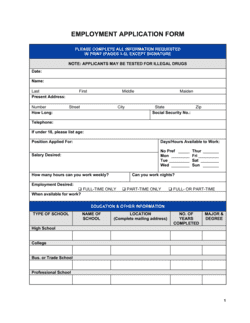

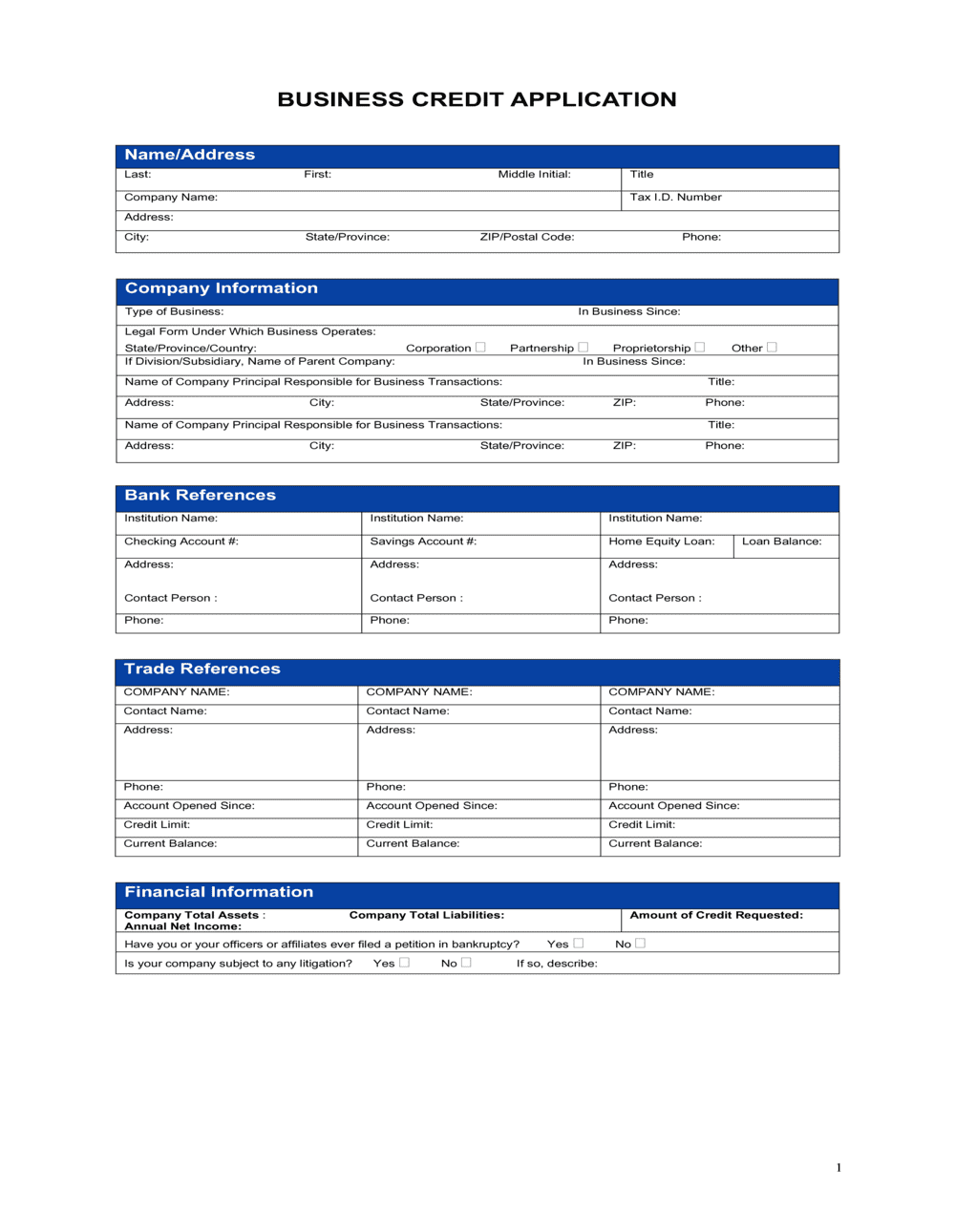

❌ Using a trade name instead of the legal entity name

Why it matters: The supplier's credit team runs checks against the legal entity name and EIN. A DBA or brand name returns no matching record and stalls the application indefinitely.

Fix: Confirm the exact registered name from your EIN filing or state business registration before completing the form.