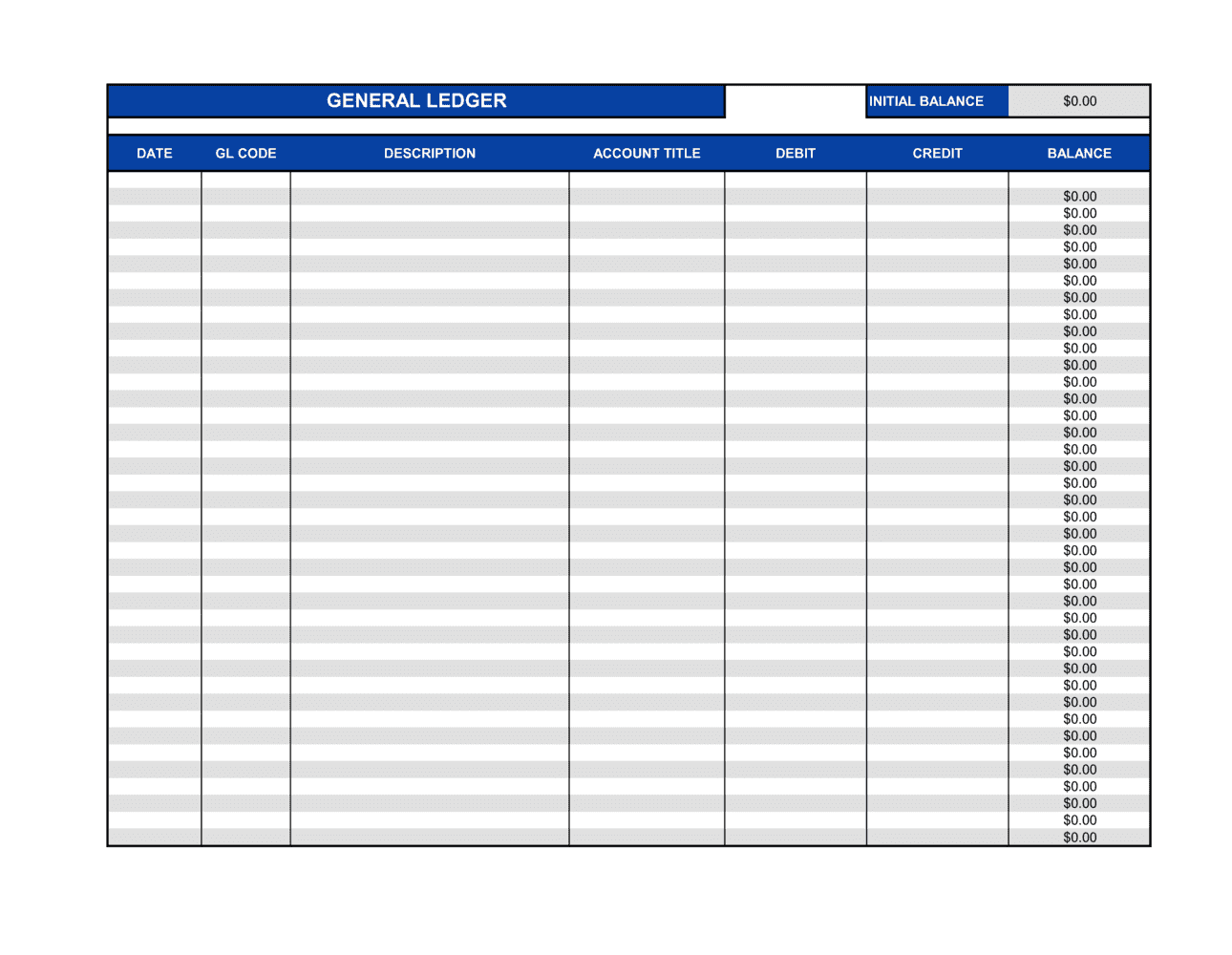

- Chart of Accounts

- A numbered list of every account used by a business, organized by category — assets, liabilities, equity, revenue, and expenses — that forms the structure of the general ledger.

- Double-Entry Bookkeeping

- An accounting method where every transaction is recorded as both a debit in one account and an equal credit in another, keeping the accounting equation in balance.

- Debit

- An entry that increases asset and expense accounts or decreases liability, equity, and revenue accounts — always recorded in the left column of a ledger entry.

- Credit

- An entry that increases liability, equity, and revenue accounts or decreases asset and expense accounts — always recorded in the right column of a ledger entry.

- Journal Entry

- The original record of a transaction, noting the date, accounts affected, amounts, and a brief description, before the amounts are posted to the general ledger.

- Trial Balance

- A summary report listing all general ledger account balances at a point in time, used to verify that total debits equal total credits before preparing financial statements.

- Account Code

- A numeric or alphanumeric identifier assigned to each ledger account for consistent classification and retrieval, typically following a standard numbering convention such as 1000s for assets, 2000s for liabilities.

- Posting

- The process of transferring amounts from journal entries into the corresponding general ledger accounts, updating each account's running balance.

- Reconciliation

- The process of comparing general ledger account balances against external records — bank statements, invoices, or subsidiary ledgers — to identify and resolve discrepancies.

- Closing Entries

- Period-end journal entries that transfer balances from temporary revenue and expense accounts to the retained earnings equity account, resetting those accounts to zero for the next period.

- Subsidiary Ledger

- A detailed ledger supporting a single control account in the general ledger — for example, individual customer balances that roll up into the accounts receivable control account.