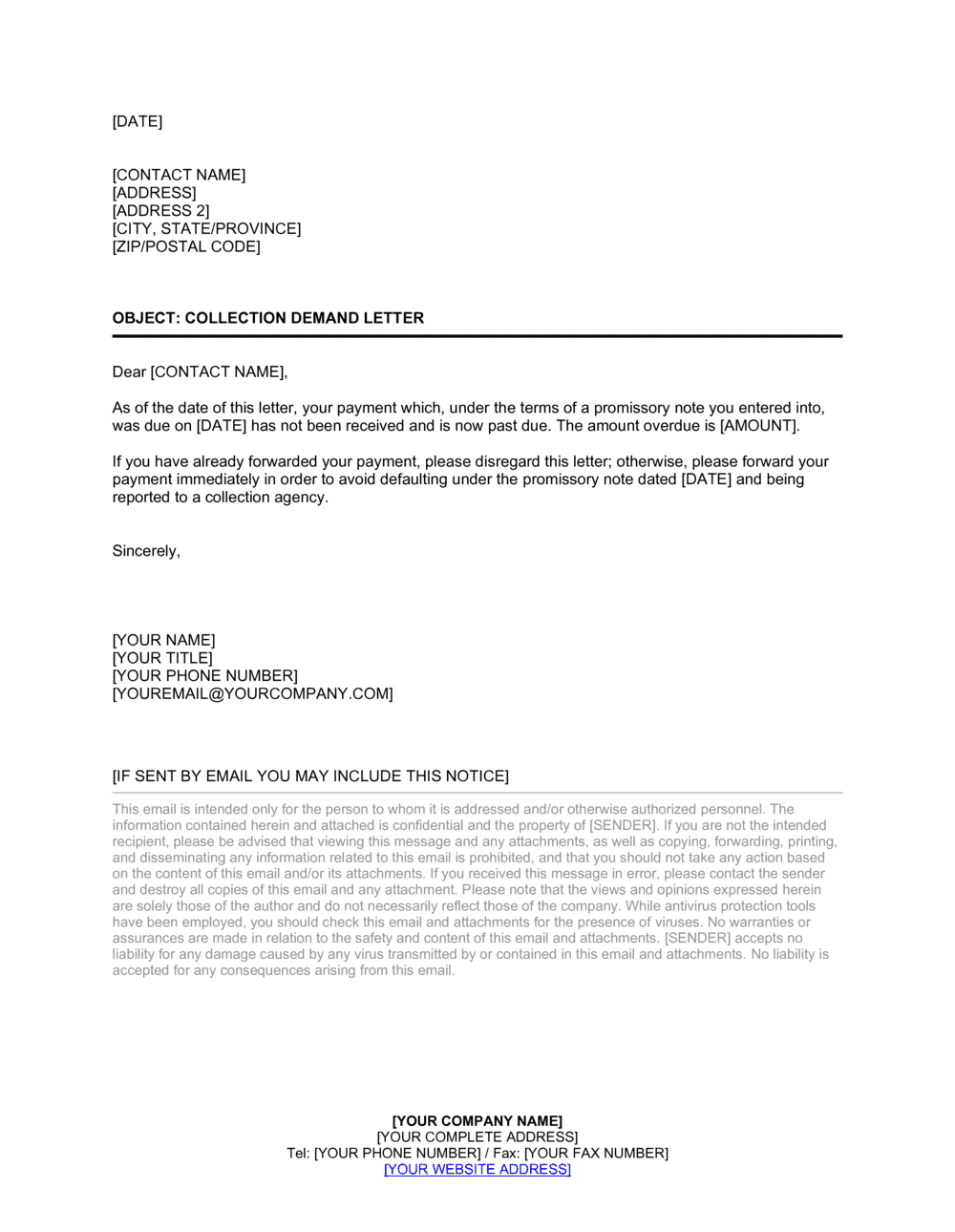

1

Retrieve and review the original promissory note

Locate the signed promissory note and confirm the execution date, principal amount, interest rate, payment schedule, late fee terms, and any acceleration or cure-period clauses. Every figure in the collection letter must trace back to the signed note.

💡 Make a photocopy of the note to attach to your records — if this escalates to court, you will need the original signed document as evidence.

2

Calculate the total amount outstanding

Tally the unpaid principal, interest accrued from the last payment date to today at the note's stated rate, and any late fees expressly authorized by the note. Do not include fees not specified in the note.

💡 Use a simple interest formula: Principal × Annual Rate ÷ 365 × Days Elapsed. Document your calculation in a separate worksheet in case the borrower disputes the amount.

3

Enter the borrower's full legal name and address

Use the borrower's name exactly as it appears on the original promissory note. Send the letter to the borrower's last known address and, if different, their registered business address.

💡 Send by both certified mail (return receipt requested) and first-class mail to create a record of delivery. Some jurisdictions require certified mail to trigger statutory cure periods.

4

Identify and cite the promissory note precisely

Reference the note by its full execution date and original principal amount in the opening paragraph. If the note has a title or reference number, include it.

💡 Quoting the specific section numbers of the note's payment, default, and acceleration clauses strengthens the legal basis of the demand and signals to the borrower — and any subsequent court — that the creditor knows the document well.

5

Set a specific repayment deadline

Choose a cure period that meets or exceeds what the note requires and any applicable statutory minimum — typically 10 to 30 days from the letter date. State the exact calendar date, not a relative timeframe like '15 days from receipt.'

💡 Use the letter's date, not the expected delivery date, as the starting point for the cure period — this is more defensible if delivery timing is disputed.

6

State consequences clearly and accurately

List only the collection actions you are legally authorized to take under the note and applicable law — civil lawsuit, collections referral, or credit reporting. Do not threaten criminal prosecution, arrest, or wage garnishment before obtaining a judgment.

💡 If you are a business collecting a commercial debt, FDCPA restrictions may not apply directly, but state consumer protection laws often do — verify the applicable rules before drafting this section.

7

Sign, date, and send the letter by certified mail

Sign the letter as the payee named in the promissory note, or include an explicit statement of authority if signing as an agent or assignee. Date the letter on the day it is mailed and retain a copy.

💡 Keep the certified mail receipt and delivery confirmation with the letter copy in a dedicated file — these become your proof of notice if the collection escalates to a lawsuit.