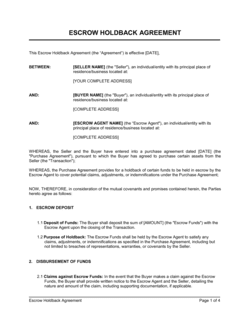

1

Identify all parties with their full legal names

Enter the escrow agent's full legal name and license number (if applicable), the remitter's full legal name and contact details, and the beneficiary's full legal name. Use registered entity names for companies, not trade names or DBA designations.

💡 Cross-check the remitter's name against the check itself — a name mismatch between the check and the receipt is a common source of processing delays and fraud flags.

2

Record complete check instrument details

Enter the check number, the name of the issuing bank, the date printed on the check, and the exact dollar amount in both numerals and written form. Note any memo or reference line on the check.

💡 If the check is a cashier's check or certified check, record that fact explicitly — it affects how quickly funds are available and how disputes are handled by the bank.

3

Reference the underlying transaction

Identify the specific transaction the funds are securing — by agreement date, property address, deal name, or LOI reference number. A clear link to the underlying deal is what makes this a valid escrow receipt rather than a generic acknowledgment.

💡 If the underlying agreement has not yet been fully executed, reference the draft or proposed transaction and plan to update the receipt once the agreement is signed.

4

Define the release conditions precisely

List each specific condition that must be satisfied before funds are released — financing contingency clearance, inspection approval, execution of closing documents, or both parties' written consent. Avoid vague terms like 'completion of the deal.'

💡 Number the conditions and use the same language as the underlying purchase or escrow agreement to prevent any interpretive gap between the two documents.

5

State the holding account type and interest allocation

Specify whether funds will be held in an interest-bearing or non-interest-bearing trust account, the bank name, and who receives any interest earned. For transactions expected to close within 30 days, a non-interest-bearing account is standard.

💡 In transactions over $100,000 or with a closing timeline exceeding 60 days, the interest allocation clause can represent real money — confirm with both parties before finalizing.

6

Set the disbursement procedure and timeline

State whether disbursement requires joint written instruction from both parties or a court order, and specify how many business days after receiving instructions the escrow agent will disburse. Typically 1–3 business days is standard.

💡 Include a wire transfer instructions addendum if disbursement will be made by wire rather than check — routing and account numbers should not appear in the body of the receipt itself.

7

Include forfeiture terms and default notice procedure

Specify what constitutes a default by the remitter, how long the remitter has to cure after written notice, and what happens to the escrowed funds upon uncured default. Tie the definition of default directly to the underlying agreement.

💡 Set the cure period to match the default cure period in the underlying purchase agreement — inconsistent timelines between documents create loopholes.

8

Execute with signatures from all three parties

Obtain signatures from the escrow agent, the remitter, and the beneficiary — each with a printed name and date. Distribute fully executed copies to all three parties and retain the original in the escrow file.

💡 If the beneficiary is not yet a party to the underlying agreement (e.g., a seller who has not countersigned), collect their signature on the receipt separately before funds are deposited.