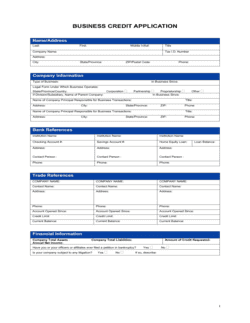

- Trade Reference

- A supplier, vendor, or creditor listed by a credit applicant who can confirm their payment history and account standing.

- Open Account

- A credit arrangement where goods or services are delivered before payment is due, with settlement expected within agreed net terms.

- Net Terms

- The number of days a buyer has to pay an invoice in full — for example, Net 30 means payment is due 30 days from the invoice date.

- Credit Limit

- The maximum outstanding balance a creditor will allow a customer to carry at any one time under open-account terms.

- Payment History

- A record of whether a customer paid invoices on time, late, or not at all, typically covering the most recent 12–24 months.

- Days Sales Outstanding (DSO)

- The average number of days it takes a customer to pay an invoice, used as a proxy for payment reliability.

- Credit Inquiry

- A formal request by one party to obtain credit-related information about another party from a reference or reporting agency.

- Confidentiality Assurance

- A statement in the request letter promising that the reference's response will be used solely for credit-evaluation purposes and not shared further.

- High Credit

- The highest outstanding balance a customer has carried with a supplier at any single point, used to indicate the scale of the relationship.

- Account Standing

- A summary assessment of whether a customer's account is current, past due, placed for collection, or closed in good standing.