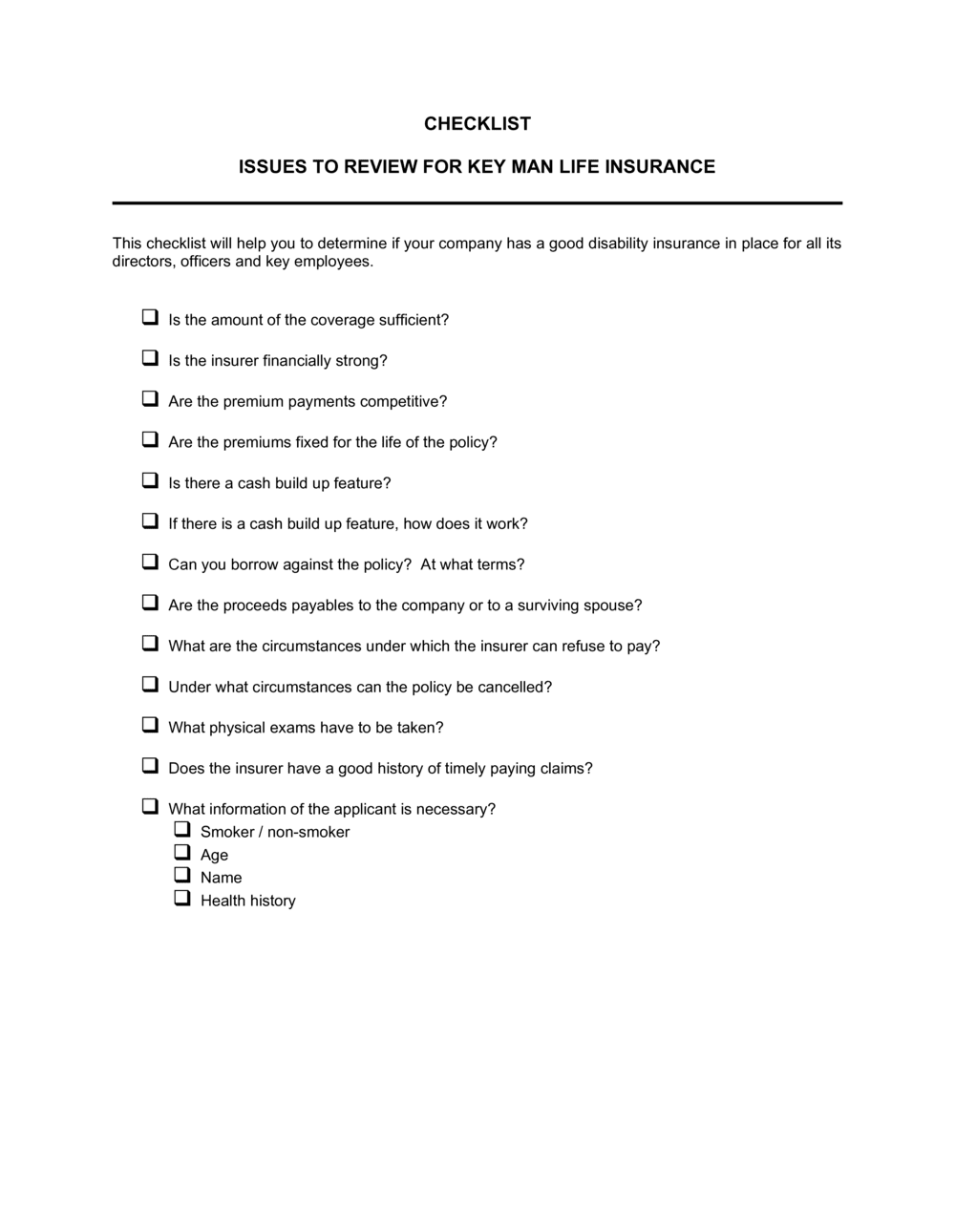

1

Identify which employees qualify as key persons

List every employee or owner whose sudden loss would cause measurable financial harm — lost revenue, client attrition, or an inability to deliver core services. Typical candidates include founders, top salespeople, lead engineers, and employees with unique client relationships.

💡 A practical threshold: if replacing this person would take more than 3 months and cost more than 1× their annual salary, they likely qualify.

2

Complete the role criticality assessment for each person

Document the specific dollar impact — annual revenue they generate or influence, cost to recruit and train a replacement, or outstanding loan or contract obligations tied to their performance.

💡 Pull numbers from your CRM or financial reports to make the assessment concrete and defensible for insurers or investors.

3

Calculate the appropriate coverage amount

Choose a calculation method — salary multiple (5–10×), revenue contribution (1–2 years' worth), or replacement cost — and record both the method and the resulting figure in the coverage field.

💡 If the business has an SBA loan, confirm the required coverage amount directly with the lender; SBA guidelines often specify a minimum death benefit equal to the outstanding loan balance.

4

Select the policy type and obtain quotes

Decide between term (lower cost, finite period) and permanent (builds cash value, lifelong coverage) based on the business objective. Get at least two carrier quotes before completing the policy details field.

💡 Term policies work well when coverage is tied to a specific loan or time-limited risk; permanent policies double as a tax-advantaged executive retention tool.

5

Fill in insurer and policy details after placement

Once the policy is issued, record the carrier name, policy number, issue date, and premium schedule in the checklist. File a copy of the policy alongside the completed checklist.

💡 Store the checklist and policy documents in a shared secure folder accessible to at least two people — sole custody creates its own key-person risk.

6

Confirm consent and disclosure compliance

Obtain and file the employee's written consent to the policy before the policy is issued. Record the date consent was given and confirm it matches the insurer's records.

💡 Use a separate consent form with the employee's signature; a checkbox on the checklist alone is not a substitute for a standalone signed document.

7

Schedule the next review date

Set a calendar reminder for the annual review — at minimum, verify that coverage amounts still reflect the employee's current role, salary, and business contribution.

💡 Tie reviews to your fiscal year-end so coverage assessment happens alongside your financial planning cycle.