1

Define the scope and list affected roles

Identify every job title that touches cash — cashiers, shift supervisors, managers, bookkeepers — and name them explicitly in the scope section. Exclude roles with no cash responsibility.

💡 Use job titles, not employee names. The policy outlasts any individual employee.

2

Set the opening float amount and denomination breakdown

Decide on a standard float for each register type and list the exact denomination mix (e.g., 4 × $5, 10 × $1, 2 rolls of quarters). Document this in the opening float section.

💡 Match the denomination mix to your typical transaction profile — a coffee shop needs more $1 bills than a furniture store.

3

Establish safe drop and drawer thresholds

Set the dollar amount at which a mid-shift safe drop is required. A common threshold for retail is $200–$300 above the float. Document the witness requirement and log format.

💡 Lower thresholds reduce theft exposure but increase operational interruption. Balance both factors against your average transaction volume.

4

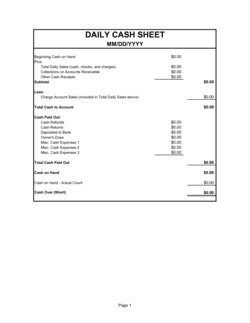

Document the end-of-shift reconciliation steps

Write out the exact sequence: cashier counts drawer, supervisor witnesses, both compare to POS report, over/short is recorded, form is signed. Attach the Daily Cash Reconciliation Form as an appendix.

💡 A form with pre-printed denomination rows speeds up counting and reduces transcription errors during busy close periods.

5

Define deposit frequency and transportation method

State how often deposits must be made (daily is best practice), who prepares and verifies them, and whether a courier service, night drop, or in-person bank visit is used.

💡 If using a night-drop safe, document the bank's confirmation process so you have a receipt trail independent of the cash count.

6

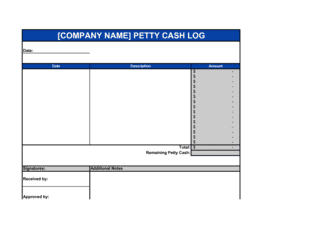

Set petty cash parameters

Enter the fund balance, per-transaction limit, eligible expense categories, and replenishment trigger (e.g., when the fund drops below $50). Name the custodian by title.

💡 Keep the petty cash fund physically separate from register cash to prevent commingling during counts.

7

Set discrepancy thresholds and assign investigation ownership

Define at least two escalation tiers — a minor threshold for same-day manager notification and a higher threshold triggering formal investigation. Name the investigating role by title.

💡 Consistent, documented investigation of even small discrepancies deters theft more effectively than reacting only to large losses.

8

Add the acknowledgment block and distribute for signatures

Include a signature line at the end of the policy confirming the employee has read, understood, and agrees to follow the procedures. Collect signed copies before an employee's first cash-handling shift.

💡 Store signed acknowledgments in each employee's HR file alongside their onboarding paperwork, not in a shared cash-office binder.