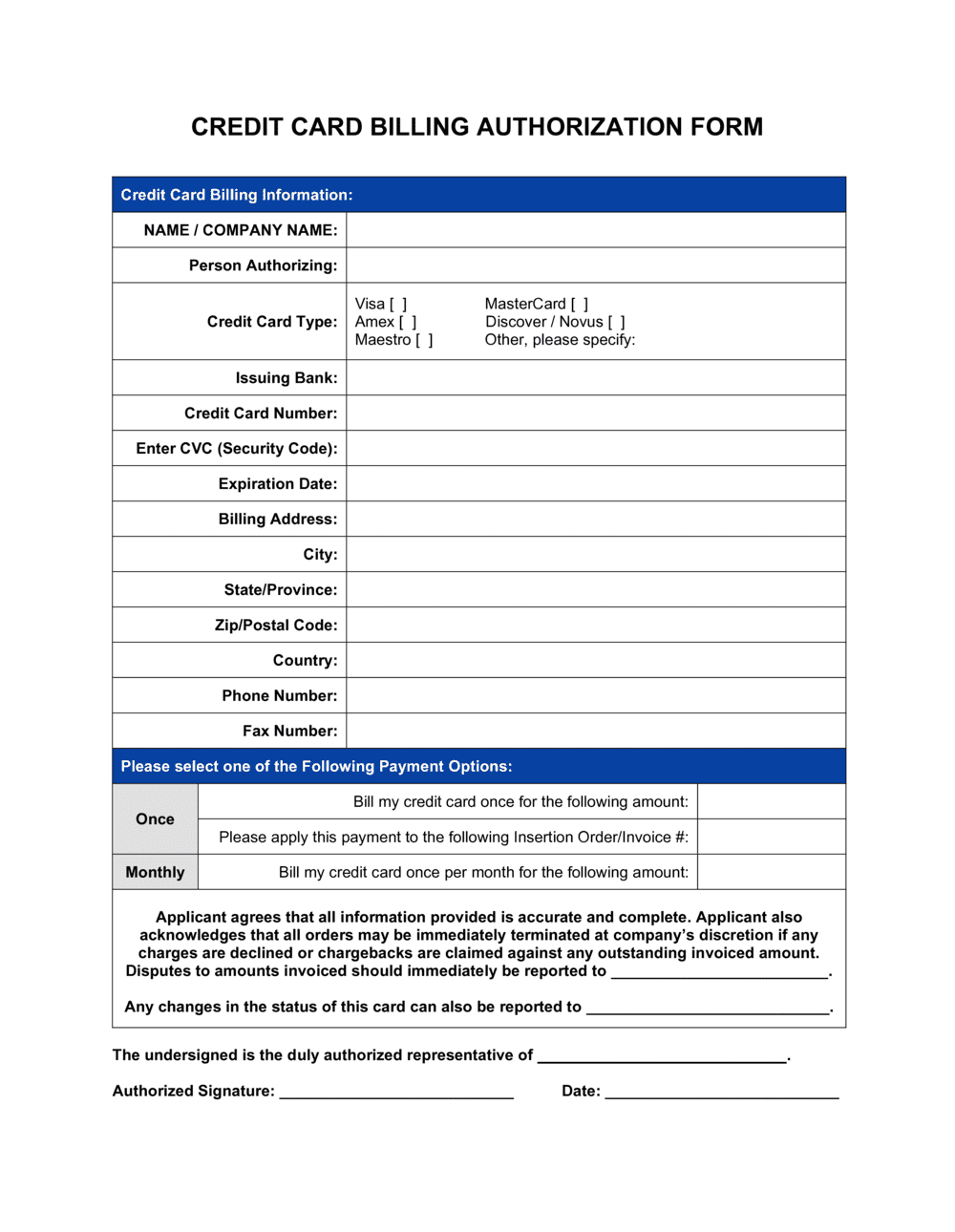

1

Add your merchant business information

Enter your legal business name, address, and contact details at the top of the form. Confirm the business name matches exactly what appears on your payment processor account and customer statements.

💡 Include the descriptor that appears on card statements — if your doing-business-as name differs from your legal name, list both so customers recognize the charge.

2

Collect the cardholder's contact and billing details

Have the customer complete their full legal name, billing address, phone number, and email. The billing address must match the address on file with the card issuer to pass address verification.

💡 For recurring customers, verify the billing address annually — cards expire and customers move, and an outdated address causes AVS failures on renewal charges.

3

Record the card type, number, and expiration

Capture the card network, the full card number (for initial processing), and the expiration date. Once the card is entered into your payment system, redact all but the last four digits on the paper form.

💡 Never store forms with full card numbers in a standard filing cabinet — use a locked, access-controlled location and shred forms once the data is in your PCI-compliant processor.

4

Specify the authorized amount and billing frequency

Enter the exact dollar amount per charge, whether the authorization is one-time or recurring, the billing interval, and the date of the first charge.

💡 If the amount may vary (e.g., utility-style billing), state a maximum authorized amount per transaction and require re-authorization when charges exceed that ceiling.

5

Describe the purpose of the charge

Write a plain-English description of the product or service being billed. Use the same language that will appear on the customer's card statement.

💡 If your payment processor allows a custom statement descriptor, coordinate the wording so the form description and the statement entry match exactly.

6

Include cancellation and modification terms

State the number of days' notice required to cancel or modify the authorization and the exact method (email, phone, or written letter) the cardholder must use.

💡 A 10-business-day notice window is standard for monthly billing — shorter windows reduce friction; longer windows increase chargeback risk when customers feel trapped.

7

Obtain a dated signature and file the form securely

Have the cardholder sign and date the completed form before processing any charge. Store the signed form — physically or digitally — for a minimum of 18 months after the last transaction.

💡 For remote customers, use an e-signature tool so the authorization is timestamped and tamper-evident, making it far easier to contest a chargeback with the card network.