1

Gather source documents for the period

Collect the official bank statement for the reconciliation period, the company's general ledger cash account detail for the same period, and the prior period's completed reconciliation to confirm the opening balance.

💡 Download the bank statement directly from the bank's portal as a PDF rather than relying on a CSV export — the PDF is the auditor-accepted source document.

2

Complete the account identification and period header

Enter the company's legal name, bank name, account type, last four digits of the account number, and the precise start and end dates of the reconciliation period.

💡 If you reconcile multiple accounts, use a separate form for each — never combine two accounts on a single reconciliation even if they are at the same bank.

3

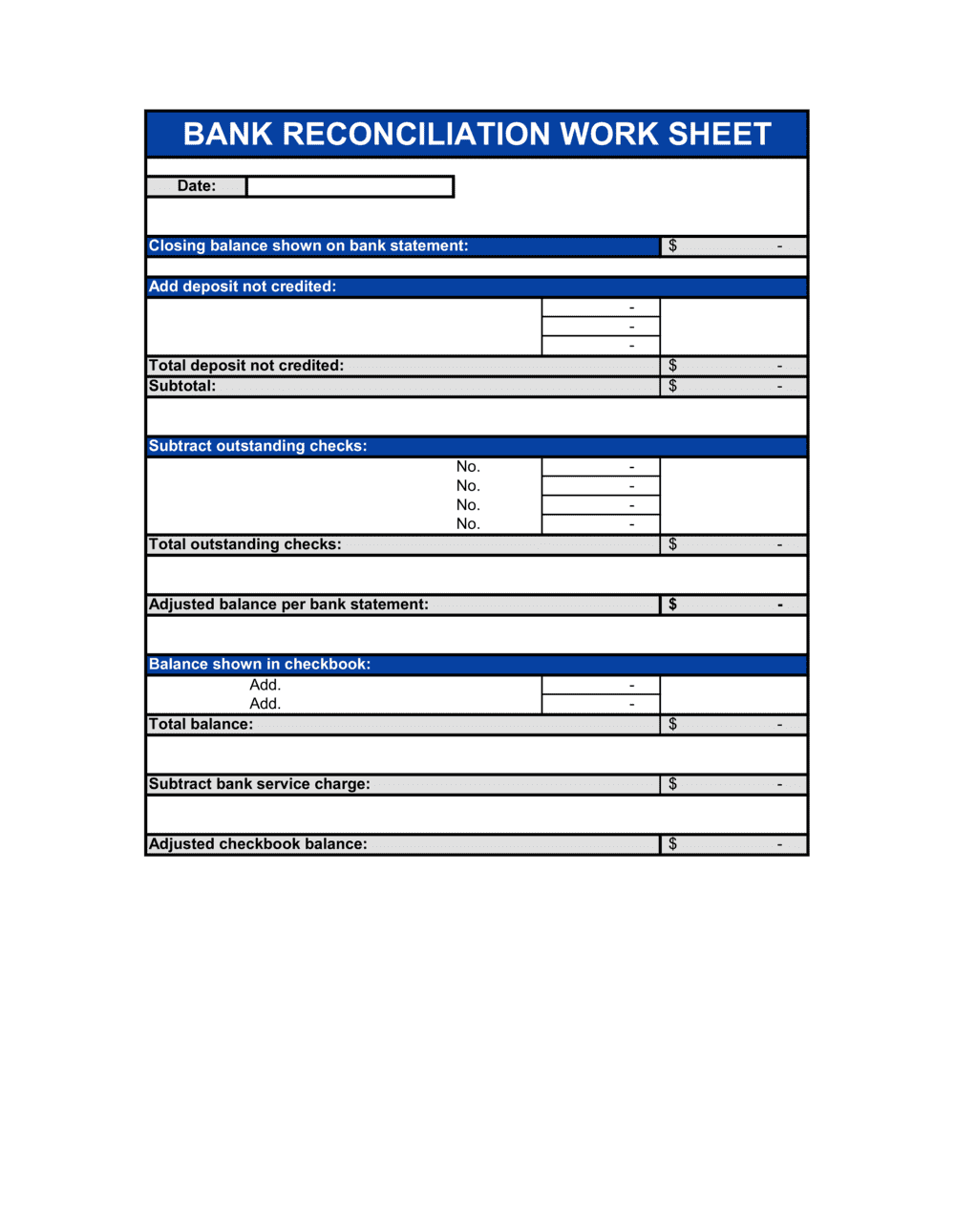

Confirm the opening balances agree

Compare the book opening balance (prior period's adjusted book balance) to the bank statement's opening balance. Document any variance before proceeding — do not carry forward unexplained prior-period differences.

💡 If opening balances do not agree, re-open the prior period's reconciliation first. A carry-forward error compounding into the current period doubles the investigation time.

4

List all outstanding checks

Pull every check recorded in the ledger that does not appear as cleared on the bank statement. Enter check number, date, payee, and amount for each item, then total the list.

💡 Flag any check outstanding for more than 60 days. Investigate before certifying — long-outstanding checks may indicate a lost instrument, a stopped payment, or a fraudulent recording.

5

List all deposits in transit

Identify deposits recorded in the books before the period-end cut-off that do not appear on the bank statement. Enter the deposit date, reference, and amount for each, then total.

💡 Cross-reference deposits in transit against the next month's bank statement to confirm they cleared. If a prior-period deposit in transit still hasn't cleared after 10 business days, escalate immediately.

6

Record bank charges, NSF items, and interest

Scan the bank statement for service charges, wire fees, NSF reversals, and interest credits not yet in the ledger. List each item with its date and amount, then prepare the corresponding journal entries.

💡 Do not post journal entries until the reconciliation is reviewed and approved — premature posting makes it impossible to retrace the reconciliation if the reviewer finds an error.

7

Document and investigate any book or bank errors

List every discrepancy that cannot be explained by a timing difference. For book errors, cross-reference the journal entry that corrects it. For bank errors, note the date you contacted the bank and the expected correction date.

💡 Keep a running discrepancy log separate from the main form. This log becomes evidence for the auditor if the error takes more than one period to resolve.

8

Verify adjusted balances are equal and obtain signatures

Calculate the adjusted bank balance and adjusted book balance. Confirm they match to the cent. Have the preparer sign, then route to a separate reviewer for independent approval and signature.

💡 Never certify a reconciliation with a residual balance and a note saying 'under investigation' — document the open item in the discrepancy log and certify only after the discrepancy is resolved or formally escalated.