Credit Management Templates

★★★★★4.7from 280+ reviews· Trusted by 20M+ businesses

Issue credit, collect on overdue accounts, and manage risk with ready-to-use documents for every step of the credit cycle.

WordEditable onlinePDF31+ credit management templates

Other Finance & Accounting categories

Most popular credit management templates

Credit applications and account setup

Account management and credit controls

More credit management templates

250K+Clients

20M+Free users

20+Years

190+Countries

10,000+Law firms

50M+Downloads

Trusted across review platforms

- Capterra★★★★☆4.649 reviews

- G2★★★★☆4.713 reviews

- GetApp★★★★☆4.649 reviews

- Google Play★★★★☆4.6179 ratings

- Google Reviews★★★★☆4.567 reviews

Frequently asked questions

What is credit management in a business context?

Credit management is the process of deciding whom to extend credit to, on what terms, and how to collect if they don't pay. It covers everything from reviewing credit applications and setting credit limits to issuing invoices, monitoring overdue balances, and pursuing collection when necessary. Effective credit management reduces bad debt and improves cash flow without turning away good customers.

Is a promissory note legally enforceable?

Yes, a properly executed promissory note is generally enforceable as a negotiable instrument in most jurisdictions. It must identify the parties, state a definite sum, include repayment terms, and be signed by the borrower. Because enforcement rules vary by jurisdiction and loan size, consider having a lawyer review any note for a significant amount.

When should a business run a credit application instead of just asking for payment upfront?

Running a credit application makes sense when you're entering an ongoing supply relationship, the customer's order volume justifies the administrative cost, or industry norms favor net-30 or net-60 payment terms. For one-time or small transactions, payment upfront or by card is simpler and carries no credit risk.

What is the difference between a credit memo and a refund?

A credit memo reduces the balance a customer owes on their account — no cash changes hands. A refund returns cash (or a card payment reversal) to the customer. Use a credit memo when the customer will make future purchases and wants to apply the credit; issue a refund when the relationship is complete or the customer requests cash back.

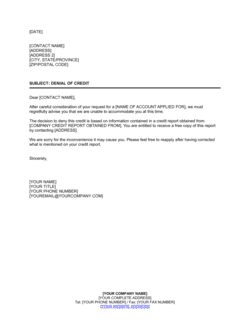

Can a business deny credit without giving a reason?

In many jurisdictions, businesses extending consumer credit are legally required to provide written notice of denial and the principal reasons, particularly when the decision is based on a credit report. Commercial (business-to-business) credit decisions are generally less regulated, but a written denial is still good practice for transparency and to avoid disputes. Always check applicable consumer protection and anti-discrimination laws in your jurisdiction.

What triggers an acceleration clause?

An acceleration clause is typically triggered by a missed payment, insolvency or bankruptcy filing, breach of a covenant in the credit agreement, or material deterioration in the borrower's financial condition. Once triggered, the full outstanding balance becomes due immediately rather than on the original schedule.

How long should a credit policy document be?

Most small-to-mid-sized business credit policies run two to five pages. They should cover at minimum: approval criteria and documentation requirements, credit limit tiers, payment terms, late-payment procedures, collection escalation steps, and authority levels for approvals and exceptions. A policy that is too short leaves gaps; one that is too long won't be followed.

What is a movable hypothec promissory note?

A movable hypothec is a security interest over movable property (personal property in common-law jurisdictions) used primarily in Quebec civil law. A movable hypothec promissory note combines the debt obligation with a charge over specified movable assets, giving the lender priority over those assets if the borrower defaults. It is the civil-law equivalent of a secured promissory note backed by a UCC filing in the US.

Credit Management vs. related documents

A credit memo and a credit note are often used interchangeably, but some businesses distinguish them: a credit memo adjusts an existing invoice in the accounts receivable ledger, while a credit note is sent to the customer as written confirmation of the credit. In practice, both reduce the amount a customer owes. Use the credit memo template for internal accounting records and the credit note template when the customer needs a formal document for their own records.

A promissory note is a simpler, one-sided instrument in which the borrower promises to repay a specified amount. A loan agreement is a bilateral contract that includes obligations on both the lender and borrower — covenants, representations, and default procedures. Promissory notes suit straightforward short-term lending; loan agreements are preferred for larger, longer-term, or more complex financing where both sides carry ongoing duties.

A credit policy is an internal document that governs how your business evaluates and grants credit — it is for your staff. A credit application is an external document completed by a customer seeking credit — it gives you the information to apply the policy. Both are necessary: the policy ensures consistent decisions; the application ensures you collect the right data to make them.

A denial of credit refuses the application outright, typically citing insufficient creditworthiness. Restrictions on credit grants credit but with reduced limits, shorter terms, or additional conditions. Use the denial when the applicant does not meet minimum criteria; use restrictions when partial credit is appropriate pending improved payment history.

Key clauses every Credit Management contains

Credit management documents share a set of core clauses that define the obligation, protect the creditor's rights, and establish what happens if the debtor defaults.

- Parties and account identification. Names the creditor and debtor using their full legal names and, where applicable, account numbers.

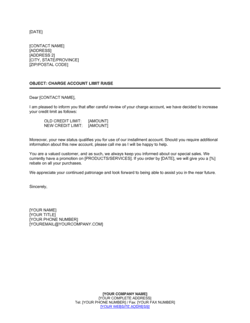

- Principal amount and credit limit. States the amount lent or the maximum credit extended, which sets the ceiling of the obligation.

- Interest rate and calculation method. Specifies the applicable rate (fixed or variable), compounding frequency, and how interest accrues.

- Repayment terms. Sets the payment schedule, due dates, acceptable payment methods, and any grace period.

- Acceleration clause. Allows the creditor to demand full repayment immediately if the debtor misses a payment or breaches a term.

- Default and remedies. Defines what constitutes a default and the creditor's rights — including collection costs and legal fees.

- Security or collateral. Identifies any assets pledged as security for the debt, which the creditor may claim on default.

- Governing law. Names the jurisdiction whose laws govern interpretation and enforcement of the credit instrument.

How to write a credit management document

The structure of every credit document follows the credit lifecycle: establish the parties, define the obligation, set the terms, and specify what happens when things go wrong.

1

Identify the parties precisely

Use full legal names for both the creditor and debtor — including any registered business names, addresses, and account or tax identifiers.

2

State the amount and type of credit

Specify the exact principal, credit limit, or adjustment amount, and whether it is a lump-sum loan, revolving line, or invoice correction.

3

Set interest rate and fees

Include the annual interest rate, compounding frequency, and any origination fees or late-payment charges permitted under applicable law.

4

Define the repayment schedule

List due dates, minimum payment amounts, acceptable payment methods, and the grace period before a payment is considered late.

5

Include an acceleration and default clause

State clearly that missing a payment or breaching any term entitles the creditor to demand the entire outstanding balance immediately.

6

Specify security and guarantees

If any collateral or personal guarantee secures the obligation, describe the asset or guarantor and the process for claiming it on default.

7

Add governing law and dispute resolution

Name the jurisdiction whose laws apply and whether disputes go to court or arbitration, so both parties know the enforcement path.

8

Sign, date, and store the executed document

Have authorized representatives sign, retain executed originals in your accounts receivable file, and set calendar reminders for key payment dates.

At a glance

- What it is

- Credit management documents are the formal instruments businesses use to extend, monitor, restrict, and recover credit extended to customers or counterparties. They range from promissory notes and credit applications to collection letters and credit policies.

- When you need one

- Any time your business lends money, sells on account, sets credit terms, or needs to collect on an overdue balance, you need a written credit management document to record the obligation and protect your right to collect.

Which Credit Management do I need?

The right template depends on where you are in the credit lifecycle: originating credit, managing an active account, or collecting on a past-due balance. Match your situation below.

Your situation

Recommended template

Lending a fixed sum to a borrower with a repayment schedule

Records the debt, repayment terms, and interest in a single enforceable instrument.Extending a revolving line of credit to a borrower

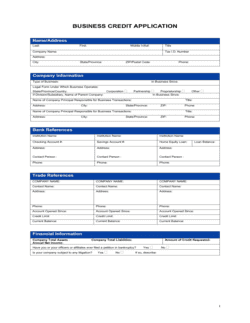

Covers draws, repayments, and re-borrowing rights on a revolving basis.Evaluating a new business customer before granting credit

Collects the financial and trade-reference information needed to assess risk.Setting internal rules for who gets credit and on what terms

Documents approval criteria, credit limits, and payment terms for staff guidance.Issuing a refund or adjustment against an outstanding invoice

Formally reduces the amount owed by a customer without issuing a cash refund.Turning down a credit application from a customer or consumer

Provides a compliant written notice of refusal with reason codes as required.A borrower has missed payments and you need to demand repayment

Puts the borrower on formal notice that full payment is due immediately.Closing a customer's credit line due to non-payment or risk

Formally terminates the credit facility and states the outstanding balance owed.Glossary

- Promissory note

- A signed written promise by one party to pay a specified sum to another party on demand or on a set date.

- Credit limit

- The maximum outstanding balance a creditor will permit a customer to carry at any one time.

- Acceleration clause

- A contract provision that makes the entire debt balance due immediately upon a specified default event.

- Credit memo

- An internal accounting document that reduces the amount a customer owes, typically due to a return, error, or adjustment.

- Credit note

- A document issued to a customer confirming that a credit has been applied to their account, reducing their outstanding balance.

- Default

- Failure by a debtor to meet a payment obligation or other term of a credit agreement on time.

- Collateral

- An asset pledged by a borrower to secure a loan, which the lender may seize if the borrower defaults.

- Net terms

- Payment terms that give the buyer a set number of days — commonly 30, 60, or 90 — to pay an invoice after the invoice date.

- Accounts receivable

- Money owed to a business by customers who have received goods or services on credit.

- Credit reference

- A third party — typically a supplier or bank — that provides information about an applicant's payment history when they apply for credit.

- Revolving credit

- A credit facility that allows the borrower to draw, repay, and re-borrow funds up to an approved limit on an ongoing basis.

- Charge-off

- The accounting action of writing off a debt as a loss after it has been deemed uncollectible, typically after a prolonged delinquency period.

What is a credit management document?

A credit management document is any formal instrument a business uses to

originate, administer, or recover credit extended to customers, clients, or

counterparties. The category spans promissory notes and credit applications at

one end, through credit memos, credit limit notices, and credit policies in

the middle, to collection letters and default notices at the other end. Together

these documents form the paper trail that defines the credit relationship,

protects the creditor's right to collect, and gives the debtor a clear record

of what they owe and on what terms.

Credit management documents are particularly important because credit risk is

one of the most common sources of unexpected loss for businesses of any size.

Without written instruments, disputes about the amount owed, the agreed

interest rate, the payment schedule, or the consequences of default are nearly

impossible to resolve in your favour. With them, the obligation is clear, the

remedies are pre-agreed, and enforcement — whether through demand letters,

collection agencies, or courts — follows a defined path.

When you need a credit management document

Any time money changes hands on a deferred basis — or any time you need to

adjust, restrict, or recover a credit balance — a written document should

accompany the transaction. The need arises at every stage of the credit

lifecycle.

Common triggers:

- A customer asks to open a trade account and pay on net-30 or net-60 terms

- A small business lends money to a partner, supplier, or employee

- A borrower requests a line of credit rather than a single lump-sum loan

- A customer returns goods and you need to issue an adjustment against their account

- An applicant does not meet your credit criteria and must be formally declined

- A customer's payment history has deteriorated and you need to reduce their limit

- A borrower has missed payments and you need to issue a formal demand

- A credit line must be cancelled due to chronic non-payment or insolvency risk

Skipping written credit documentation rarely saves time — it only defers the

problem until the moment you most need to enforce the obligation and can't.

A well-chosen template from this folder puts the right language in place in

minutes, so you can extend credit confidently and collect on it when you need to.

Award-winning platform

- Great Place to Work 2025

- BIG Award — Product of the Year 2025

- Smartest Companies 2025

- Global 100 Excellence 2026

- Best of the Best 2025