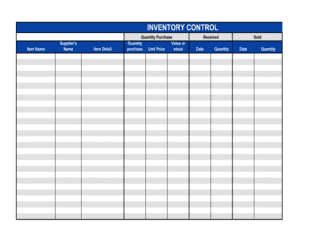

- Book Inventory

- The quantity of a SKU recorded in an accounting or inventory management system, based on transactions rather than a physical count.

- Physical Count

- The actual quantity of a specific item found on the shelf, bin, or floor during a manual or scanner-assisted count.

- Variance

- The numerical difference between book inventory and physical count for a given SKU — positive when physical exceeds book, negative when book exceeds physical.

- Cycle Count

- A scheduled, ongoing process of counting a rotating subset of SKUs rather than shutting down operations for a full stocktake.

- Shrinkage

- Inventory loss attributable to theft, damage, administrative error, or vendor fraud — expressed as a percentage of cost of goods sold.

- SKU (Stock-Keeping Unit)

- A unique alphanumeric identifier assigned to a specific product variant for tracking purposes in purchasing, sales, and inventory systems.

- Adjustment Entry

- A corrective journal entry or system transaction that updates book inventory to match the verified physical count after reconciliation.

- Root Cause Analysis

- The structured process of tracing a discrepancy back to its origin — receiving error, picking error, theft, system lag, or data entry mistake.

- FIFO / LIFO

- First-In-First-Out and Last-In-First-Out — inventory costing methods that affect the dollar value assigned to stock on hand and cost of goods sold.

- Dead Stock

- Inventory that has not moved within a defined period and is unlikely to sell, often requiring write-down or write-off in the reconciliation process.

- Bin Location

- A specific, labeled storage position in a warehouse or stockroom used to track exactly where each SKU is physically stored.