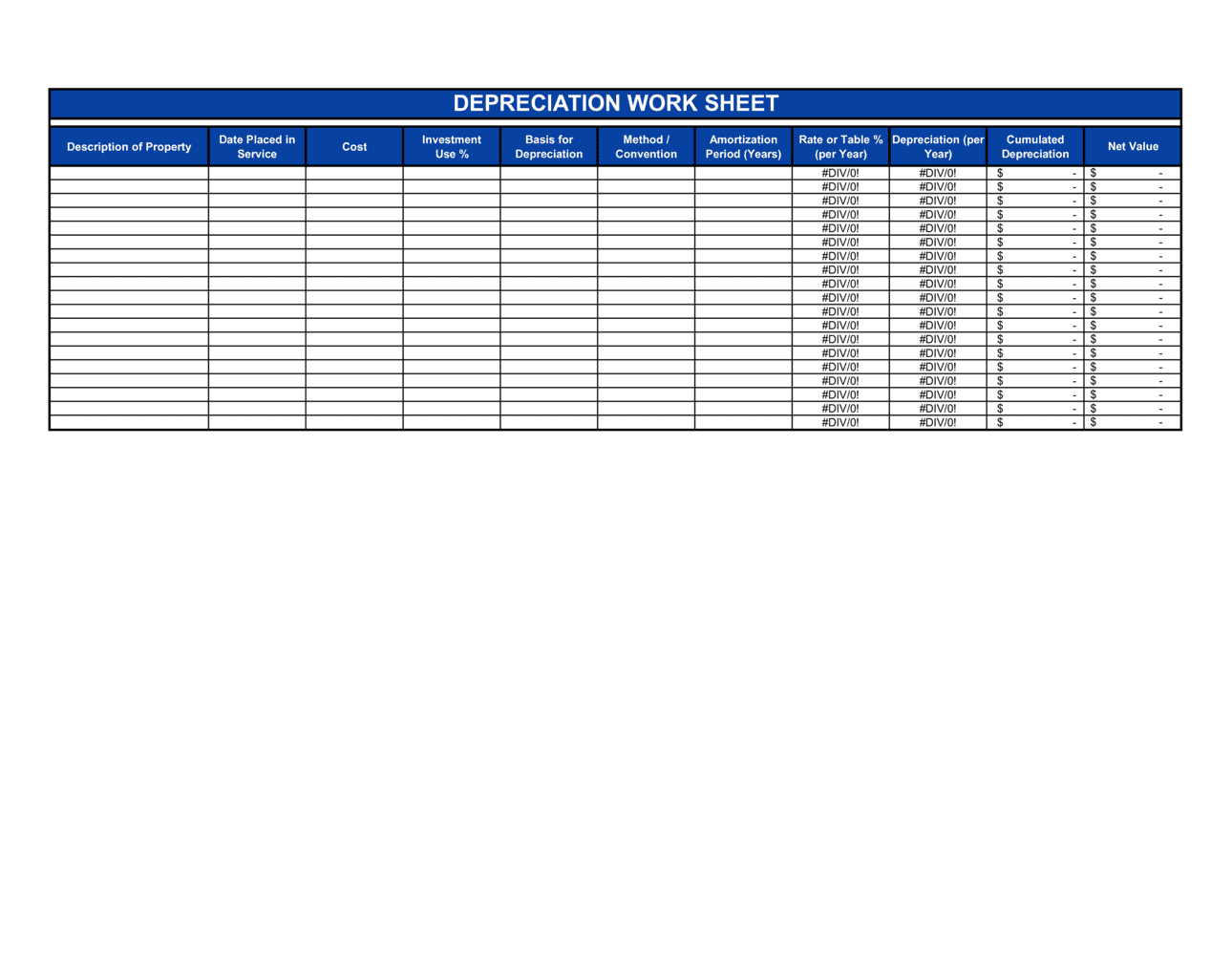

1

Assign a unique asset ID and complete the identification block

Enter a sequential or coded asset identifier, a plain-language description, the asset category (e.g., office equipment, vehicle, leasehold improvement), and the physical location and cost-center code.

💡 Use a coding convention that matches your accounting system — e.g., 'VEH-2026-003' for the third vehicle acquired in 2026 — so the worksheet auto-links to the general ledger.

2

Record the acquisition date and full cost basis

Enter the date the asset was placed in service — not the purchase-order date or invoice date — and sum all capitalized costs: invoice price, freight, installation, testing, and applicable taxes.

💡 For leasehold improvements, include the cost of permits and architect fees in the cost basis; they are depreciable as part of the improvement.

3

Elect and document the depreciation method

Select the method appropriate for the asset class and jurisdiction — straight-line for GAAP book purposes, MACRS for US tax, capital allowances for UK tax. Record the authority (IRC section, accounting policy reference, or HMRC class) in the method field.

💡 Keep book and tax depreciation on separate rows or columns from the start — blending them in a single calculation creates reconciliation headaches at year-end.

4

Set useful life and salvage value

Enter the book useful life in years and, where different, the IRS or statutory recovery period. For book depreciation, record a realistic salvage value based on dealer quotes or historical disposal data — not zero unless supportable.

💡 IRS Publication 946 lists the MACRS class lives for common asset types. Cross-reference it before assigning a recovery period to avoid a class-life mismatch.

5

Calculate and enter annual depreciation for each year

Apply the elected formula to compute each year's depreciation charge. For straight-line: (Cost minus Salvage) ÷ Useful Life. For declining-balance: remaining book value × fixed rate. Carry the exact figures forward without rounding until the final period.

💡 Build the full depreciation table through the asset's entire useful life when you first enter the asset — this surfaces any errors in your useful-life or rate assumptions before they appear in a tax filing.

6

Update accumulated depreciation and net book value at each period close

At each month-end or year-end close, add the current period's charge to accumulated depreciation and subtract from cost basis to derive net book value. Confirm the net book value matches the general ledger balance for that asset account.

💡 A variance between the worksheet's net book value and the GL balance signals an unrecorded addition, disposal, or impairment — investigate before signing financial statements.

7

Record any disposal, sale, or write-off

When an asset is sold, traded in, or written off, enter the disposal date, proceeds, net book value at disposal, and the resulting gain or loss. Remove the asset from the active register and flag it as disposed.

💡 For mid-year disposals, calculate the partial-year depreciation up to the disposal date using the half-year, mid-quarter, or mid-month convention that matches the convention used at acquisition.

8

Obtain preparer and reviewer signatures

Have the person who completed the worksheet sign the attestation block, then route it to a senior accountant, CFO, or authorized officer for review and counter-signature before filing or presenting to third parties.

💡 Date each signature separately — the preparer date and reviewer date should reflect the actual workflow, not be backdated to the period-end date.