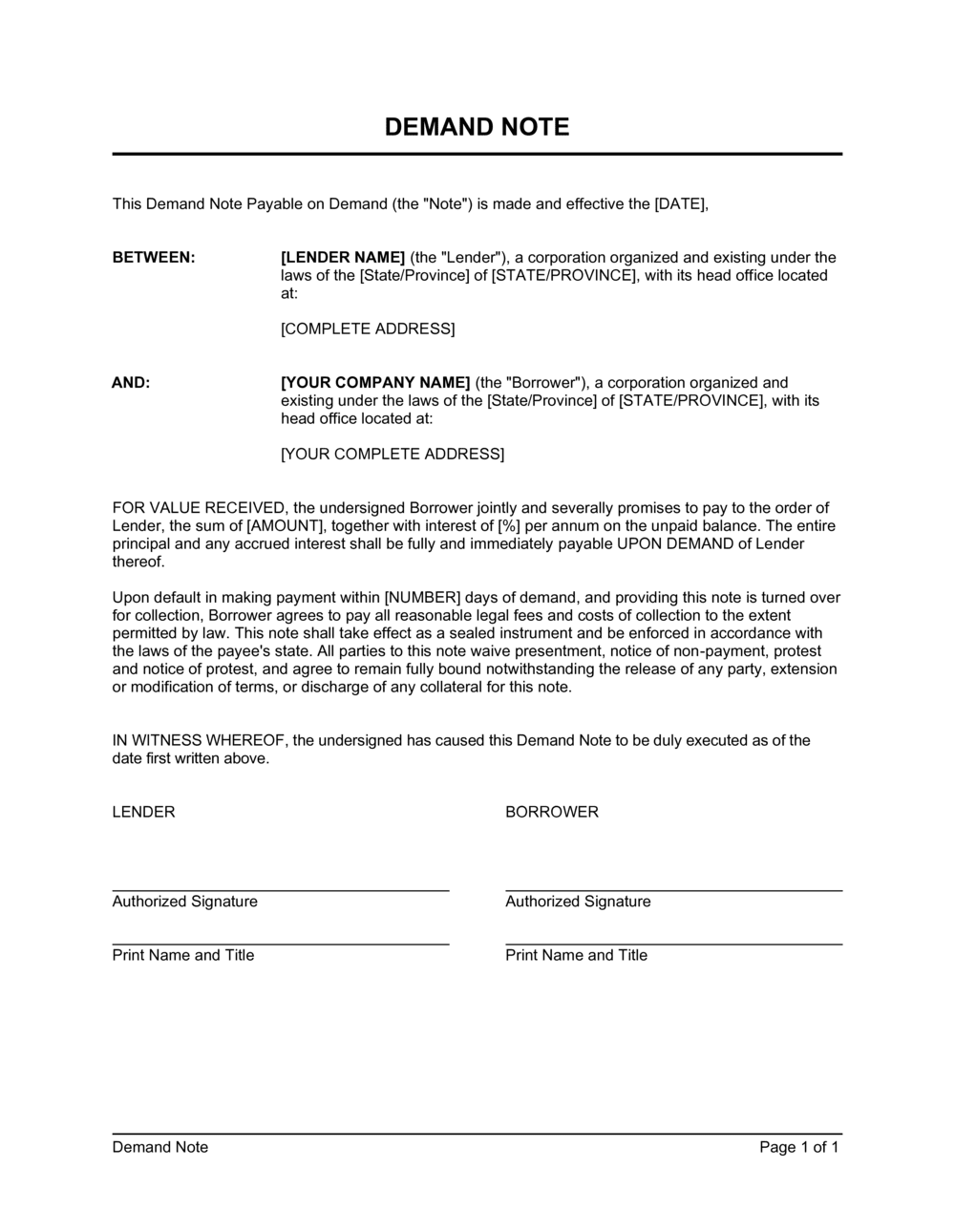

- Demand Note

- A promissory note with no fixed maturity date that becomes due and payable immediately upon the lender's written demand.

- Principal

- The original sum of money lent, exclusive of any interest that accrues over time.

- Accrued Interest

- Interest that has accumulated on the outstanding principal balance but has not yet been paid by the borrower.

- Per Annum Rate

- The annual interest rate expressed as a percentage of the outstanding principal balance.

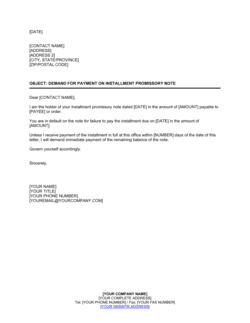

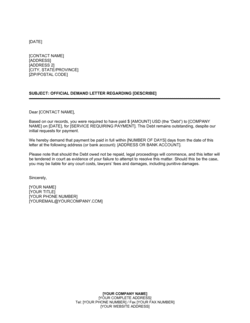

- Demand

- A written notice from the lender to the borrower requiring repayment of all or part of the outstanding balance, typically effective on delivery or within a short notice window.

- Default

- The borrower's failure to repay the full amount owed within the period specified in a demand notice, triggering the lender's right to pursue collection.

- Acceleration

- A clause that makes the entire outstanding balance immediately due upon a defined trigger event — such as the borrower's insolvency or breach of the note terms.

- Imputed Interest

- Interest the IRS or tax authority deems to have been charged on a below-market or interest-free loan, even if no interest was actually paid, creating a taxable event.

- Guarantor

- A third party who agrees to repay the note if the primary borrower fails to do so, providing the lender an additional source of recovery.

- Usury

- The practice of charging interest above the maximum rate permitted by law in the applicable jurisdiction, which can render the interest provision — or the entire note — unenforceable.

- Maker

- The party who signs a promissory note as the borrower and is legally obligated to repay the amount stated.

- Holder

- The party who holds and is entitled to enforce a promissory note — typically the lender or any subsequent assignee.