- Authorizing Party

- The individual or entity whose credit information is being released — the person or business giving permission.

- Recipient

- The organization or person authorized to receive the credit information, such as a lender, landlord, or employer.

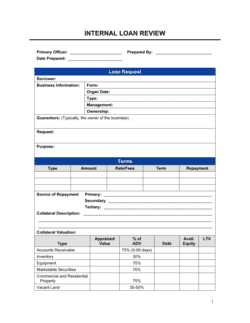

- Credit Report

- A detailed record of a person's or business's borrowing and repayment history compiled by a credit reporting bureau.

- Credit Bureau

- An agency that collects, maintains, and supplies credit history data — in the US, the major bureaus are Equifax, Experian, and TransUnion.

- Scope of Release

- The specific categories of credit data covered by the authorization, such as credit score, payment history, outstanding balances, or judgments.

- FCRA (Fair Credit Reporting Act)

- US federal law governing how consumer credit information may be collected, accessed, and used — requiring written consent before most credit pulls.

- Permissible Purpose

- A legally recognized reason under the FCRA for obtaining a credit report, including credit transactions, employment, and tenancy screening.

- Hard Inquiry

- A credit report pull that is recorded on the subject's credit file and can temporarily affect their credit score — typically triggered by a formal lending application.

- Soft Inquiry

- A credit check that does not affect the subject's credit score and is not visible to other lenders — used for pre-qualification and background checks.

- Revocation of Consent

- The act of withdrawing a previously granted authorization, typically in writing, before the authorized party has acted on it.

- Duration of Authorization

- The period during which the authorization remains valid, commonly expressed as a specific number of days from the signature date.