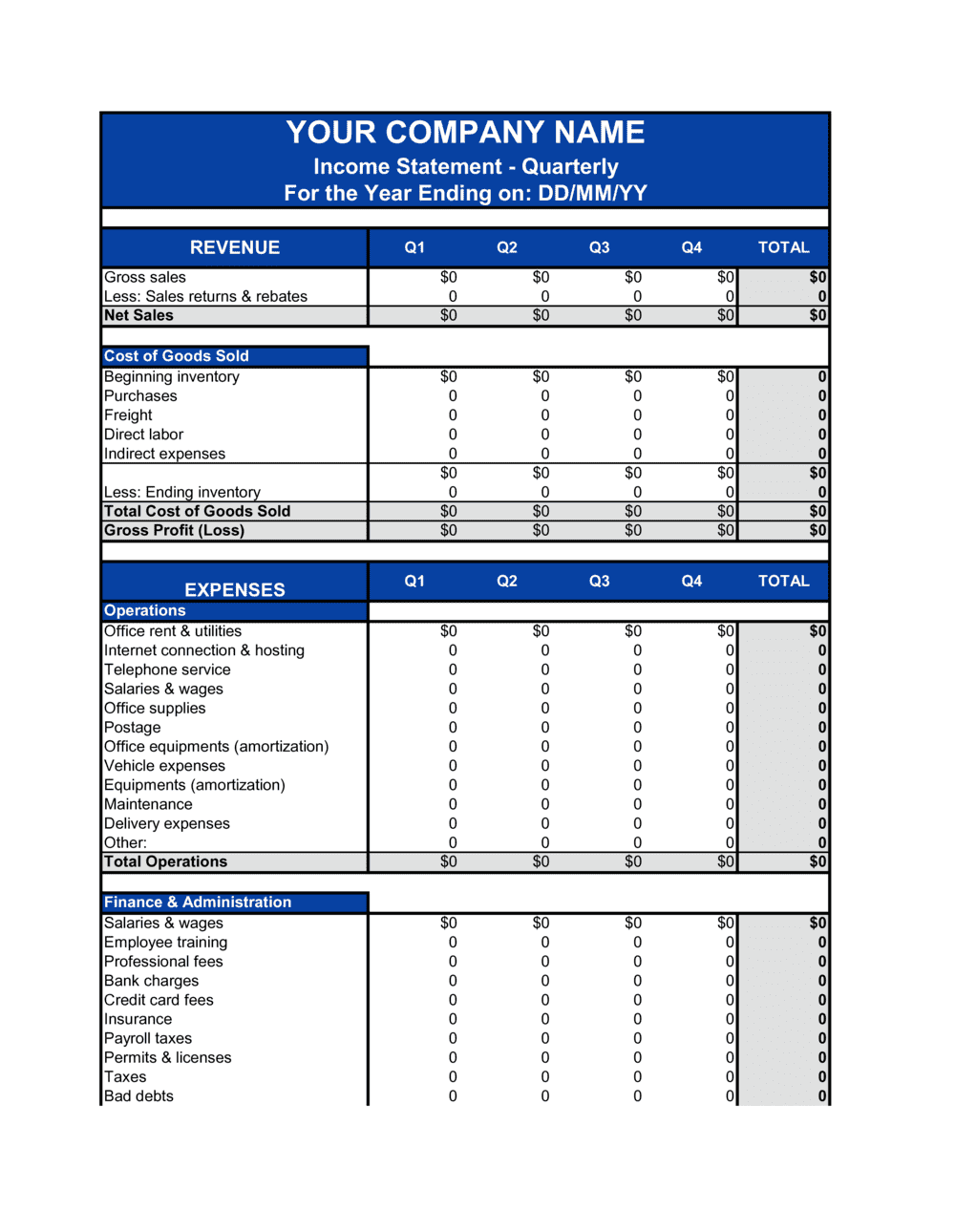

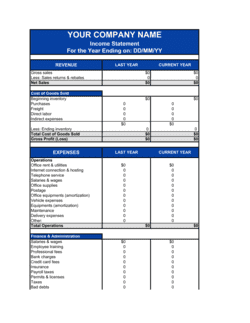

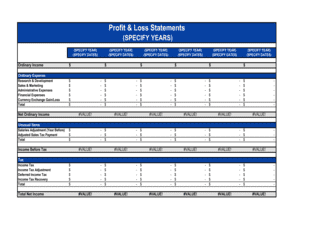

- Revenue

- The total income earned from the sale of goods or services before any costs or expenses are deducted.

- Cost of Goods Sold (COGS)

- The direct costs attributable to producing the goods or services sold during the quarter, including materials and direct labor.

- Gross Profit

- Revenue minus COGS — the profit remaining before operating expenses, interest, and taxes are applied.

- Gross Margin

- Gross profit expressed as a percentage of revenue, used to assess production efficiency and pricing power.

- Operating Expenses (OpEx)

- Recurring costs required to run the business that are not directly tied to production, such as salaries, rent, and marketing.

- Operating Income (EBIT)

- Earnings Before Interest and Taxes — gross profit minus operating expenses, representing the profit generated from core business operations.

- Non-Operating Income and Expenses

- Revenue or costs unrelated to core operations, such as interest income, investment gains, or foreign exchange losses.

- Pre-Tax Income (EBT)

- Earnings Before Tax — operating income adjusted for non-operating items, representing profit before the tax provision is applied.

- Tax Provision

- The estimated income tax expense recognized in the period, calculated as a percentage of pre-tax income based on the applicable statutory rate.

- Net Income

- The bottom-line profit or loss after all revenues, costs, expenses, and taxes have been accounted for during the quarter.

- Prior-Period Comparison

- A column showing the same line items from the equivalent prior quarter or the immediately preceding quarter, enabling trend analysis.

- Accrual Basis Accounting

- A method that records revenues when earned and expenses when incurred, regardless of when cash is received or paid.