1

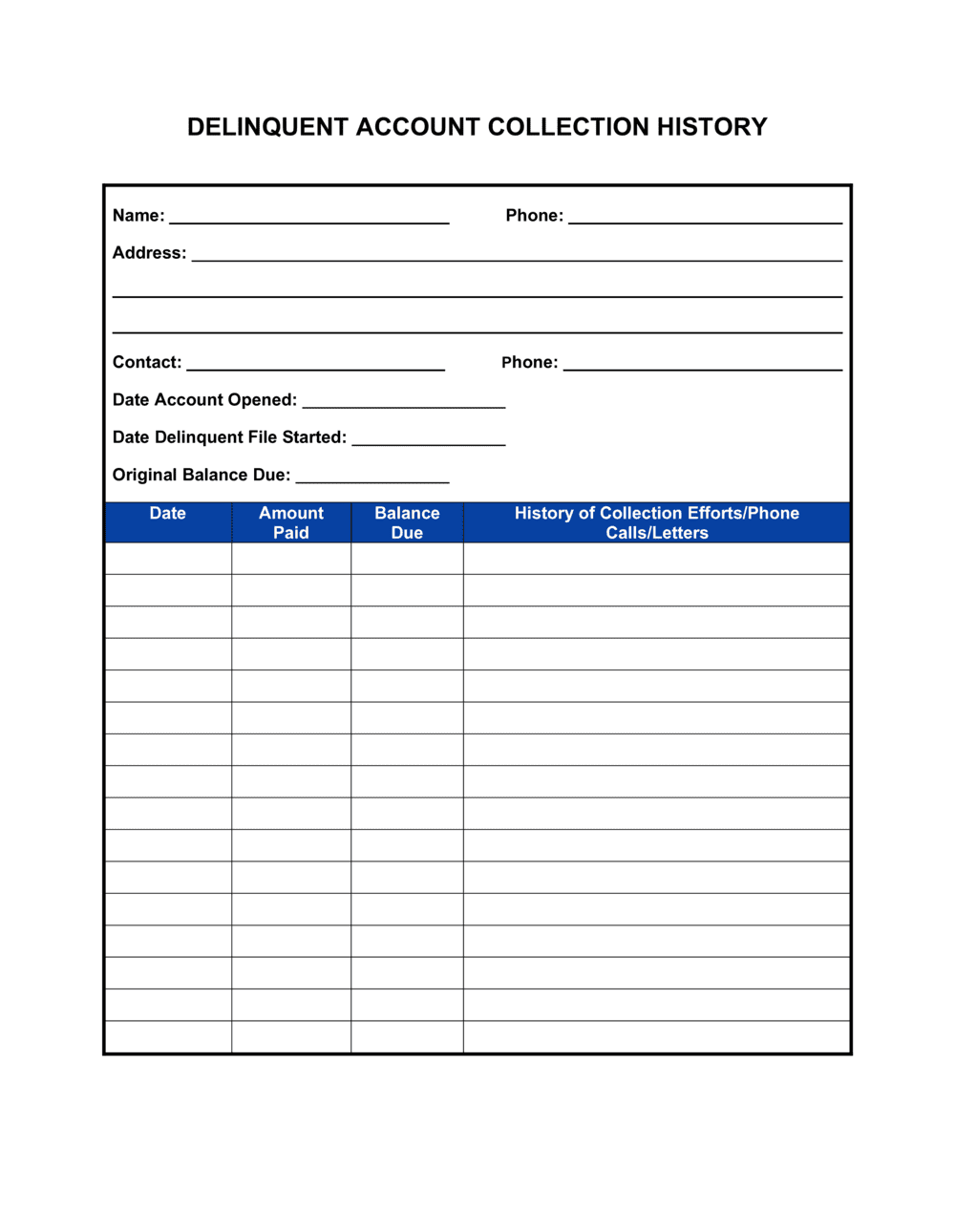

Complete the account identification block on day one of delinquency

Enter the debtor's full legal name, address, account number, original invoice or contract reference, the original balance, and the date payment was first missed. This anchors the entire record.

💡 Cross-reference the debtor's name against your contract or credit application to confirm the exact legal entity — suing the wrong entity wastes time and fees.

2

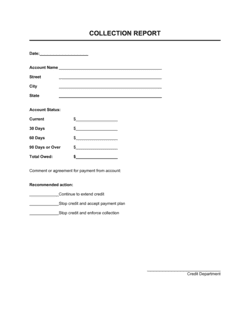

Record the current outstanding balance with a full breakdown

Enter principal, accrued interest at the contracted rate, any late fees permitted by your agreement, and subtract payments already received. Update this figure each time a payment is logged.

💡 Confirm your late-fee and interest rates are disclosed in the original agreement — undisclosed fees are unenforceable in most jurisdictions and can trigger counter-claims.

3

Log every contact attempt immediately after it occurs

Record the date, time, method, and outcome of every call, email, letter, and text — including unanswered attempts. Note the name of anyone you spoke with and summarize their response in two to three sentences.

💡 Log entries the same day they occur. Memory fades and reconstructed logs are easily challenged; a contemporaneous timestamp is your strongest credibility tool.

4

Document every promise to pay with a follow-up date

When a debtor commits to a payment, record the exact amount promised, the exact date promised, and set a calendar follow-up for the day after that date to record whether the promise was kept or broken.

💡 A pattern of three or more broken PTPs is strong evidence of willful non-payment and can support an application for summary judgment in some jurisdictions.

5

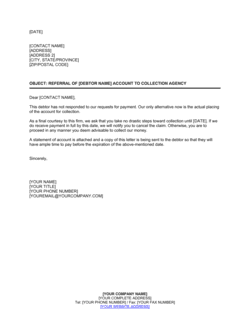

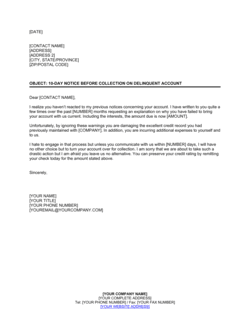

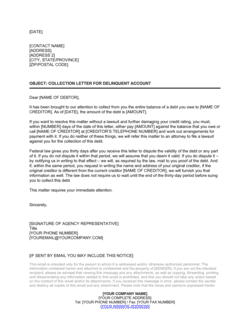

Retain and log all written correspondence with delivery confirmation

For each notice sent — demand letter, validation notice, final notice — record the date, method, and proof of delivery such as a certified mail tracking number, courier receipt, or email read receipt.

💡 Send all statutory notices by certified mail with return receipt requested, even if you also email them — postal confirmation is the gold standard in court and regulatory proceedings.

6

Record escalation decisions with supervisor authorization

When the account qualifies for escalation — typically after 60–90 days past due with broken PTPs — enter the escalation type, the name and title of the authorizing manager, and the stated reason.

💡 Define your escalation thresholds in writing (e.g., 'agency referral after 90 days past due and two broken PTPs') so every account is treated consistently, reducing fair-lending or discriminatory-collection exposure.

7

Update the log through legal referral and judgment

If the account is referred to an attorney or agency, record the referral date, contact details, and case number when filed. Continue updating with court dates, judgment amounts, and enforcement actions.

💡 Request written confirmation from your attorney each time a milestone occurs — filing date, hearing date, judgment date — and attach it to the collection file alongside this log.

8

Close and sign the record when the account reaches final status

Enter the final status (paid in full, settled, written off, or referred), the closing date, and have the responsible collector or account manager sign and date the document to authenticate it.

💡 Retain the signed collection history for at least seven years — or the applicable statute of limitations plus two years, whichever is longer — in case the debt is later disputed or sold.