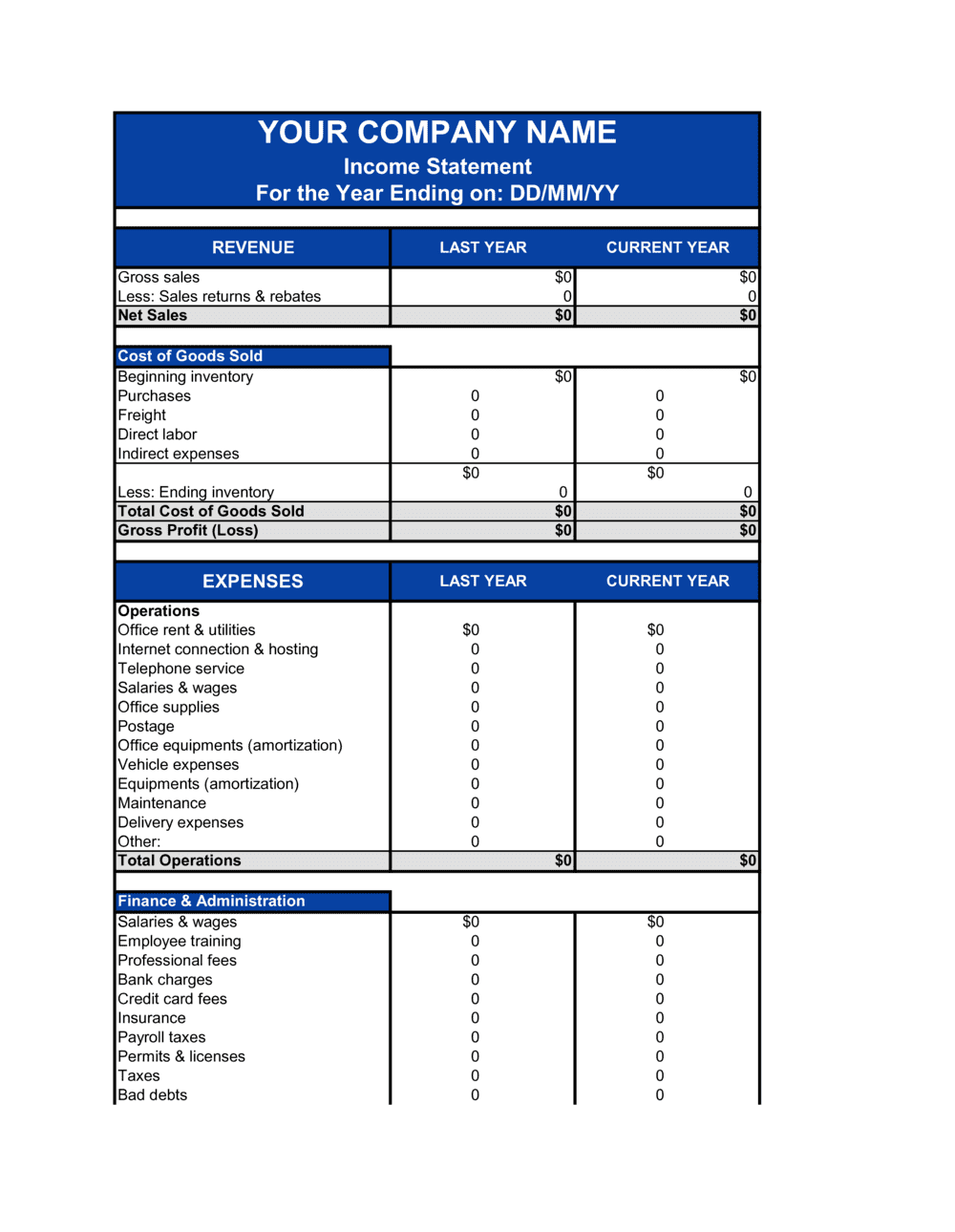

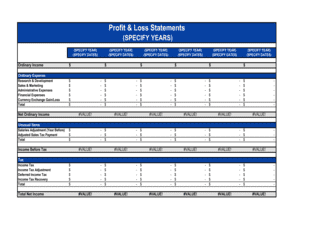

- Revenue (Net Sales)

- Total income from the sale of goods or services after deducting returns, allowances, and discounts — the top line of the income statement.

- Cost of Goods Sold (COGS)

- Direct costs attributable to producing the goods or services sold — including materials, direct labor, and manufacturing overhead.

- Gross Profit

- Revenue minus COGS — the amount left to cover operating expenses, interest, taxes, and generate net income.

- Gross Margin

- Gross profit expressed as a percentage of revenue, used to benchmark efficiency against industry peers.

- Operating Expenses (OpEx)

- Costs incurred in running the business that are not directly tied to production — such as salaries, rent, marketing, and depreciation.

- EBITDA

- Earnings Before Interest, Taxes, Depreciation, and Amortization — a proxy for operating cash generation widely used in valuations and lending covenants.

- Operating Income (EBIT)

- Gross profit minus operating expenses — earnings before the effects of financing decisions and tax obligations.

- Non-Operating Income and Expenses

- Items outside normal business operations, such as interest income, interest expense, foreign exchange gains or losses, and gains on asset sales.

- Income Tax Provision

- The estimated corporate income tax expense for the period, calculated on pre-tax income at the applicable statutory rate plus deferred tax adjustments.

- Net Income (Net Loss)

- The bottom line — total revenue minus all expenses, taxes, and interest for the reporting period.

- Accrual Basis

- Accounting method that records revenue when earned and expenses when incurred, regardless of when cash is received or paid.

- Comparative Period

- A prior period column shown alongside the current period on the income statement to enable trend analysis — typically the prior quarter or prior year.