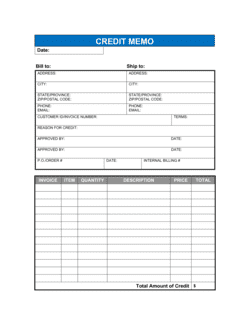

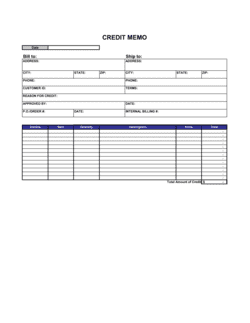

1

Enter seller and buyer legal entity names

Use the full registered legal name of both parties — not trade names or DBAs. Cross-reference the original purchase order or invoice to ensure the names match exactly.

💡 Mismatched entity names between the credit notice and the original invoice are the single most common cause of payment reconciliation delays in accounts receivable systems.

2

Reference the RMA number and original invoice

Enter the return merchandise authorization number previously issued, along with the original purchase order and invoice numbers. This links the credit notice to the physical return and the financial transaction.

💡 If no RMA was issued prior to the return, issue one retroactively and document the reason — an unauthorized return with no paper trail creates inventory and audit problems.

3

List returned goods with full product detail

Record each returned item on its own line with product name, SKU or part number, quantity returned, and unit price from the original invoice. Include lot or serial numbers for regulated or high-value goods.

💡 Copy line items directly from the original invoice rather than retyping descriptions — any variation in product description can make it difficult to match credits against specific inventory records.

4

Document the inspection outcome

Record the date goods were inspected, the condition found, and whether the return is accepted in full, partially, or rejected. Note who performed the inspection and their role.

💡 Photograph returned goods before and after inspection for high-value or dispute-prone returns — photos stored with this document provide objective evidence if the buyer contests the credit amount.

5

Calculate gross and net credit amounts

Start with the original invoiced price of the returned goods, then subtract any restocking fee, return shipping costs charged to the seller, or damage reduction. Show each deduction explicitly.

💡 State the restocking fee as both a percentage and a dollar amount — buyers who see only the percentage or only the dollar figure are more likely to dispute the math.

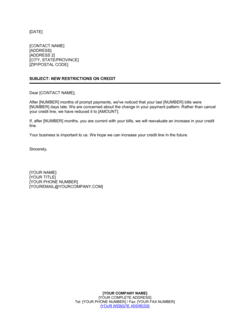

6

Specify how and when the credit will be applied

State the posting date, whether the credit offsets a specific outstanding invoice or sits as an open balance, and — if a cash refund — the method and expected timeline for payment.

💡 If the credit offsets a specific invoice, reference that invoice number explicitly. Leaving an open credit balance without tying it to a receivable creates reconciliation problems at both companies' period-end.

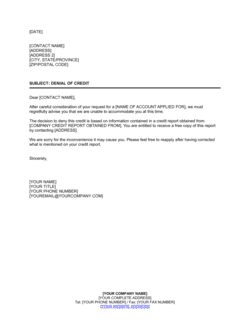

7

Set conditions, limitations, and the no-liability clause

Enter any expiry date for unused credit balances, confirm the no-admission-of-liability language is included, and review the governing law clause to confirm it matches the original purchase agreement.

💡 For warranty or recall returns, have legal counsel review the no-liability clause before sending — the language must be clear enough to withstand a later product-liability argument.

8

Obtain authorized signatures and distribute

Both parties' authorized representatives should sign the notice. Retain a fully executed copy in your accounts receivable file alongside the original invoice, RMA, and goods receipt record.

💡 Send the signed notice by email with read receipt or tracked delivery — a timestamped delivery record matters if the buyer later disputes whether they received the credit notification.