Accounts Receivable Templates

★★★★★4.7from 280+ reviews· Trusted by 20M+ businesses

Track, assign, and collect outstanding receivables with the right document for every stage of the cash cycle.

WordEditable onlinePDF18+ accounts receivable templates

Other Finance & Accounting categories

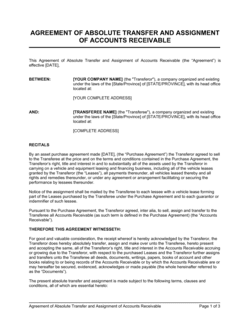

Assignment and transfer agreements

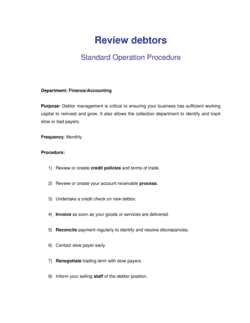

Policy, process, and ledger

More accounts receivable templates

250K+Clients

20M+Free users

20+Years

190+Countries

10,000+Law firms

50M+Downloads

Trusted across review platforms

- Capterra★★★★☆4.649 reviews

- G2★★★★☆4.713 reviews

- GetApp★★★★☆4.649 reviews

- Google Play★★★★☆4.6179 ratings

- Google Reviews★★★★☆4.567 reviews

Frequently asked questions

What is an accounts receivable template used for?

An accounts receivable template is used to record, manage, assign, or verify money owed to a business by its customers. Specific templates cover the AR ledger itself, assignment and transfer agreements when receivables are sold to third parties, audit confirmation letters, and collection improvement checklists. Each template standardizes a different stage of the AR lifecycle.

What is the difference between assigning receivables with and without recourse?

With recourse, the assignor remains liable if the debtor fails to pay — the assignee can demand the assignor buy back uncollected balances. Without recourse, the assignee absorbs all default risk and cannot recover from the assignor if the debtor doesn't pay. Non-recourse arrangements cost more (higher discount rates) because the buyer takes on more risk.

Is an assignment of accounts receivable legally binding?

Yes, when properly drafted and executed by authorized representatives, an assignment of accounts receivable is generally enforceable. Most jurisdictions require that the debtor can be notified of the assignment and that the receivables are clearly identified. Consider consulting a lawyer if the receivables involve secured lending or regulated industries.

Does the debtor need to be notified of an assignment?

In many jurisdictions, notice to the debtor is required for the assignment to be enforceable against that debtor. Without notice, the debtor may validly pay the original assignor and discharge their obligation, leaving the assignee with no recourse against the debtor. Check applicable law and include a notice clause in your agreement.

What is accounts receivable factoring?

Factoring is an ongoing commercial arrangement where a business sells invoices to a factoring company (the factor) at a discount in exchange for immediate cash. It differs from a one-time assignment in that factoring typically involves a continuing flow of invoices, a servicing relationship, and a facility agreement. An assignment agreement is usually one component of a larger factoring arrangement.

How do I improve slow accounts receivable collections?

Start by reviewing your credit terms, invoicing accuracy, and follow-up cadence. Common improvements include shortening payment terms, sending invoices immediately on delivery, automating payment reminders, and escalating overdue accounts on a fixed schedule. The Checklist Action to Improve Collection of Accounts template (D183) provides a structured process for identifying and fixing gaps in your collections workflow.

What is a request for verification of receivable during an audit?

It is a standardized confirmation letter sent by an auditor (or by the business at an auditor's request) to a debtor, asking them to confirm the balance they owe as of a specific date. The response provides independent third-party evidence that the receivable is real and accurately stated, which is a required audit procedure for most financial statement audits.

Can I use an AR template without a lawyer?

For routine internal documents — ledgers, checklists, debtor review procedures — a well-drafted template is typically sufficient. For assignment and transfer agreements involving material dollar amounts, secured creditors, or cross-border parties, a 1–2 hour legal review is advisable. The legal risk in a poorly drafted assignment agreement generally far exceeds the cost of a brief consultation.

Accounts Receivable vs. related documents

Accounts receivable represents money owed TO your business by customers; accounts payable represents money your business owes TO suppliers and vendors. AR is an asset on the balance sheet; AP is a liability. The two are managed by separate ledgers and workflows, though both affect working capital directly.

With recourse, the assignor retains liability if the debtor defaults — the buyer can "put back" uncollected receivables to the seller. Non-recourse transfers default risk entirely to the buyer. Non-recourse factoring typically costs more because the buyer absorbs all collection risk; recourse arrangements are cheaper but expose the seller to ongoing liability.

A factoring agreement is a broader commercial arrangement in which a business sells a stream of invoices to a factor on an ongoing basis, usually at a discount. An assignment of accounts receivable is a narrower, one-time legal instrument transferring specific named receivables. Factoring relationships typically incorporate an assignment agreement as one component of the overall deal.

A promissory note is a debtor's written promise to pay a fixed amount by a specific date; an accounts receivable record reflects an open balance arising from credit sales. Both represent money owed, but a promissory note is a negotiable instrument that can be transferred more easily, while AR balances require a formal assignment agreement to transfer.

Key clauses every Accounts Receivable contains

Whether you're recording a balance or transferring it to a third party, every accounts receivable document relies on the same core provisions.

- Identification of receivables. Names the specific invoices, balances, or debtor accounts covered — vague descriptions create disputes during collection or audit.

- Purchase price or consideration. States what the assignee pays for the receivables, typically expressed as a percentage of face value.

- Representations and warranties. The assignor confirms the receivables are valid, undisputed, and free of prior liens or encumbrances.

- Recourse or non-recourse election. Specifies whether the assignor remains liable if the debtor defaults — the single most important commercial term in an assignment.

- Notice to debtor. Requires or permits notification to the underlying debtor that their obligation has been assigned to a new party.

- Collections and remittance. Defines who collects payments post-assignment and how funds are remitted between the parties.

- Repurchase obligation. In recourse arrangements, sets out the conditions and timeline under which the assignor must buy back uncollected receivables.

- Governing law. Identifies the jurisdiction whose laws govern the agreement and where disputes will be resolved.

How to write an accounts receivable assignment agreement

A well-drafted AR assignment agreement protects the assignor's right to receive the purchase price and protects the assignee's right to collect from the debtor.

1

Identify all parties

State the full legal names of the assignor (current creditor), the assignee (buyer), and — where required — the underlying debtor.

2

Describe the receivables precisely

List each invoice or account by number, date, debtor name, and face amount to prevent any ambiguity about what's being transferred.

3

State the purchase price and payment terms

Specify the discount rate or flat purchase price and the date by which the assignee pays the assignor.

4

Choose recourse or non-recourse

Decide who bears the risk of non-payment by the debtor and document that election explicitly — it affects price, risk, and enforceability.

5

Add representations and warranties

The assignor should warrant that each receivable is valid, legally enforceable, and free of any prior assignment, lien, or setoff right.

6

Define the collections process

Specify whether the assignor or assignee will collect payments and how proceeds are remitted after closing.

7

Include notice and governing law provisions

Address whether and how the debtor will be notified, and name the governing jurisdiction to make enforcement straightforward.

At a glance

- What it is

- Accounts receivable (AR) documents are the contracts, ledgers, policies, and checklists a business uses to record money owed by customers, assign or transfer that debt, and enforce timely collection.

- When you need one

- Any time you extend credit to a customer, sell or assign outstanding invoices, conduct an AR audit, or need to formalize your collections process, a purpose-built AR template keeps your records defensible and your cash flow predictable.

Which Accounts Receivable do I need?

The right AR template depends on whether you're recording receivables, transferring them to a third party, verifying them during an audit, or improving your collection process. Match your situation below.

Your situation

Recommended template

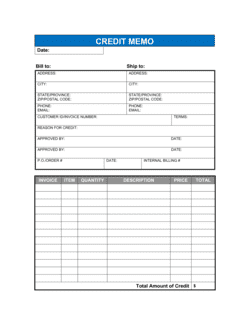

Setting up or maintaining a standard accounts receivable record

Provides a structured ledger for tracking all outstanding customer balances.Assigning receivables to a lender while retaining default risk

Your business remains liable if the debtor fails to pay the assignee.Selling receivables to a buyer who takes on all collection risk

Transfers default risk entirely to the buyer — no liability if debtor doesn't pay.Completing a full, permanent sale and transfer of receivables

Documents an outright sale with no ongoing obligation from the seller.Selling, transferring, and assigning a receivable portfolio in one agreement

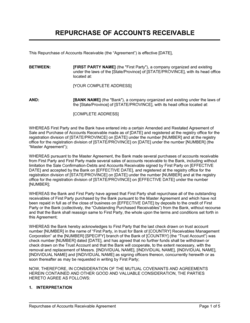

Consolidates sale, transfer, and assignment terms into a single executed document.Buying back previously assigned receivables from an assignee

Governs the terms under which the original assignor reacquires the receivables.Auditor or accountant requesting confirmation of a specific balance

Provides the standardized confirmation letter required during AR audit procedures.Collections are slow and you need a structured improvement plan

Step-by-step checklist identifies and addresses the root causes of late payments.Glossary

- Accounts receivable (AR)

- Money owed to a business by customers for goods or services already delivered but not yet paid for; recorded as a current asset on the balance sheet.

- Assignor

- The party transferring ownership of a receivable to another party.

- Assignee

- The party receiving ownership of the receivable and the right to collect payment from the debtor.

- Recourse

- The assignor's obligation to buy back a receivable if the underlying debtor fails to pay.

- Non-recourse

- An arrangement in which the assignee bears all risk of debtor default and cannot recover from the assignor.

- Factoring

- An ongoing financing arrangement in which a business sells invoices to a factor at a discount to obtain immediate cash.

- Debtor

- The customer or counterparty who owes the outstanding balance recorded in the accounts receivable.

- Face value

- The full invoice amount owed by the debtor before any discount, adjustment, or credit note.

- Audit confirmation

- A written response from a debtor confirming the balance they owe, used by auditors as independent evidence of a receivable's existence and amount.

- Days sales outstanding (DSO)

- A metric expressing the average number of days it takes a business to collect payment after a sale; lower DSO indicates faster collections.

- Setoff right

- A debtor's right to reduce the amount they owe by deducting a counterclaim or cross-debt owed to them by the creditor.

What is an accounts receivable document?

Accounts receivable (AR) documents are the contracts, ledgers, policies, and operational checklists a business uses to record money owed by customers, transfer that debt to third parties, and enforce timely collection. In accounting terms, receivables are current assets — real money already earned but not yet received — and the documents that govern them determine how quickly and reliably that money actually arrives.

The AR document category spans several distinct needs. At one end, an AR ledger or debtor review procedure supports day-to-day finance operations: who owes how much, since when, and what follow-up is scheduled. At the other end, assignment and transfer agreements are formal legal instruments used when a business sells or pledges its receivables to a lender, factor, or investor in exchange for immediate liquidity. In between sit audit verification letters, collection checklists, and payment allocation forms — each solving a specific problem in the AR lifecycle.

When you need an accounts receivable template

You need an AR template any time money flows from a customer to your business on credit terms, or any time you need to formally document, transfer, verify, or enforce those outstanding balances. These situations arise at every stage of the cash cycle.

Common triggers:

- You extend credit to a customer and need a structured record of every outstanding invoice and its aging status

- You want to raise working capital by selling or assigning invoices to a lender or factoring company

- You're transferring a receivable portfolio to a new owner and need to document the sale, transfer, and assignment in a single executed agreement

- An external auditor requests written confirmation from your debtors of the balances they owe

- A previously assigned receivable needs to be repurchased under the terms of an existing agreement

- Collections have slowed and you need a systematic checklist to identify and fix gaps in your follow-up process

- Your finance team needs a documented policy for how incoming payments are applied to specific debtor accounts

Without proper AR documentation, disputes over what is owed, who owns the receivable, and who is responsible for collection become difficult and expensive to resolve. A well-drafted set of AR templates eliminates that ambiguity before it becomes a problem.

Award-winning platform

- Great Place to Work 2025

- BIG Award — Product of the Year 2025

- Smartest Companies 2025

- Global 100 Excellence 2026

- Best of the Best 2025