- Due Diligence

- The investigative process a buyer, investor, or lender undertakes to verify the accuracy of a target's representations and identify material risks before closing a transaction.

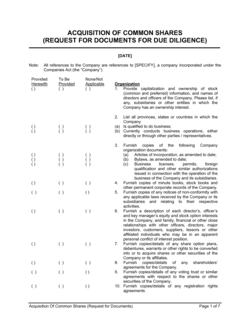

- Requisition List

- A formal, numbered list of documents and information a requesting party asks the target to produce, typically organized by category.

- Virtual Data Room (VDR)

- A secure, cloud-hosted repository where the target uploads diligence documents for the requesting party to review without sharing physical copies.

- Letter of Intent (LOI)

- A non-binding preliminary agreement outlining the key terms of a proposed transaction, after which formal due diligence typically begins.

- Material Contract

- Any agreement that is significant to a target company's business operations — typically defined by dollar threshold, strategic importance, or change-of-control provisions.

- Representations and Warranties

- Factual statements made by the seller in the purchase agreement about the state of the business; due diligence verifies whether these statements are true.

- Change of Control Clause

- A contract provision that allows a counterparty to terminate or renegotiate the agreement if ownership of one party changes — a key diligence flag in material contracts.

- Indemnification

- A contractual obligation by the seller to compensate the buyer for losses arising from breaches of representations discovered after closing.

- Cap Table

- A spreadsheet listing all equity owners, their ownership percentages, and outstanding options or warrants — a standard first request in any equity transaction.

- Data Room Index

- A master list of all documents uploaded to the virtual data room, organized to mirror the requisition list categories so reviewers can locate materials quickly.

- Escrow

- A portion of the purchase price held by a neutral third party after closing to cover post-closing indemnification claims by the buyer.

- MAC / MAE Clause

- Material Adverse Change or Material Adverse Effect — a provision allowing a buyer to walk away from a deal if a significant negative development occurs between signing and closing.