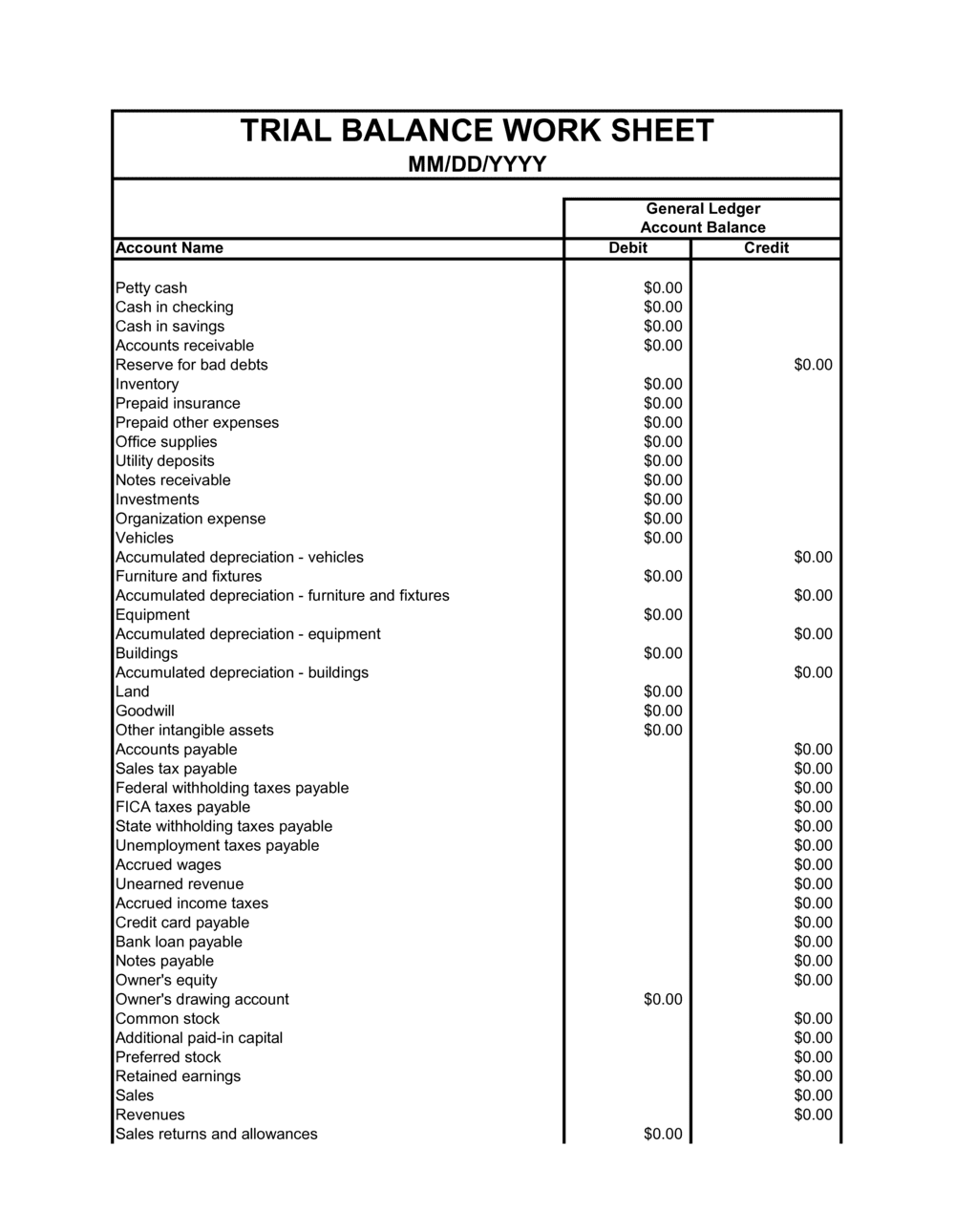

- General Ledger

- The master record of all financial transactions in a business, organized by account — the source data that a trial balance summarizes.

- Debit

- An entry that increases asset or expense accounts and decreases liability, equity, or revenue accounts.

- Credit

- An entry that increases liability, equity, or revenue accounts and decreases asset or expense accounts.

- Double-Entry Bookkeeping

- An accounting system in which every transaction affects at least two accounts, keeping total debits equal to total credits at all times.

- Unadjusted Trial Balance

- A trial balance produced directly from the general ledger before any period-end adjusting entries — such as accruals or depreciation — are posted.

- Adjusted Trial Balance

- A trial balance produced after all adjusting journal entries have been posted, used as the direct input to the formal financial statements.

- Closing Entry

- A journal entry made at year-end to transfer balances from temporary accounts (revenue, expense, dividends) to retained earnings, resetting them to zero.

- Chart of Accounts

- A numbered list of every account used in a company's general ledger, providing the structure that a trial balance follows.

- Accrual

- Revenue or expense recognized in the period it is earned or incurred, regardless of when cash changes hands — a common source of period-end adjusting entries.

- Suspense Account

- A temporary holding account used when a transaction cannot immediately be assigned to the correct account — a non-zero suspense balance flags an error on the trial balance.