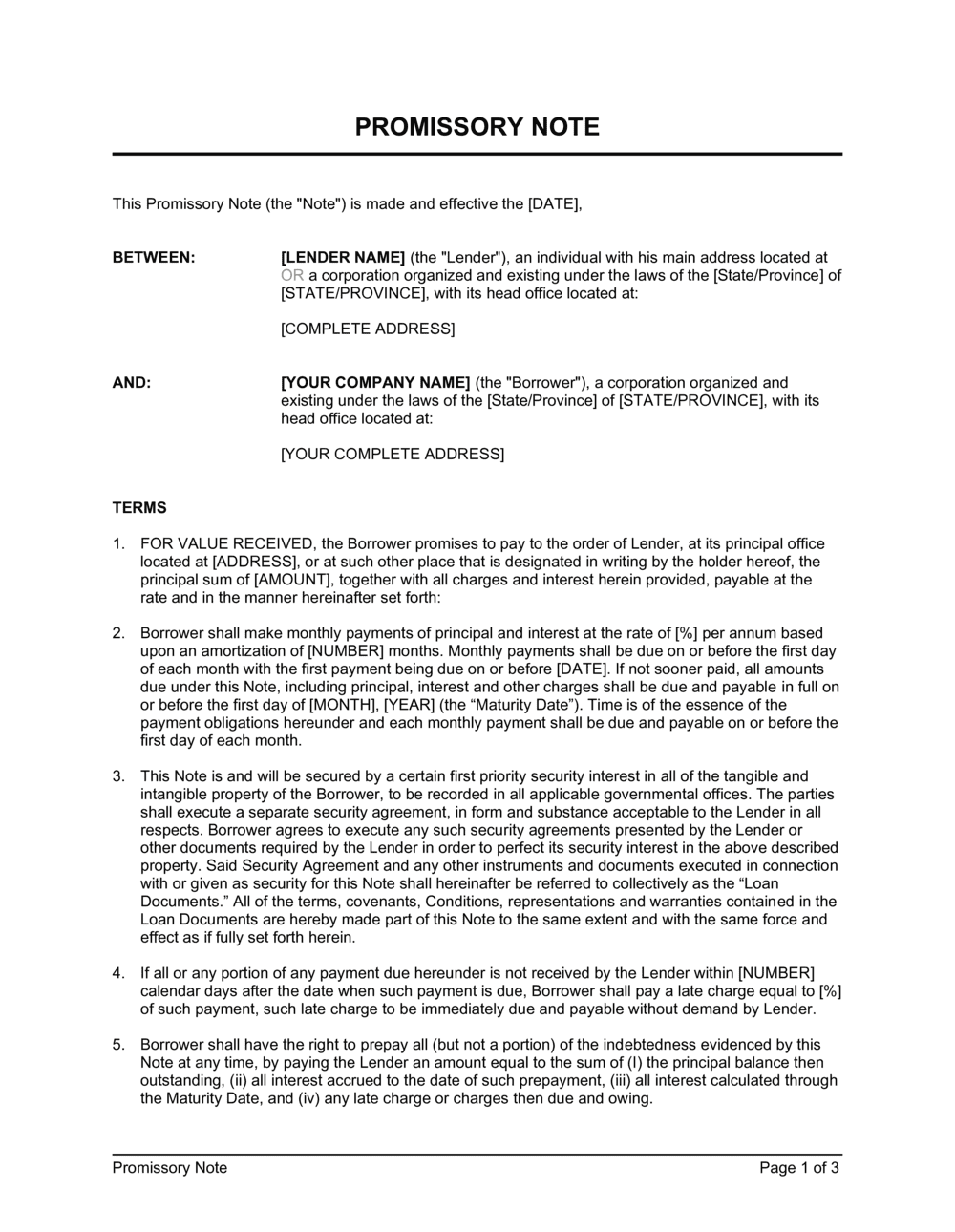

1

Identify parties with full legal names

Enter the borrower's and lender's complete legal names — registered entity names for businesses, full legal names for individuals — and their current addresses.

💡 For an LLC or corporation as borrower, confirm the exact name on the current state or provincial registration to avoid a mismatch that could complicate enforcement.

2

State the principal amount and disbursement date

Enter the loan amount in both words and figures, and record the actual date funds are transferred. If funds are disbursed in multiple tranches, consider using a schedule of advances rather than a single date.

💡 Writing the amount in words and figures protects against alteration disputes — courts default to the written-out amount if the two conflict.

3

Set the interest rate and confirm it is below the usury ceiling

Enter the annual interest rate, specify whether it is fixed or variable, and confirm it does not exceed the maximum rate allowed in the governing jurisdiction for this loan type and amount.

💡 US state usury limits for commercial loans range from roughly 16% to 25% per annum; consumer loans are often capped lower. Check your state's current limit before drafting.

4

Define the repayment schedule precisely

Choose between a lump-sum maturity payment or a periodic installment schedule. For installments, run an amortization calculation to confirm the payment amount fully retires the balance by the maturity date.

💡 Include the first and last payment dates explicitly — 'monthly beginning on [DATE]' is clearer than 'monthly' alone and prevents disputes over when the clock starts.

5

Complete the default and acceleration provisions

List all events of default, including missed payment (with a defined cure period), insolvency, and assignment without consent. Confirm the acceleration language gives the lender discretionary — not automatic — acceleration to preserve flexibility.

💡 A discretionary acceleration right (lender 'may' declare the balance due) is generally more favorable than an automatic trigger, which can create unintended consequences in technical-default situations.

6

Add collateral reference if the note is secured

Describe the pledged asset, reference the accompanying security agreement, and note the lender's intent to file a perfection document. For real property, attach a deed of trust or mortgage reference instead of a UCC filing.

💡 File the UCC-1 or PPSA registration within 20 days of the loan date to protect priority against other creditors from the original advance date.

7

Choose governing law tied to a real connection

Select the state or province where the lender is located, where the borrower operates, or where the primary collateral is situated. Avoid choosing a low-regulation jurisdiction with no genuine connection to the transaction.

💡 For consumer loans, apply the consumer-protection law of the borrower's state regardless of the chosen governing law — courts routinely override choice-of-law clauses that disadvantage consumers.

8

Execute with wet or electronic signatures before funds are disbursed

Both parties must sign before or simultaneously with the transfer of funds. Date the note to reflect the actual signing date. For corporate borrowers, ensure the signatory has authorization — a board resolution or operating-agreement authority — to bind the entity.

💡 Keep a fully executed copy in a secure document repository and record the note number in your loan register. Lenders who cannot produce the original signed note face enforceability challenges in some jurisdictions.