- Sales Invoice

- A legally binding demand for payment issued by a seller to a buyer after goods have been delivered, specifying what was sold, the price, and when payment is due.

- Payment Terms

- The agreed conditions under which the buyer must pay — for example, Net 30 means the full amount is due within 30 days of the invoice date.

- Late-Payment Penalty

- A contractual charge applied to balances not paid by the due date, typically expressed as a monthly percentage rate such as 1.5% per month.

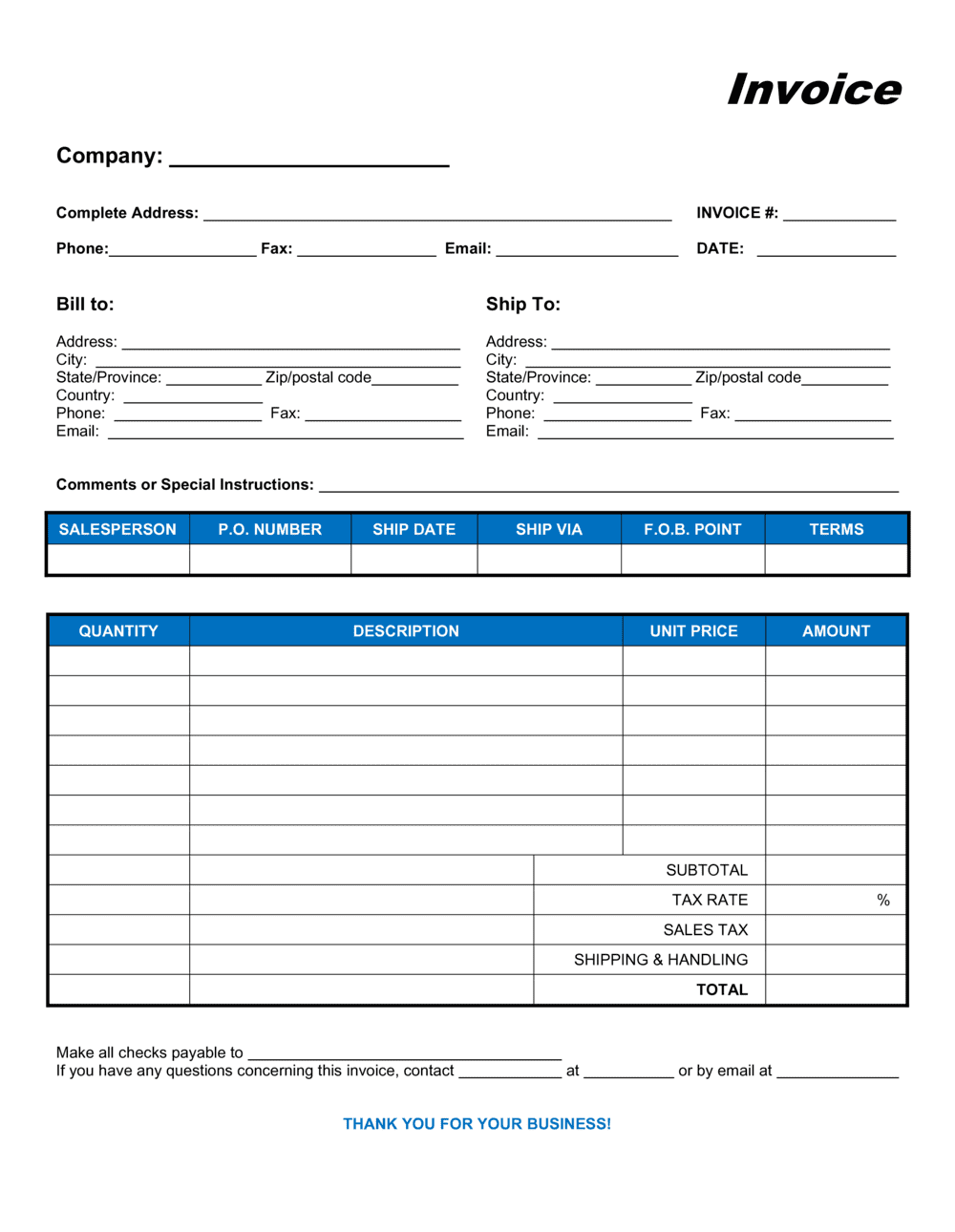

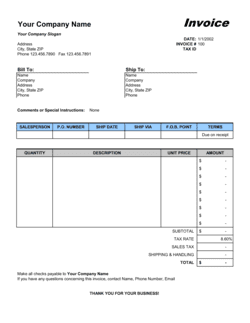

- Purchase Order (PO) Number

- A reference number issued by the buyer before delivery to authorize the purchase; including it on the invoice helps the buyer match and approve payment faster.

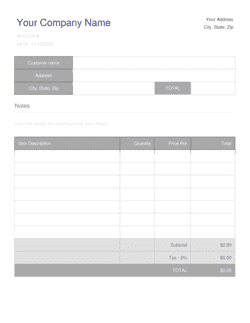

- Line Item

- A single row on the invoice representing one product or SKU with its description, quantity, unit price, and extended total.

- Tax Invoice

- A sales invoice that meets specific regulatory requirements — including the seller's tax registration number — allowing the buyer to claim a VAT or GST credit.

- Title of Goods

- Legal ownership of the goods; a sales invoice often specifies when title transfers from seller to buyer — at shipment, at delivery, or upon full payment.

- Retention of Title (ROT)

- A clause stating the seller retains legal ownership of the goods until the buyer pays in full, allowing the seller to reclaim goods if payment is not made.

- FOB (Free on Board)

- A shipping term specifying the point at which the buyer assumes risk and cost for goods in transit — FOB Origin means at the seller's loading dock; FOB Destination means at the buyer's delivery point.

- Credit Note

- A document issued to reduce or cancel a previously sent sales invoice, used for returns, pricing errors, or negotiated adjustments.

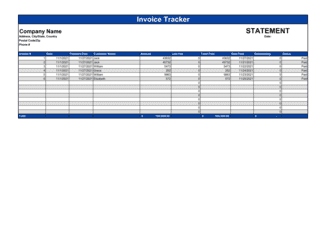

- Accounts Receivable

- Money owed to a business by its customers for goods or services delivered but not yet paid for; sales invoices create the accounts-receivable entry.

- Aging Report

- An accounts-receivable report grouping outstanding invoices by how long they have been unpaid — typically 0–30, 31–60, 61–90, and 90+ days.