1

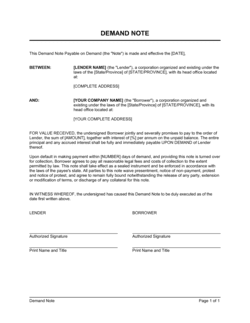

Enter the legal names and addresses of both parties

Use the borrower's and lender's full legal names — for companies, the registered entity name — and their current mailing addresses. If the borrower is signing in a personal capacity as guarantor of a business debt, note that distinction explicitly.

💡 Run a quick corporate registry search to confirm the borrower entity's exact registered name before filling in the parties clause.

2

State the principal amount in both words and figures

Write the loan amount in full words followed by the numeral in parentheses and specify the currency. Record the actual date the money was or will be advanced, not the date the note is signed if they differ.

💡 If the loan is being advanced in tranches, consider attaching a draw schedule rather than trying to capture multiple advance dates in the body of the note.

3

Set the interest rate and confirm it is within usury limits

Enter the annual interest rate and specify whether it compounds or accrues as simple interest. Before finalizing, verify the applicable usury ceiling for the governing jurisdiction — federal and state or provincial limits differ for commercial vs. consumer loans.

💡 For zero-interest loans between related parties, consult a tax advisor first. Tax authorities in the US, Canada, and the UK may impute a market interest rate on below-market loans between related entities.

4

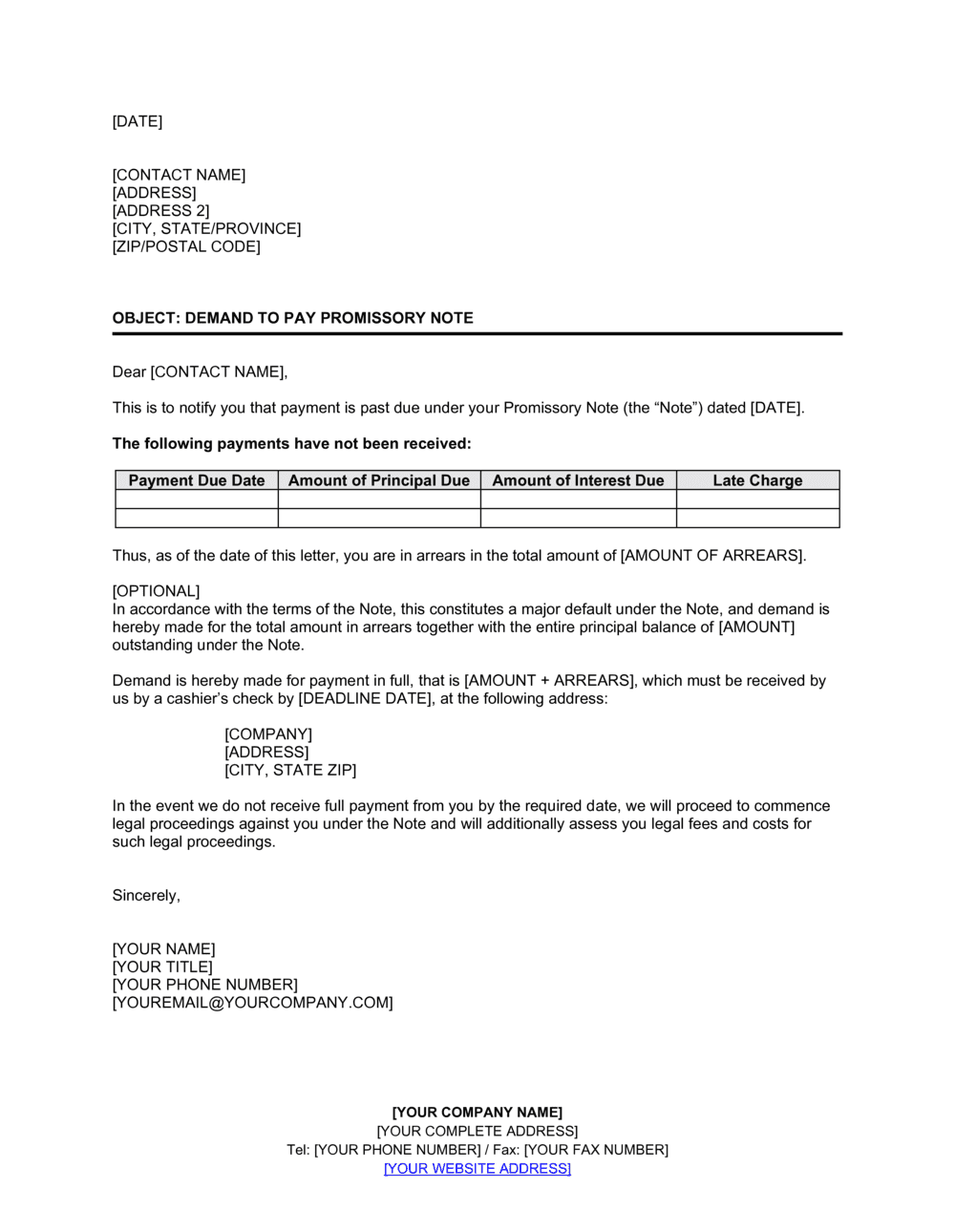

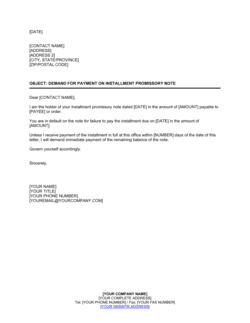

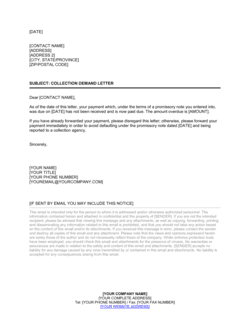

Define the demand and grace period mechanics

Specify that demand must be in writing and state the delivery method — email with read receipt, certified mail, or courier. Then set the grace period in business days (typically 5–10 days for commercial loans, up to 30 days for personal ones).

💡 Include both parties' email addresses in a notices clause so there is no dispute about where written demand must be sent.

5

List all events of default

Beyond non-repayment after demand, include insolvency events, assignment for the benefit of creditors, and commencement of bankruptcy or receivership proceedings. For corporate borrowers, add change of control as a default trigger if the lender's decision to lend was based on specific ownership.

💡 Review the borrower's existing debt obligations before finalizing default triggers — conflicting default clauses across multiple notes can create unintended cross-default situations.

6

Include the fee-shifting and waiver clauses

Confirm the costs-of-collection clause specifying attorneys' fees is in the note, and retain the presentment waiver. These two clauses materially improve the lender's enforcement position if the borrower defaults.

💡 Some US states limit or disallow contractual attorney-fee provisions in consumer loan agreements — verify applicability before including the clause.

7

Choose and confirm the governing law

Select the jurisdiction whose law will govern the note — typically where the lender is located or where the borrower operates. Ensure the chosen state or province has a usury ceiling that accommodates your interest rate.

💡 If the borrower is in one US state and the lender in another, the governing-law clause is especially important — courts will usually honor a commercially reasonable choice of law between sophisticated parties.

8

Execute before the loan is advanced

Both parties should sign the note before or at the time funds are transferred. The lender should retain the original signed note; the borrower should receive a copy. For higher-value loans, witness signatures or notarization adds evidentiary weight.

💡 Store the executed original in a secure location — a promissory note may be a negotiable instrument, and the original document is required for enforcement in many jurisdictions.