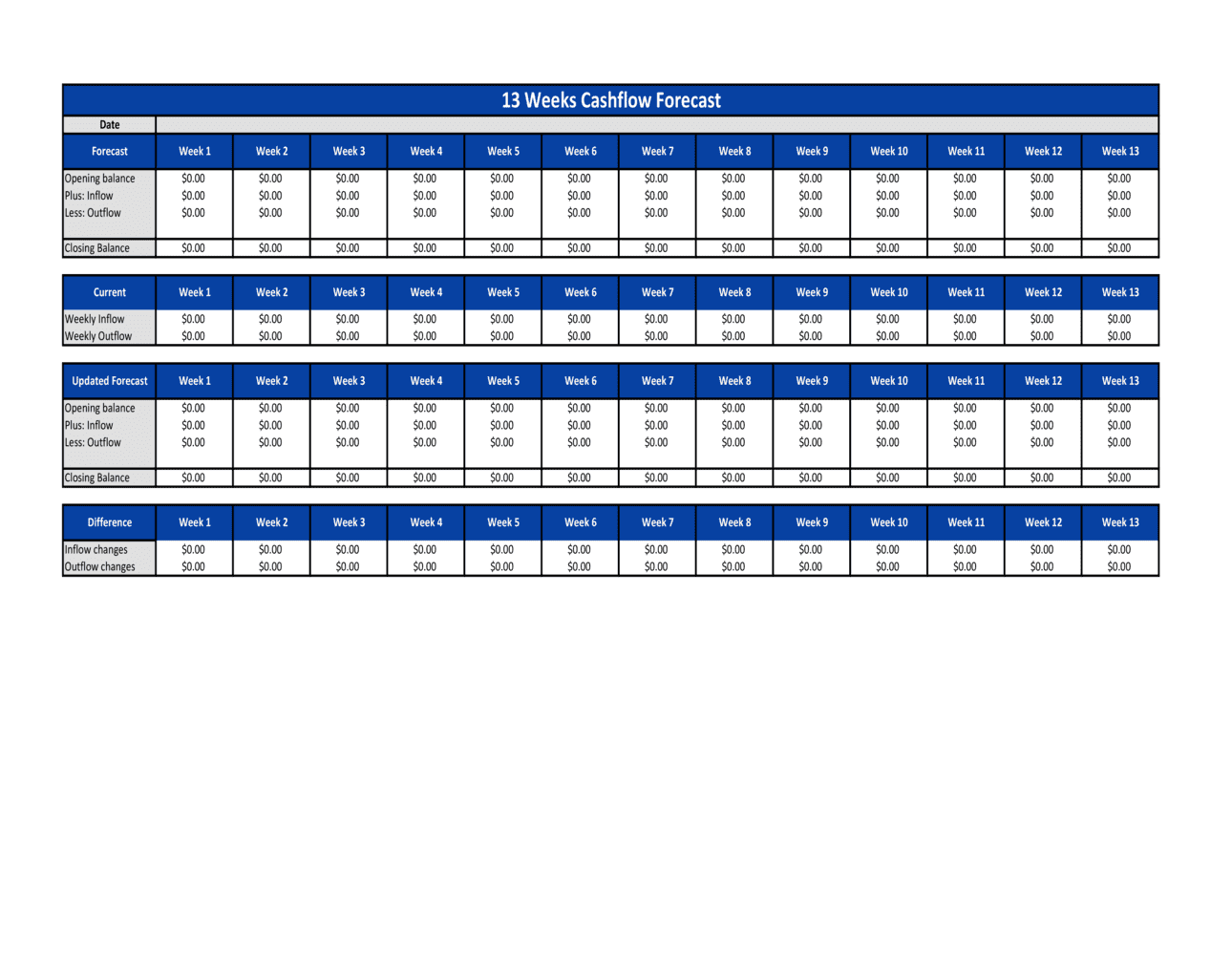

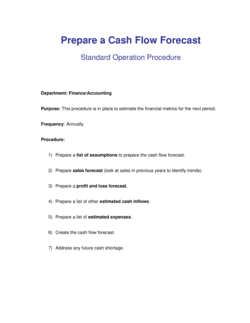

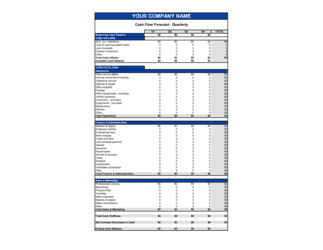

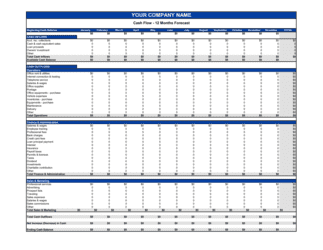

- Opening Cash Balance

- The verified cash in bank accounts at the start of the forecast period, taken directly from the most recent bank statement.

- Closing Cash Balance

- The projected cash remaining at the end of each forecast week, calculated as the opening balance plus net cash movement for that week.

- Cash Inflows

- All cash expected to be received in a given week — customer payments, loan proceeds, asset sales, or tax refunds — not revenue recognised on an accrual basis.

- Cash Outflows (Disbursements)

- All cash payments expected to leave the business in a given week, including payroll, rent, supplier payments, debt service, and tax remittances.

- Net Cash Movement

- Total inflows minus total outflows for a single week — a positive number increases the closing balance; a negative number draws it down.

- Variance

- The difference between the forecasted cash position and the actual cash position for a completed week, used to assess forecast accuracy and identify surprises.

- Runway

- The number of weeks remaining before the closing cash balance reaches zero at the current projected net cash movement, assuming no new financing.

- Burn Rate

- Average weekly net cash outflow, calculated over the forecast period, showing how quickly the business is consuming its cash reserves.

- Rolling Forecast

- A forecast updated each week by dropping the completed week and adding a new week at the end, always maintaining a 13-week forward view.

- Covenant Compliance

- A contractual obligation to a lender that requires the borrower to maintain minimum cash balances or meet other financial thresholds — a 13-week forecast is often the reporting tool used to demonstrate compliance.