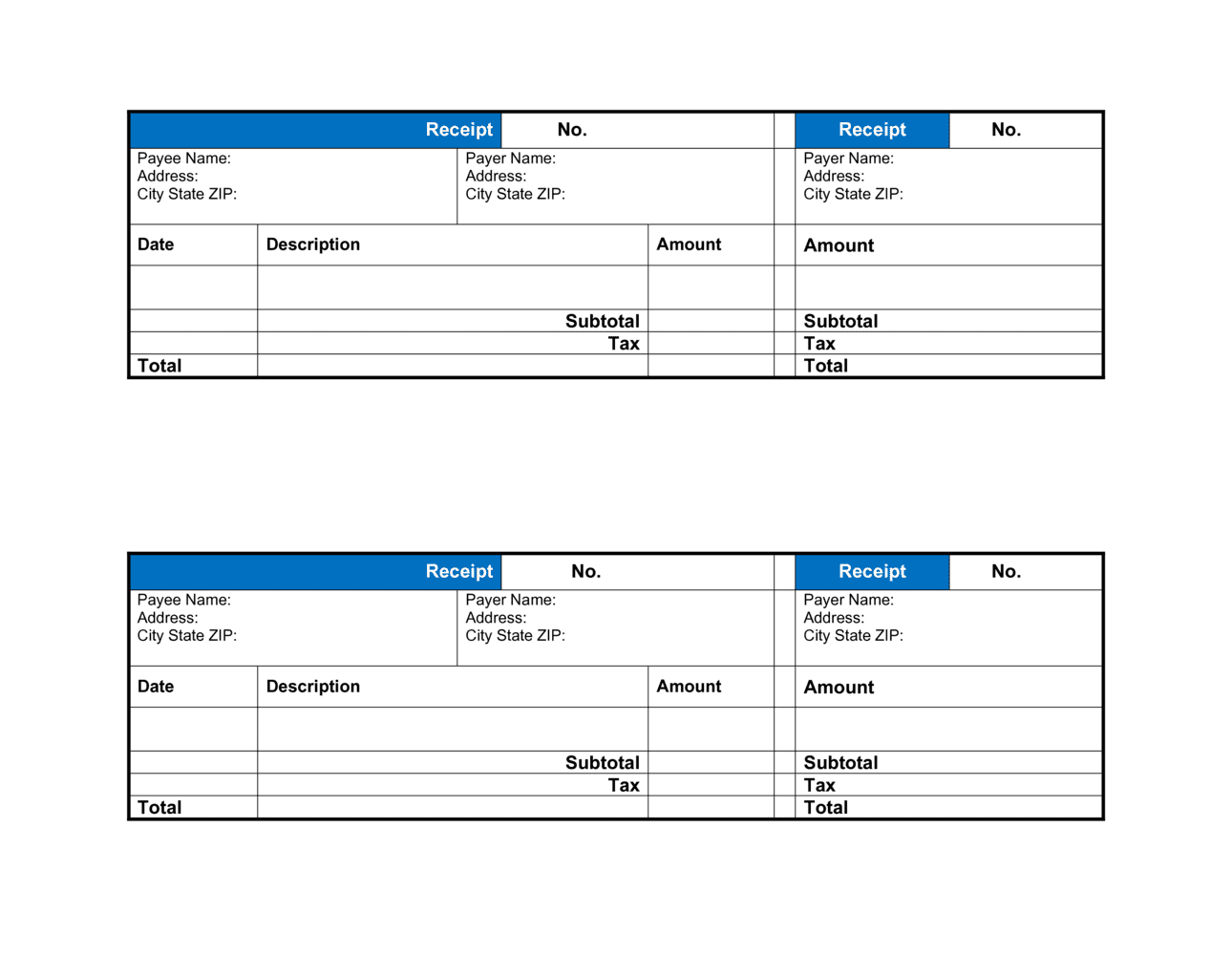

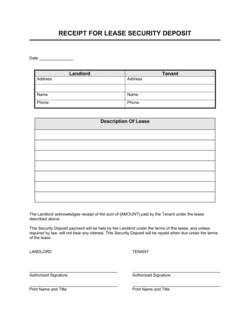

1

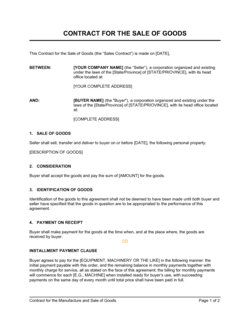

Enter both parties' legal names and contact details

Add the seller's full registered business name, address, phone, and tax ID in the seller block. Add the buyer's legal name or company name and billing address in the buyer block.

💡 Cross-reference your business registration documents to confirm the exact legal entity name — trade names and legal names often differ.

2

Assign a unique receipt number and transaction date

Use a sequential numbering format such as RCP-2026-0001. Enter the date payment was actually received, not the date the invoice was issued.

💡 A YYYY-NNNN format keeps receipts sortable by year and prevents duplicate numbering across periods.

3

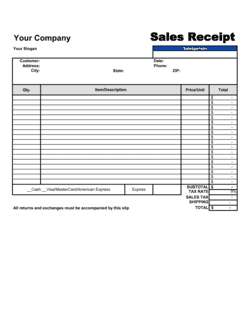

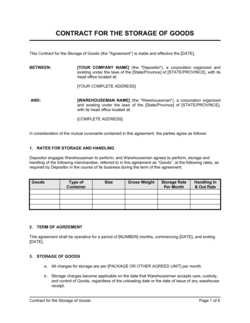

Itemize every good sold or service performed

List each product or service on a separate line with a specific description, quantity, unit price, and line total. Avoid catch-all descriptions like 'miscellaneous' or 'services.'

💡 Specific descriptions reduce dispute frequency significantly — 'Interior wall painting, 3 rooms, 400 sq ft @ $1.50/sq ft' is far more defensible than 'Painting Services.'

4

State the total amount and payment method

Enter the subtotal, applicable tax amount and rate, and the final total received. Record the exact payment method — cash, check number, bank transfer reference, or last four digits of a card.

💡 For cash payments, consider having the buyer initial next to the payment method line as additional acknowledgment.

5

Include a payment-in-full statement

Add explicit language confirming the amount received satisfies the total outstanding balance. For partial payments, state the remaining balance clearly instead.

💡 If this is a partial payment, note both the amount received and the remaining balance due on a separate line to avoid any ambiguity.

6

Describe the condition of goods and any warranty terms

State whether goods are new, used, or sold as-is. Include any warranty period if applicable, or explicitly disclaim warranties for as-is transactions.

💡 For used goods sold privately or at liquidation, an explicit 'as-is, no warranty' clause materially limits your post-sale liability.

7

Obtain signatures from both parties

Have both the seller and the buyer sign and print their names with the date. For business entities, the signatory should be authorized to bind the company.

💡 If the transaction occurs remotely, use an eSign tool to timestamp execution and create an auditable record of both parties' acknowledgment.

8

Provide a copy to both parties and retain the original

Issue the buyer a signed copy immediately upon completion of the transaction. Store your original — or a digitally executed copy — in your records for at least seven years for tax and audit purposes.

💡 Scan or photograph the receipt immediately after signing if you are using a paper copy. Ink fades and paper is lost; a digital backup is non-negotiable.