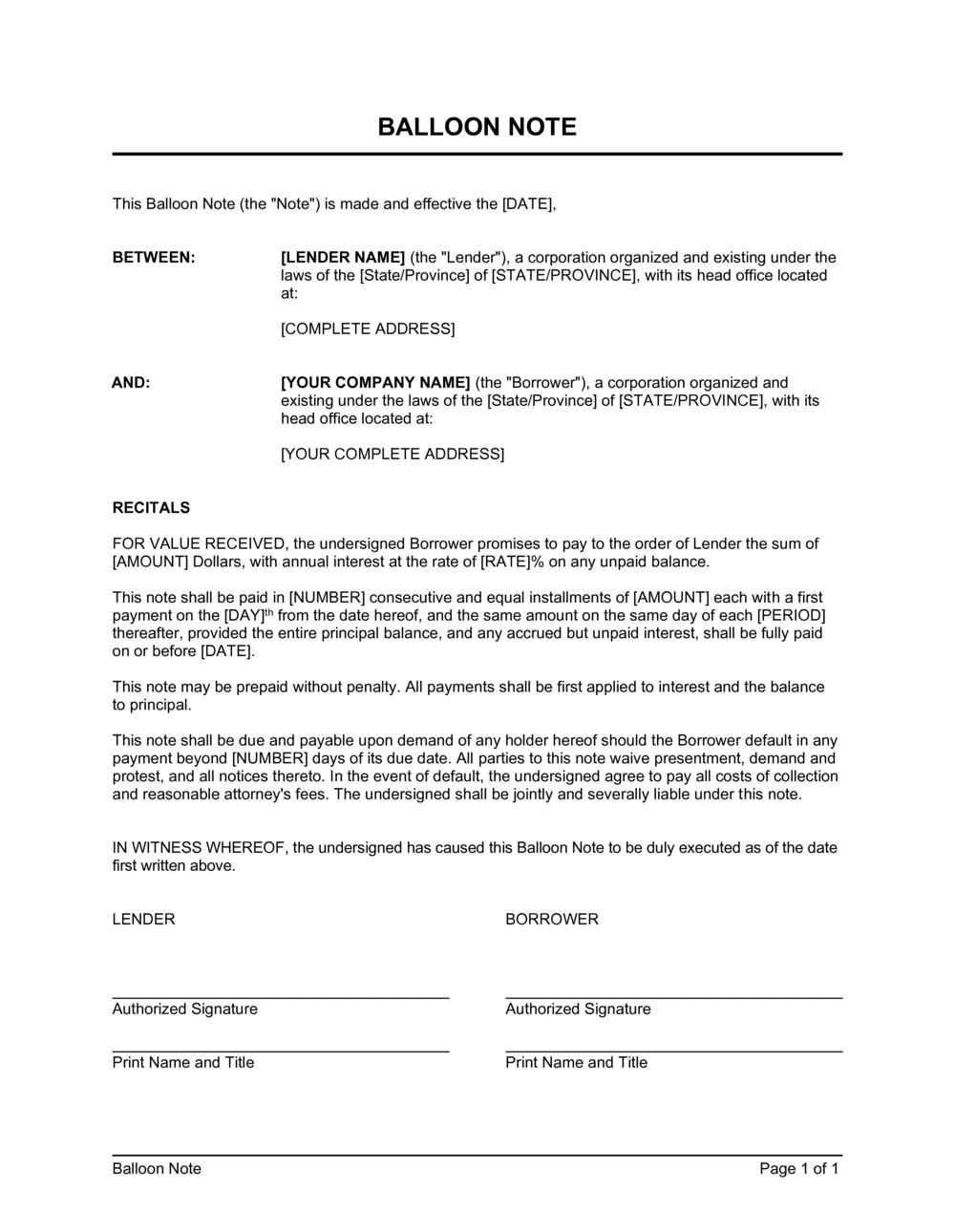

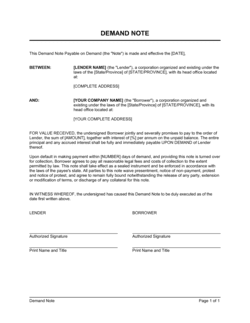

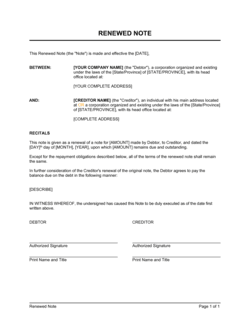

1

Identify the parties with full legal names

Enter the Maker's (borrower's) full legal name — individual or registered entity — and the Holder's (lender's) full legal name. For entities, confirm the name against the corporate registry before execution.

💡 If the borrower is an LLC or corporation, require a copy of the resolution authorizing the borrowing before signing. Unauthorized borrowings can be voided.

2

State the principal amount and execution date

Enter the exact loan amount in both numerals and words (e.g., $250,000 — Two Hundred Fifty Thousand Dollars). Record the date the note is signed, which triggers the interest accrual start.

💡 If funds are disbursed in tranches, consider a construction draw schedule as an exhibit rather than a single principal amount — this keeps the outstanding balance unambiguous at each draw.

3

Set the interest rate and calculation method

Enter the fixed annual percentage rate and specify the day-count convention — actual/365 for most commercial notes, 30/360 for mortgage-style calculations. If the rate is variable, define the index (e.g., SOFR + 2.5%) and any rate cap or floor.

💡 Confirm the stated rate does not exceed your jurisdiction's usury ceiling for this loan type. California, Texas, and New York each impose different usury limits for commercial vs. consumer loans.

4

Define the payment schedule

Set the periodic payment amount, frequency (monthly is most common), first payment date, and the day of the month payments are due. Include a grace period of 5 to 15 days before late fees apply.

💡 If periodic payments are interest-only, state that explicitly — 'each payment shall consist solely of accrued interest, with no reduction of principal.' Ambiguity here leads to disputes about the balloon amount at maturity.

5

Set the maturity date and balloon amount

Enter the specific calendar date on which the balloon payment is due. If the balloon amount can be calculated at execution (e.g., full principal for an interest-only note), state it. If not, define the formula.

💡 Cross-check the maturity date against any related security instrument. A mismatch between the note's maturity and the mortgage's term creates a title defect that title insurers will flag.

6

Draft the default, cure, and acceleration provisions

Define all events that constitute a default, assign a cure period of at least 5 days for payment defaults and 30 days for non-payment defaults, and confirm acceleration is at the Holder's election, not automatic.

💡 List cross-default triggers explicitly — if the borrower has other loans from the same lender, a default on one should trigger a default here. Silence on cross-defaults creates leverage gaps.

7

Reference any security instrument

If the note is secured, cite the security agreement, deed of trust, or mortgage by instrument type and execution date. Confirm the collateral description in the security instrument matches the collateral referenced here.

💡 Record the security instrument in the appropriate public registry (county recorder, UCC filing office) before or simultaneously with executing the note — priority is determined by recording date, not execution date.

8

Execute with proper authority and retain originals

Both parties sign in the signature blocks; entities must sign through an authorized officer or manager. The original signed note — not a photocopy — is the negotiable instrument the Holder needs to enforce.

💡 Store the original note in a fireproof location or with a title company. A lost original promissory note requires a lost-note affidavit proceeding before foreclosure can proceed in most jurisdictions.