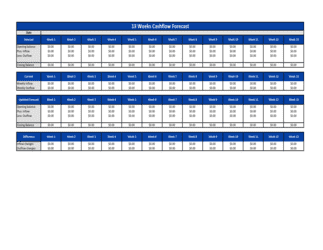

- Opening Balance

- The actual cash and cash-equivalent balance at the start of each forecast period, carried forward from the prior period's closing balance.

- Cash Inflow

- Any receipt of cash into the business — from customers, loans, asset sales, or investor contributions — during a forecast period.

- Cash Outflow

- Any payment of cash out of the business — to suppliers, employees, lenders, or tax authorities — during a forecast period.

- Net Cash Movement

- Total cash inflows minus total cash outflows for a given period; a positive figure increases the balance, a negative figure depletes it.

- Closing Balance

- The projected cash balance at the end of a period, calculated as opening balance plus net cash movement; becomes the next period's opening balance.

- Burn Rate

- Monthly net cash outflow for a business spending more than it earns — how fast it consumes its available cash reserves.

- Runway

- The number of months a business can continue operating at its current burn rate before exhausting available cash.

- Variance

- The difference between a forecasted figure and the actual figure recorded once the period has passed, used to improve future forecast accuracy.

- Rolling Forecast

- A forecast that is updated each period to always look a fixed number of weeks or months ahead, rather than ending at a fixed year-end date.

- Accrual vs. Cash Basis

- Accrual accounting records revenue and expenses when earned or incurred; cash-basis accounting — used in cash flow forecasts — records only when cash actually moves.

- Trade Receivables

- Amounts owed to the business by customers for goods or services already delivered but not yet paid for.

- Working Capital

- Current assets minus current liabilities — the short-term liquidity buffer a business uses to fund day-to-day operations.