- Accounts Receivable (AR)

- Money owed to a business by its customers or clients for goods or services already delivered but not yet paid for.

- Creditor

- The party owed money — the business or individual that delivered goods or services and is waiting for payment.

- Debtor

- The party that owes money — the customer or client who received goods or services and has an outstanding balance.

- Outstanding Balance

- The total amount currently owed by the debtor, including principal, accrued interest, and any applicable fees as of a stated date.

- Payment Schedule

- A contractually agreed series of payment dates and amounts by which the debtor will retire the outstanding balance.

- Late Payment Interest

- Interest charged on overdue amounts, typically expressed as an annual percentage rate applied per month to the unpaid balance.

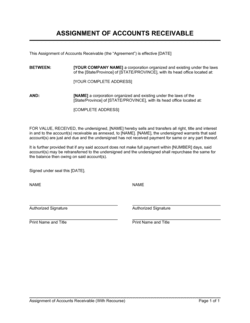

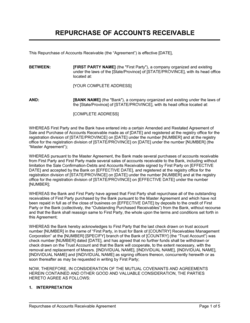

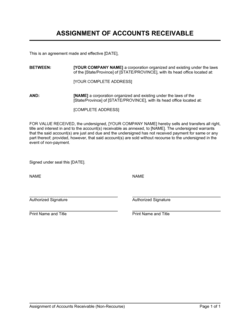

- Assignment of Receivables

- The transfer of the right to collect an outstanding debt from the original creditor to a third party, such as a factoring company or lender.

- Personal Guarantee

- A clause in which an individual — typically a director or sole trader — agrees to be personally liable for the debtor's obligation if the entity cannot pay.

- Acceleration Clause

- A provision that makes the entire outstanding balance immediately due and payable if the debtor misses a scheduled payment or breaches a material term.

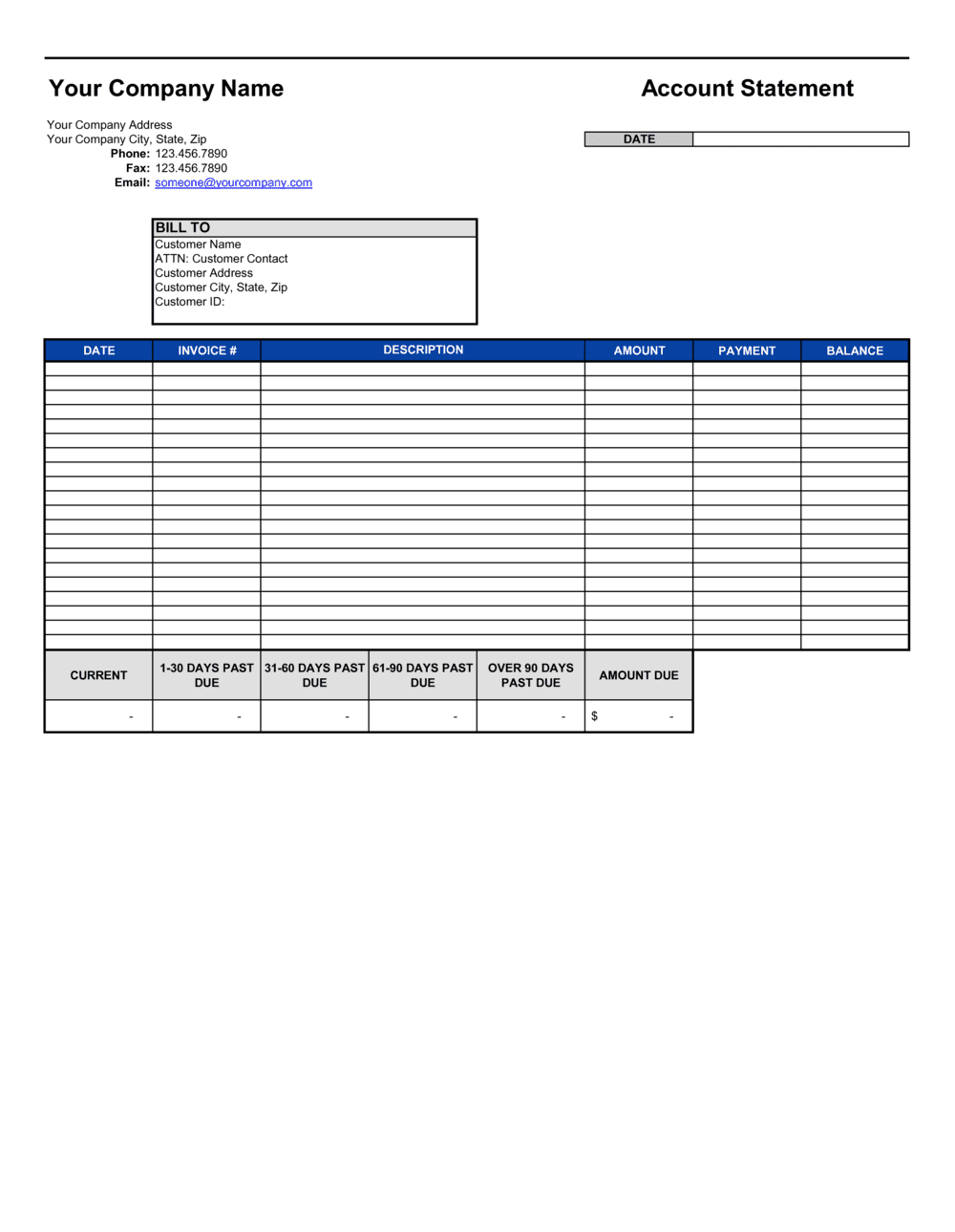

- Aging Report

- An internal AR report grouping outstanding invoices by how long they have been unpaid, typically in 0–30, 31–60, 61–90, and 90+ day buckets.

- Factoring

- A financing arrangement in which a business sells its receivables to a third party at a discount in exchange for immediate cash.

- Net Payment Terms

- The number of days from invoice date within which a buyer must pay — e.g., Net 30 means full payment is due within 30 calendar days.