1

Identify all three parties with legal names

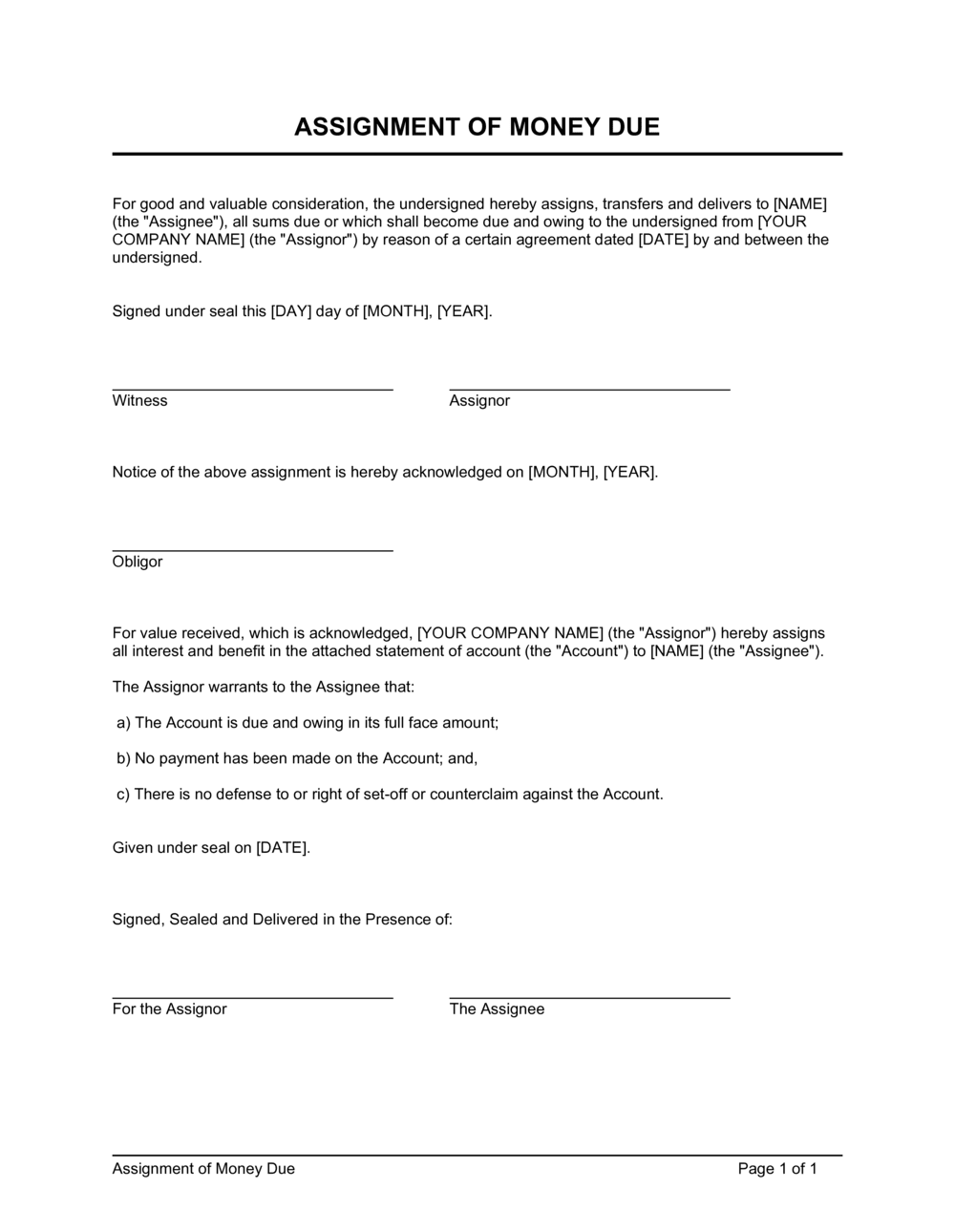

Enter the full registered legal name, address, and entity type for the Assignor, Assignee, and Debtor. Confirm the Debtor's current mailing address — this is where the notice of assignment must be sent.

💡 Pull the Debtor's name directly from the original contract or invoice to ensure it matches exactly — a discrepancy can give the Debtor grounds to dispute the validity of the notice.

2

Describe the assigned debt precisely

Reference the specific invoice number, contract date, or agreement title that created the debt. State the exact outstanding balance and any accrued interest rate. Attach a copy of the underlying document as an exhibit.

💡 If multiple invoices are being assigned together, list each one in a numbered schedule attached to the agreement rather than describing them in the body — this keeps the main document clean and makes future disputes easier to resolve.

3

State the consideration clearly

Enter the actual dollar amount the Assignee is paying for the right to collect the debt, or describe another form of consideration such as debt forgiveness. Avoid 'nominal' consideration of $1 for assignments of material value — it can attract fraudulent-transfer scrutiny.

💡 If the assignment is being used to satisfy a separate obligation the Assignor owes the Assignee, describe that offset clearly as the consideration rather than leaving it implied.

4

Complete the representations and warranties block

Confirm each warranty is accurate before signing: the debt is genuinely outstanding, it has not been pledged or previously assigned, and you are not aware of any disputes or setoffs the Debtor may raise.

💡 Run a UCC lien search (US) or equivalent in your jurisdiction before executing — if the receivable is already collateral for a bank loan, you cannot validly assign it without the lender's consent.

5

Set the notice deadline and prepare the notice document

Enter the number of business days within which notice must be delivered to the Debtor after execution — 5 business days is standard. Draft the notice letter (Exhibit A) at the same time you complete the agreement so it is ready to send immediately.

💡 Send the notice by a trackable method — certified mail, courier, or email with read receipt — and retain proof of delivery. The date the Debtor receives notice is the date from which their obligation to pay the Assignee begins.

6

Elect recourse or non-recourse and complete the applicable clause

Decide whether the Assignor will guarantee payment if the Debtor defaults. If recourse, specify the number of days after the due date before the Assignee can demand payment from the Assignor. If non-recourse, state it explicitly.

💡 Non-recourse assignments typically command a lower purchase price because the Assignee bears the credit risk — price the consideration accordingly.

7

Sign before delivering notice to the Debtor

Both the Assignor and Assignee must sign the agreement before the notice is delivered. The signed agreement is the foundation of the Assignee's right to collect — notice without an executed agreement behind it is legally ineffective.

💡 Use a timestamped electronic signature so the execution date is independently verifiable if the Debtor later claims the notice was premature.

8

Retain executed copies and file any required security interest

Both parties should retain a fully executed copy. In the US, if the assigned receivable is material and the Assignee wants priority over other creditors, file a UCC-1 financing statement in the Assignor's state of organization.

💡 Set a calendar reminder for the UCC-1 continuation filing deadline — financing statements lapse after 5 years if not renewed, which could subordinate the Assignee's claim in an insolvency.