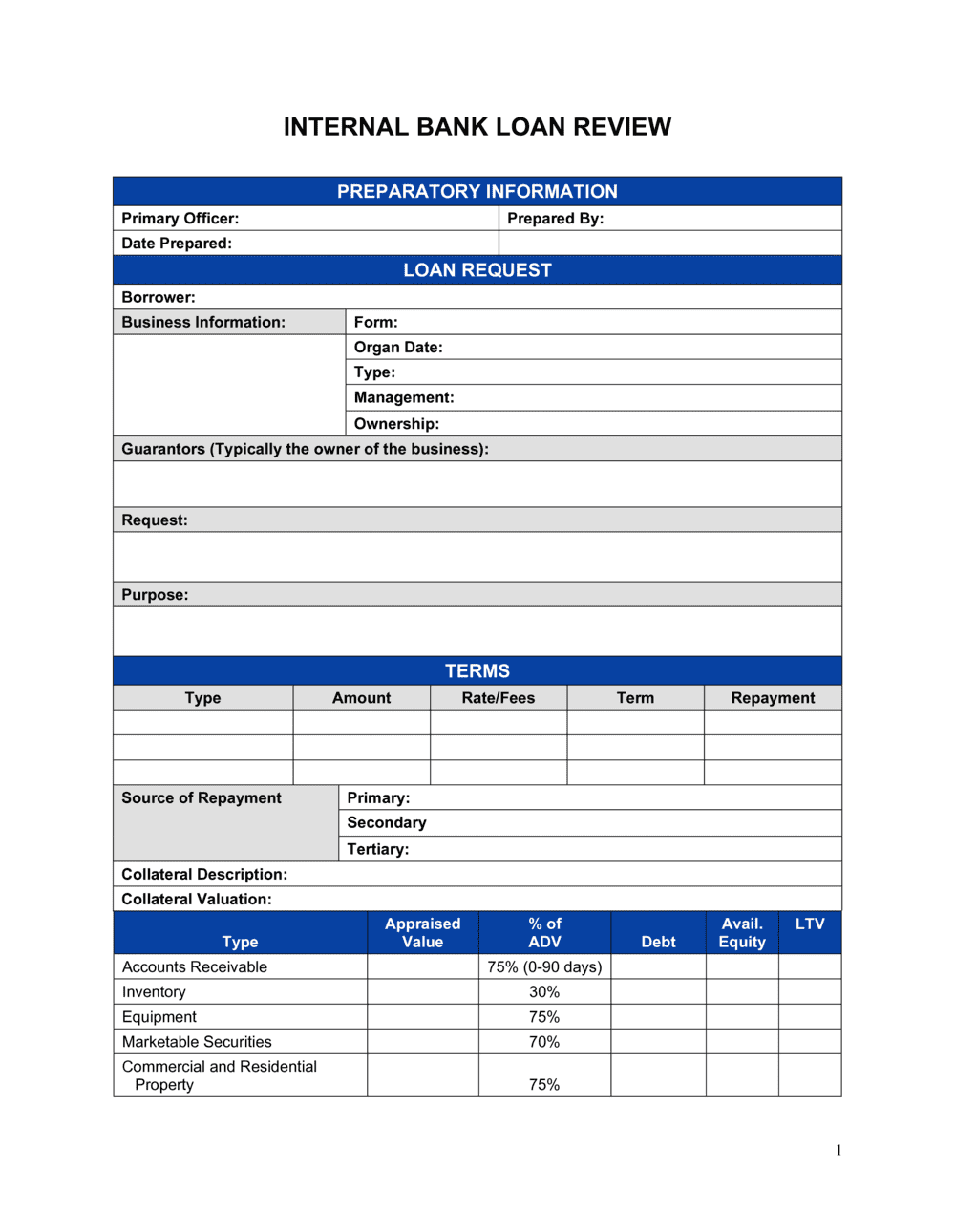

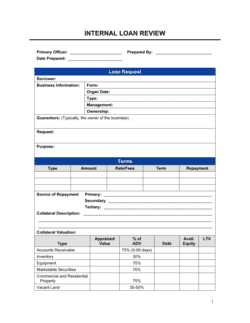

- Loan Purpose

- A clear description of how the borrowed funds will be used — for example, equipment purchase, inventory, real estate acquisition, or working capital.

- Collateral

- An asset pledged by the borrower that the lender can seize and sell if the loan is not repaid — common examples include real estate, equipment, and receivables.

- Debt Service Coverage Ratio (DSCR)

- Annual net operating income divided by total annual debt payments — a ratio above 1.25 is typically required by most business lenders.

- Loan-to-Value Ratio (LTV)

- The loan amount expressed as a percentage of the appraised value of the collateral — lower LTV ratios signal less risk to the lender.

- Personal Guarantee

- A commitment by a business owner to repay the loan personally if the business defaults, making the owner's personal assets liable.

- SBA Loan

- A business loan partially guaranteed by the U.S. Small Business Administration, enabling lenders to offer more favorable terms to borrowers who might not qualify conventionally.

- Amortization Schedule

- A table showing the breakdown of each loan payment into principal and interest over the full repayment term.

- Working Capital

- Current assets minus current liabilities — the liquid buffer a business has to cover short-term obligations and day-to-day operations.

- Pro Forma Financial Statements

- Forward-looking income statements, balance sheets, and cash flow statements built on assumptions rather than historical data, required by most lenders for new or expanding businesses.

- Underwriting

- The lender's process of evaluating a borrower's creditworthiness, collateral, and repayment capacity before approving a loan.