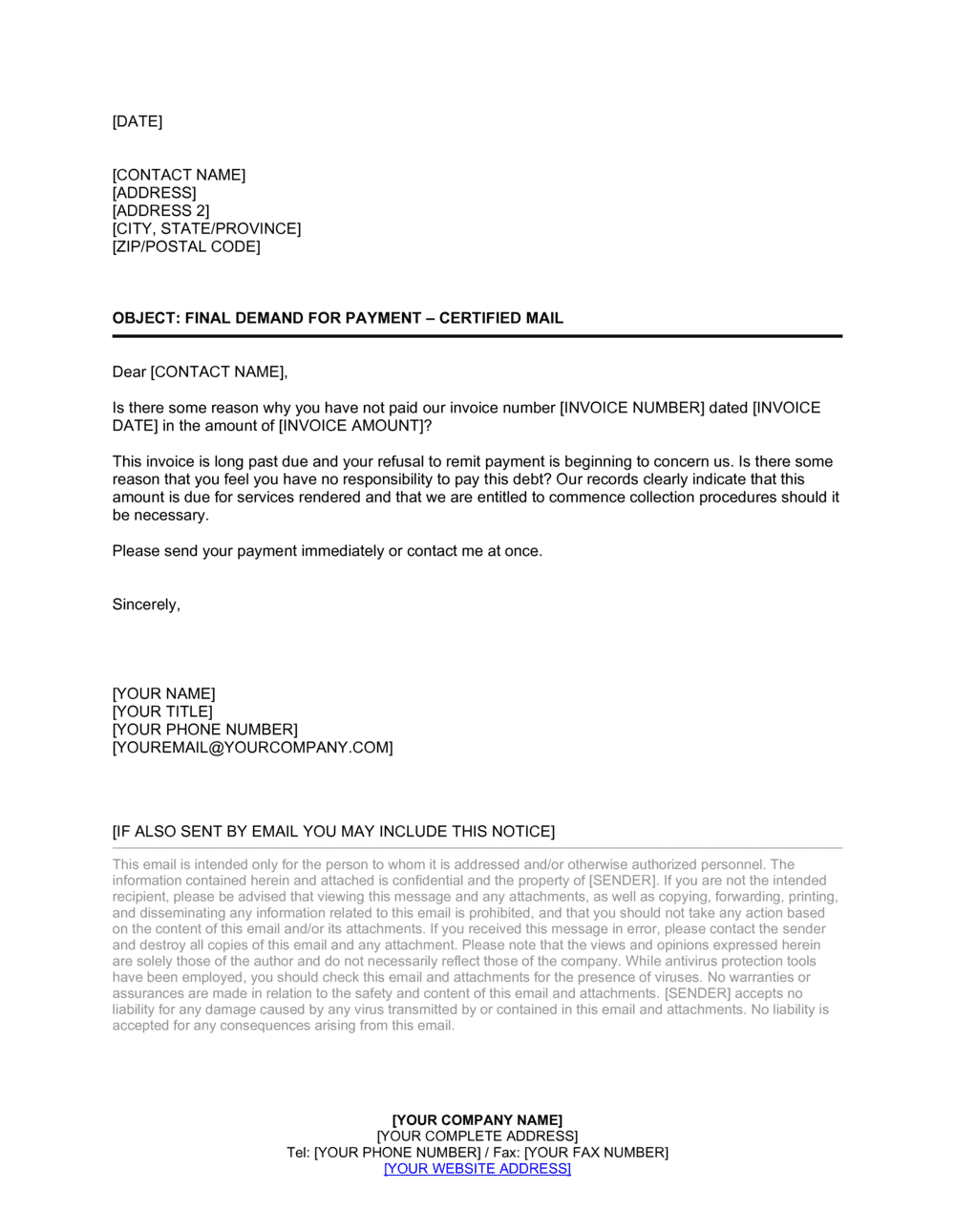

What is a Final Demand For Payment Letter?

A Final Demand For Payment Letter is a formal pre-litigation notice sent by a creditor to a debtor who has failed to pay one or more outstanding invoices despite prior invoices and follow-up reminders. It identifies both parties, references the specific invoices in default, states the exact total amount owed — including any accrued interest or late fees — and sets a firm deadline, typically 7 to 14 days, for payment in full. If the debtor does not pay or dispute the amount in writing within that window, the letter puts them on explicit notice that the creditor will proceed with legal action, small claims filing, or referral to a third-party collections agency without further notice.

Unlike a routine payment reminder, a final demand letter is a legally significant document. Courts in most jurisdictions treat it as evidence that the creditor gave the debtor a last reasonable opportunity to cure the default before initiating formal proceedings, which strengthens the creditor's position when seeking court costs and, where applicable, attorney's fees.

Why You Need This Document

Attempting to collect an overdue debt without a properly documented final demand exposes you to procedural setbacks at every stage of escalation. Small claims courts routinely ask whether the plaintiff sent a prior written demand; arriving without one weakens your case before you speak. Civil litigation attorneys charge to send the demand themselves if you haven't — adding cost and delay to a process you could have started weeks earlier. Without a trackable, signed, dated letter citing specific invoices and a firm deadline, the debtor can credibly claim ambiguity about what was owed, when it was due, and whether they were ever formally put on notice.

A well-structured final demand letter resolves all three problems simultaneously: it creates a paper trail, establishes the precise amount in dispute, starts a documented cure period running, and signals to the debtor — often effectively — that you are prepared to follow through. This template gives you a professionally formatted, jurisdiction-aware document you can complete in under 30 minutes and send by both email and certified mail the same day.