- Principal

- The original amount of money borrowed, before interest or fees are added.

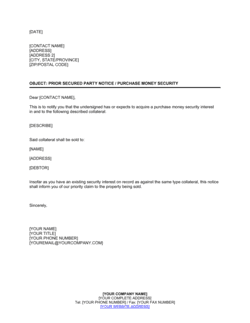

- Security Interest

- A lender's legal right to take and sell specific collateral if the borrower fails to repay the debt.

- Collateral

- An asset pledged by the borrower to the lender as security for a loan — the lender may seize it upon default.

- Amortization

- The process of spreading loan repayment over a schedule of fixed installments, each covering both principal reduction and interest.

- Acceleration Clause

- A provision that makes the entire outstanding loan balance immediately due and payable upon a defined default event.

- Default

- A borrower's failure to meet any material obligation under the note — typically a missed payment, insolvency, or breach of a covenant.

- Cure Period

- A defined number of days after a default notice within which the borrower may correct the default before the lender exercises remedies.

- UCC Financing Statement (UCC-1)

- A public filing under the Uniform Commercial Code that gives notice to third parties of a lender's security interest in personal property collateral.

- Per Annum Interest Rate

- The annual rate of interest applied to the outstanding principal balance, stated as a percentage and used to calculate each installment's interest component.

- Prepayment Penalty

- A fee charged to the borrower for repaying some or all of the principal ahead of schedule, compensating the lender for lost future interest.

- Maturity Date

- The date on which the final installment is due and all remaining principal and accrued interest must be fully repaid.

- Recourse

- The lender's right to pursue the borrower's personal or other assets beyond the pledged collateral if the collateral's value is insufficient to cover the outstanding debt.