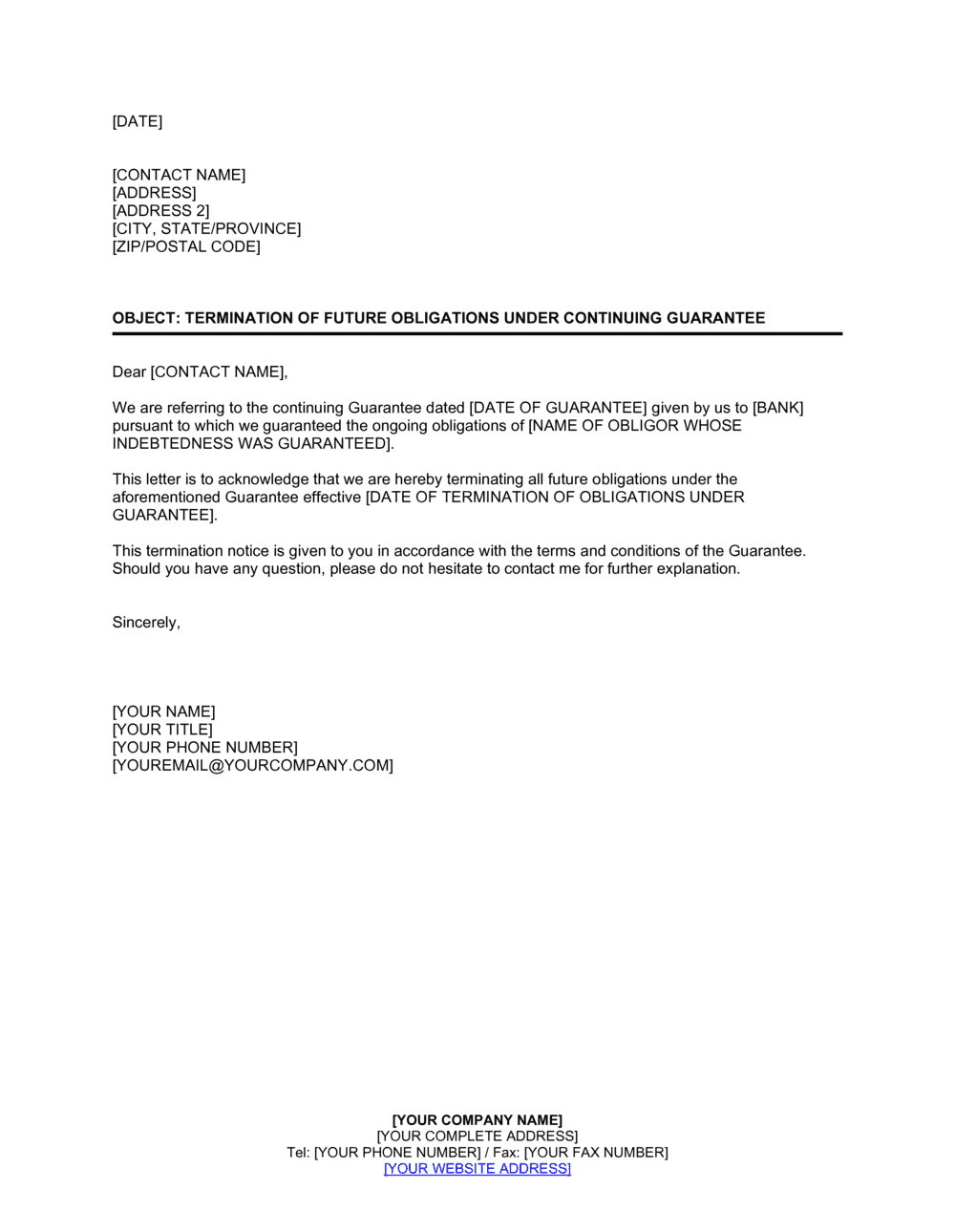

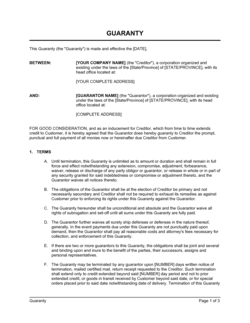

- Continuing Guaranty

- A guaranty that covers an ongoing and potentially unlimited series of future transactions or obligations, rather than a single fixed debt.

- Future Guaranty

- The portion of a continuing guaranty that applies to obligations not yet incurred at the time a revocation notice is delivered.

- Guarantor

- The individual or entity that promises to satisfy a debt or obligation if the primary debtor fails to do so.

- Principal Debtor

- The party whose debt or obligation is guaranteed — the borrower, tenant, or buyer whose performance the guarantor is backing.

- Revocation

- The act of formally withdrawing a continuing guaranty with respect to obligations not yet created, effective from the date the creditor receives written notice.

- Prospective Liability

- Exposure arising from transactions or obligations entered into after the termination notice date — the category of liability this document eliminates.

- Accrued Liability

- Obligations already created under the guaranty before the revocation notice is received, which typically remain enforceable against the guarantor regardless of termination.

- Creditor

- The lender, supplier, landlord, or other party who extended credit or extended an obligation in reliance on the guaranty.

- Consideration

- Something of value exchanged to make a contract enforceable — in the context of a guaranty termination, this is often the guarantor's written notice and the creditor's acknowledgment.

- Delivery

- The act of formally transmitting the termination notice to the creditor in a manner that establishes a documented date of receipt, such as certified mail or personal delivery.

- Survival Clause

- A contractual provision confirming that certain obligations — here, pre-termination guaranty liability — remain in force even after the document takes effect.