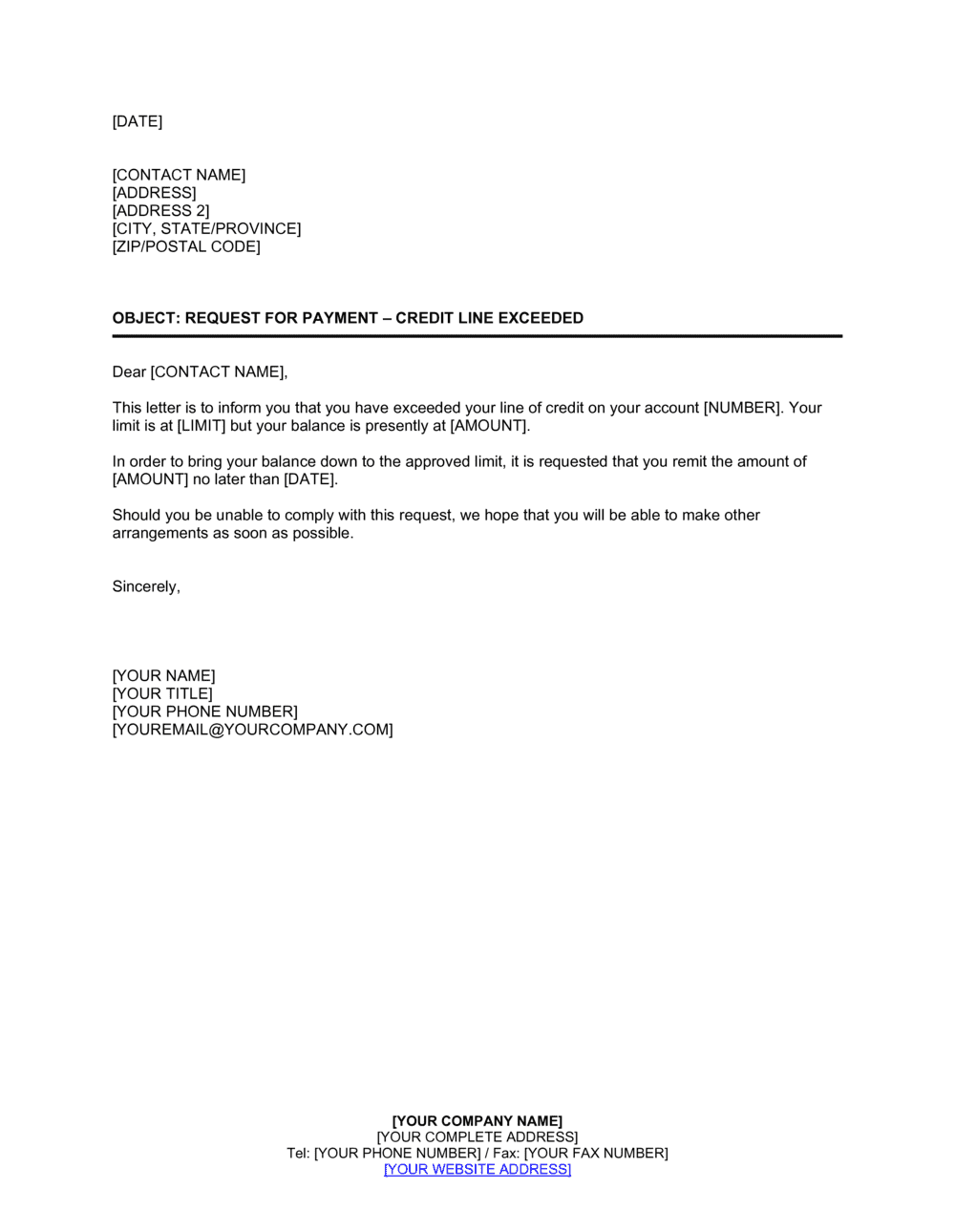

❌ Using approximate figures instead of exact balances

Why it matters: A customer who receives a letter with rounded or estimated numbers can question the accuracy of the entire balance and use the discrepancy to delay payment while requesting documentation.

Fix: Pull exact figures directly from your AR system on the day the letter is drafted, and reference the specific invoice numbers that make up the outstanding balance.