1

Enter the creditor's and debtor's full legal details

Add the full registered legal name and address of your business as the creditor, and the debtor's full legal name, company name if applicable, and last known billing address.

💡 Use the exact name and address from your original contract or invoice — inconsistencies can create enforcement difficulties if the matter reaches court.

2

Reference all prior collection notices with dates and reference numbers

List the dates and reference or tracking numbers of every prior collection notice sent. This establishes the escalation history and confirms the debtor had ample opportunity to pay.

💡 Keep copies of all prior notices on file with proof of delivery — email receipts, certified mail tracking numbers, or courier confirmation — before sending the final letter.

3

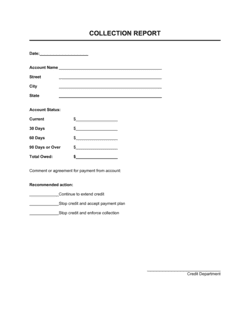

State the outstanding balance with full itemization

Enter the original invoice number and amount, the original due date, any accrued interest or late fees calculated at the contracted rate, and the current total due. Confirm the math is exact.

💡 If interest has accrued daily, calculate it to the date of the letter and note the per-diem rate so the debtor can calculate any additional amount owed if they pay late.

4

Set a firm, specific final payment deadline

Choose a deadline that gives the debtor a reasonable but firm window — typically 7 to 14 days from the letter date. State the exact calendar date, not a relative term like 'within two weeks.'

💡 In some jurisdictions, consumer debt collection laws require a minimum notice period before referral to a collections agency or credit reporting. Check applicable rules before setting a deadline under 7 days.

5

List the specific consequences of non-payment

State clearly and only what you actually intend to do if the deadline passes — litigation, collections agency referral, or credit bureau reporting. Do not include consequences you have no authority or intention to pursue.

💡 If your original contract or service agreement includes an attorney's fees clause, reference it here — it significantly increases the debtor's financial incentive to pay before you file.

6

Provide complete payment instructions

Include at least two payment methods — bank transfer with routing and account numbers, certified check with mailing address, or a direct payment portal link — directly in the body of the letter.

💡 Assign the original invoice number as the payment reference so the funds are matched to the correct account immediately upon receipt.

7

Sign and date the letter before sending

Have an authorized signatory — owner, CFO, or legal representative — sign the letter by name and title. Add the date of issuance, which starts the clock on the debtor's response window.

💡 Send the final letter via at least two methods — certified mail with return receipt and email with read receipt — so you have documented proof of delivery for any subsequent legal filing.

8

Log the letter and set a follow-up trigger

Record the letter date, delivery confirmation, and deadline date in your accounts receivable system. Set a calendar reminder one business day after the deadline to initiate the next action immediately if payment has not been received.

💡 Do not extend the deadline after sending unless the debtor has reached out and agreed to a documented payment arrangement. Repeated deadline extensions undermine the credibility of future demands.