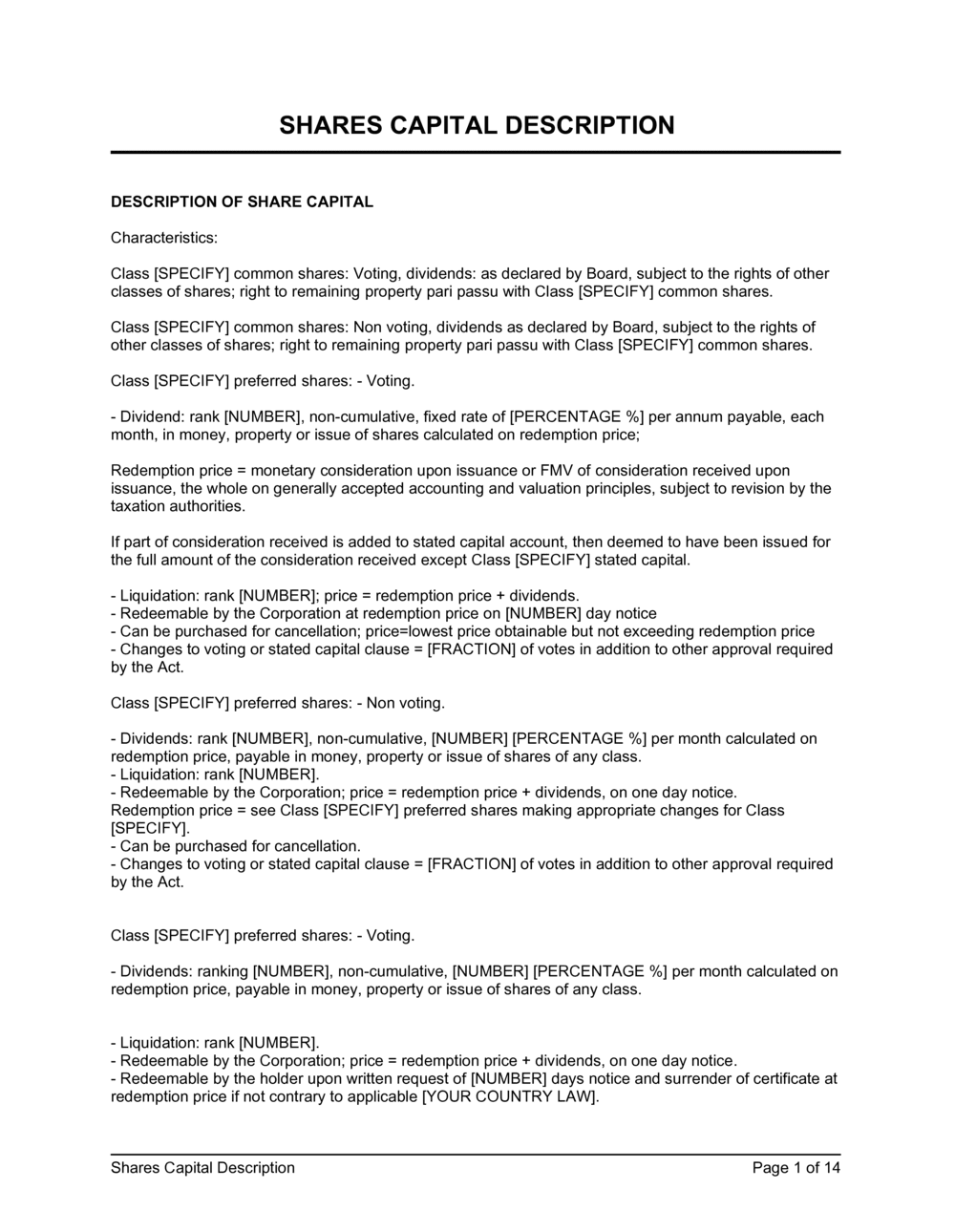

What is a Shares Capital Description — Preferred Shares?

A Shares Capital Description — Preferred Shares is a formal binding corporate document that defines all the rights, privileges, restrictions, and conditions attached to a class of preferred shares in a corporation's authorized capital structure. It specifies how preferred shareholders are treated in relation to common shareholders across four critical dimensions: economic rights (dividends, liquidation preference, and participation), conversion mechanics (voluntary and mandatory conversion into common shares, anti-dilution adjustments), governance rights (voting, protective provisions, and board representation triggers), and exit mechanics (redemption rights and deemed liquidation definitions). In most jurisdictions, this document is embedded in or attached to the corporation's articles of incorporation, making it a public corporate record rather than a private agreement.

Preferred shares are the standard equity instrument used in venture capital and angel financing because they allow investors to negotiate specific protections — a priority return of capital, anti-dilution adjustments in down rounds, and veto rights over major corporate decisions — while still holding equity that converts into common shares at a successful exit. The shares capital description is the document that makes those protections legally binding and enforceable against the corporation and all current and future shareholders.

Why You Need This Document

Without a clearly drafted preferred shares capital description, the specific economic and governance protections that investors negotiate in a term sheet have no legal standing once shares are issued. A handshake understanding of "1× liquidation preference and weighted-average anti-dilution" means nothing if those terms are not formally incorporated into the articles. When a sale or merger occurs, the distribution of proceeds is determined by what the articles say — not what the parties understood at the time of investment. Ambiguous or missing terms in the capital description become the basis for shareholder disputes, delayed closings, and, in the worst cases, litigation that consumes the very proceeds being distributed.

For founders, a well-structured preferred share description protects the common share value that founders and employees hold. For investors, it is the legal foundation of their economic rights. For both parties, having a professionally structured template as a starting point — reviewed by counsel before filing — reduces the negotiation surface, speeds up incorporation and amendment filings, and ensures the document integrates cleanly with the shareholder agreement and share purchase agreement that accompany every serious financing round.