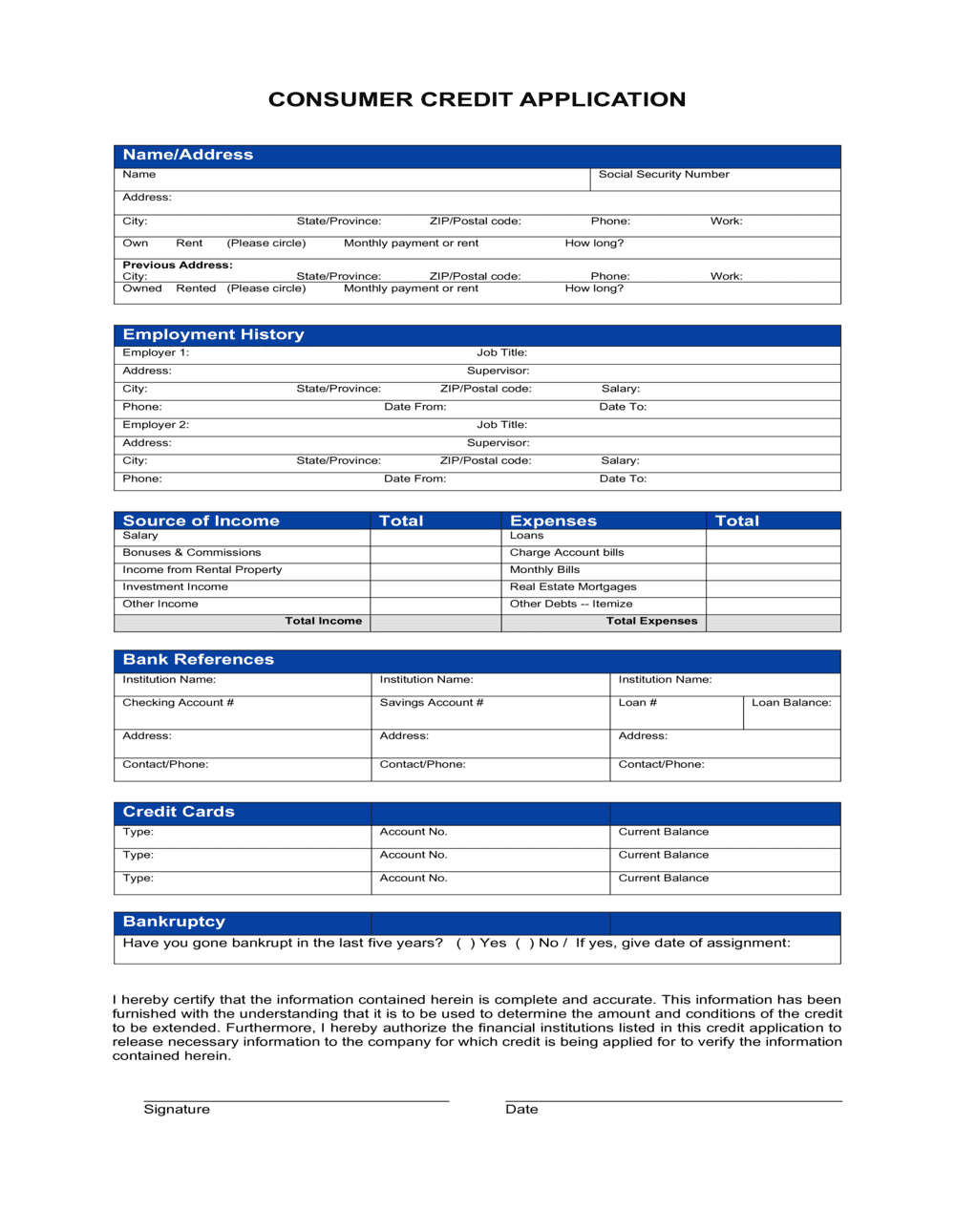

❌ Pulling a credit report before collecting a signed authorization

Why it matters: Under the Fair Credit Reporting Act, obtaining a consumer report without a permissible purpose and signed authorization exposes the lender to civil liability and regulatory penalties.

Fix: Make the signed authorization the last step before submission — build a checklist that includes 'authorization signed' as a hard gate.