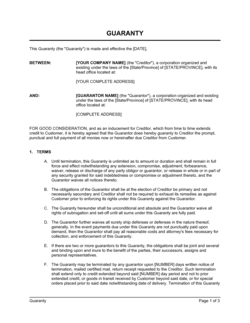

- Guarantor

- The person or entity that promises to satisfy a debt or obligation if the primary obligor defaults.

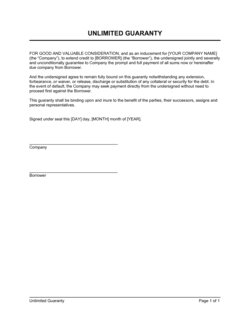

- Continuing Guaranty

- A guaranty that covers an open-ended series of future transactions or obligations, rather than a single fixed amount, and remains in force until formally revoked.

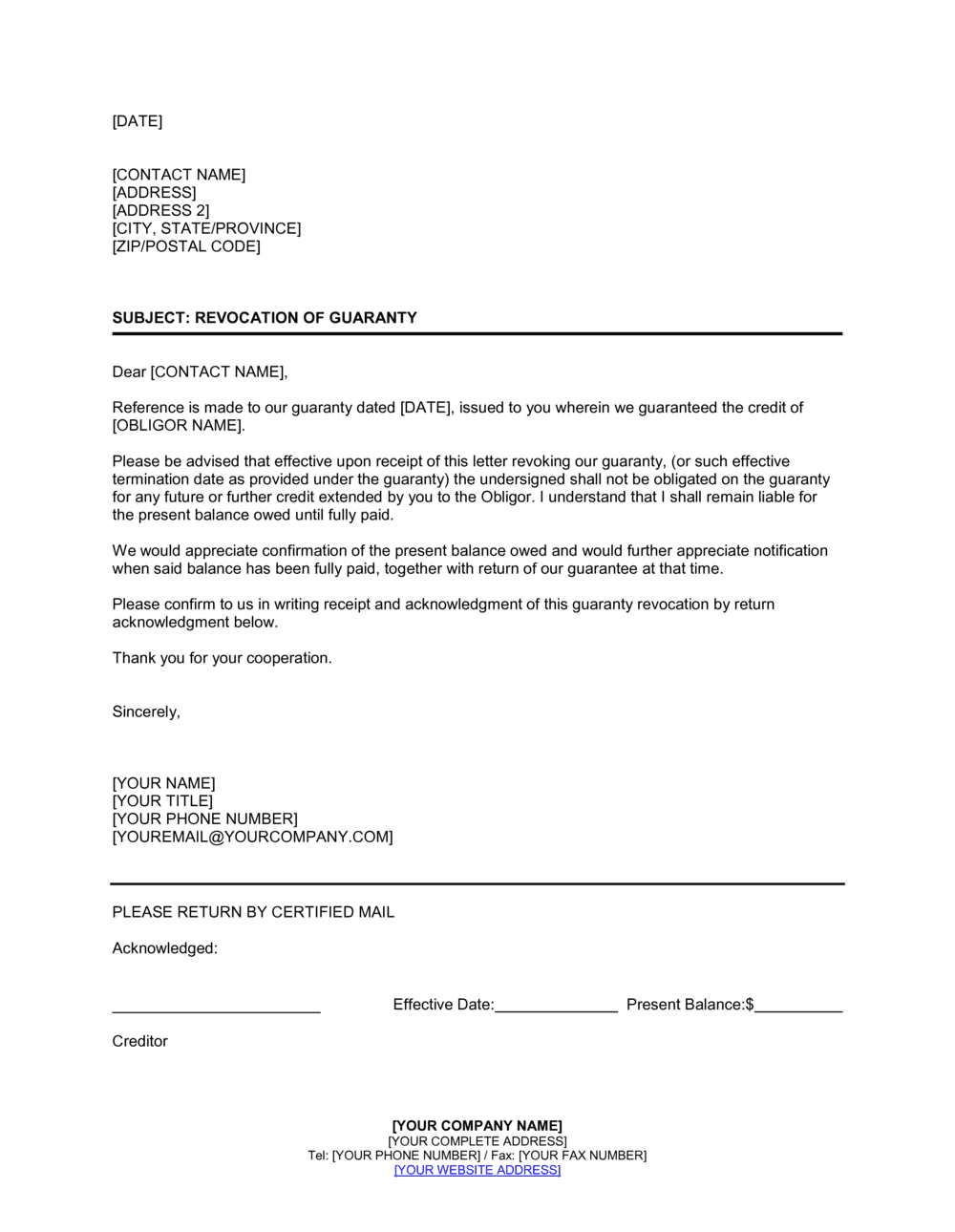

- Revocation

- A formal, written withdrawal of a guarantor's commitment to be liable for future obligations arising after the notice is delivered.

- Primary Obligor

- The borrower, tenant, or debtor whose obligation the guarantor has agreed to back — distinct from the guarantor themselves.

- Creditor or Obligee

- The lender, landlord, or supplier to whom the guaranty was given and to whom the revocation notice must be delivered.

- Effective Date

- The specific date on which the revocation takes effect and after which the guarantor incurs no new liability under the guaranty.

- Accrued Obligations

- Debts or liabilities already incurred under the original guaranty before the revocation's effective date, for which the guarantor remains responsible.

- Notice Clause

- The provision in the original guaranty or the revocation document specifying how, and to whom, a revocation notice must be delivered to be legally effective.

- Suretyship

- The legal relationship in which one party (the surety or guarantor) agrees to answer for the debt or default of another — the broader legal category that includes guaranty contracts.

- Consideration

- Something of value exchanged between parties to make a contract binding — in a revocation context, courts in some jurisdictions examine whether adequate consideration supports the release from future liability.

- Notarization

- Authentication of a document's execution by a licensed notary public, required by some lenders or jurisdictions to make a guaranty revocation effective against third parties.