1

Gather the underlying financial statements

Collect the balance sheet and income statement for the period you are analyzing. Confirm whether they are audited, reviewed, or internally prepared, and note the accounting standard (GAAP, IFRS, or ASPE).

💡 Use the same-period statements throughout — mixing a Year-End balance sheet with a mid-year income statement produces ratios that are not comparable to any standard benchmark.

2

Enter the reporting period and financial statement basis

Fill in the fiscal period end date and tick the appropriate disclosure for statement quality (audited, reviewed, or internal). This information appears on every page of the output.

💡 If submitting to a lender, confirm their covenant reporting requirements before you start — some require audited statements for annual submissions and reviewed statements for quarterly ones.

3

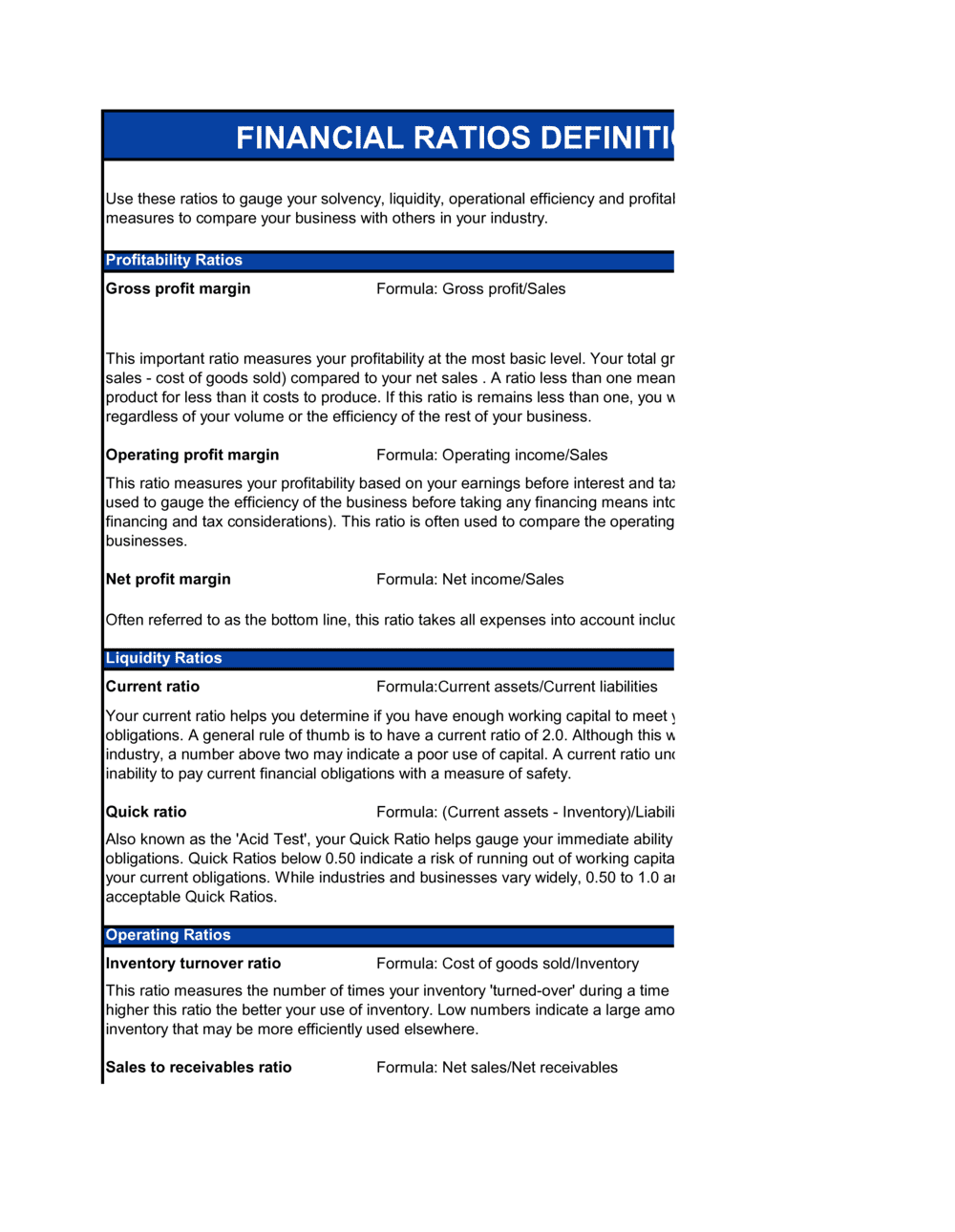

Populate the liquidity ratios inputs

Enter current assets, inventory, and current liabilities from the balance sheet. The template calculates current ratio and quick ratio automatically.

💡 Exclude prepaid expenses and deferred tax assets from the quick ratio numerator — these items cannot be quickly converted to cash.

4

Complete the profitability ratios inputs

Enter revenue, COGS, gross profit, EBIT, net income, total assets, and shareholders' equity. The template derives gross margin, net margin, ROA, and ROE.

💡 Use post-tax net income for ROA and ROE. Cross-check that the net income figure matches the bottom line of your income statement to the cent.

5

Fill in the leverage and solvency inputs

Enter total liabilities, total debt (including current portion of long-term debt), shareholders' equity, EBIT, and interest expense to compute debt-to-equity, debt-to-assets, and interest coverage.

💡 Check whether your loan agreement uses a narrow definition of 'total debt' (funded debt only) or a broad one (all liabilities). Use the definition in the covenant, not the balance sheet total.

6

Enter efficiency ratio inputs

Input COGS, average inventory (opening plus closing divided by two), accounts receivable, accounts payable, and the number of days in the period. The template calculates inventory turnover, DSO, and AP days.

💡 For DSO, divide accounts receivable by average daily revenue — not total revenue. Dividing by total revenue without adjusting for the period length produces a ratio that is not comparable across periods of different length.

7

Review the benchmark comparison table

Check calculated ratios against the industry benchmark column. Flag any ratio outside the acceptable range in the Status column and add a brief explanation in the variance notes section.

💡 Source industry benchmarks from a specific sector database (e.g., RMA Annual Statement Studies, IBISWorld, or your industry association) rather than generic business averages.

8

Complete the certification block and obtain the required signature

Have the appropriate officer — CFO, CEO, or controller, depending on the loan agreement — sign and date the attestation. Retain a copy with the original financial statements.

💡 Never pre-sign the certification before entering figures. The attestation certifies the specific numbers on the page — signing a blank or partially completed form exposes the signatory to personal liability.