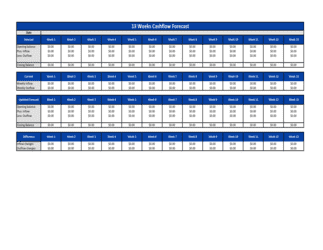

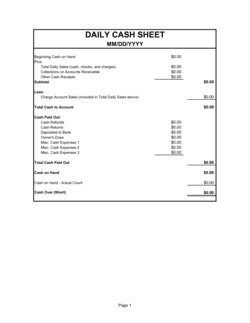

- Opening Cash Balance

- The amount of cash held at the start of a forecast period, carried forward from the prior month's closing balance.

- Cash Inflow

- Any source of cash received during the period — including customer receipts, loan drawdowns, asset sales, or investor contributions.

- Cash Outflow

- Any payment of cash made during the period — including supplier payments, payroll, rent, loan repayments, and tax remittances.

- Net Cash Movement

- Total cash inflows minus total cash outflows for the month — a positive figure means cash increased; negative means it decreased.

- Closing Cash Balance

- The amount of cash remaining at the end of the period, calculated as opening balance plus net cash movement.

- Burn Rate

- Monthly net cash outflow for a pre-revenue or growth-stage business — how quickly it consumes available capital.

- Runway

- The number of months a business can operate at its current burn rate before cash reaches zero, assuming no new revenue or funding.

- Operating Activities

- Cash flows directly tied to the core business — customer receipts, supplier payments, wages, and overhead expenses.

- Investing Activities

- Cash flows from the purchase or sale of long-term assets such as equipment, vehicles, or property.

- Financing Activities

- Cash flows related to borrowing or repaying debt, issuing equity, or paying dividends to shareholders.

- Variance

- The difference between a forecasted cash figure and the actual amount recorded — used to measure forecast accuracy and flag emerging issues.

- Accrual vs. Cash Basis

- Accrual accounting records revenue and expenses when earned or incurred; cash-basis accounting records them only when cash actually changes hands — a cashflow forecast always uses the cash basis.