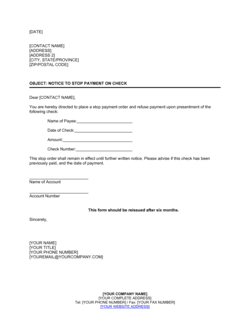

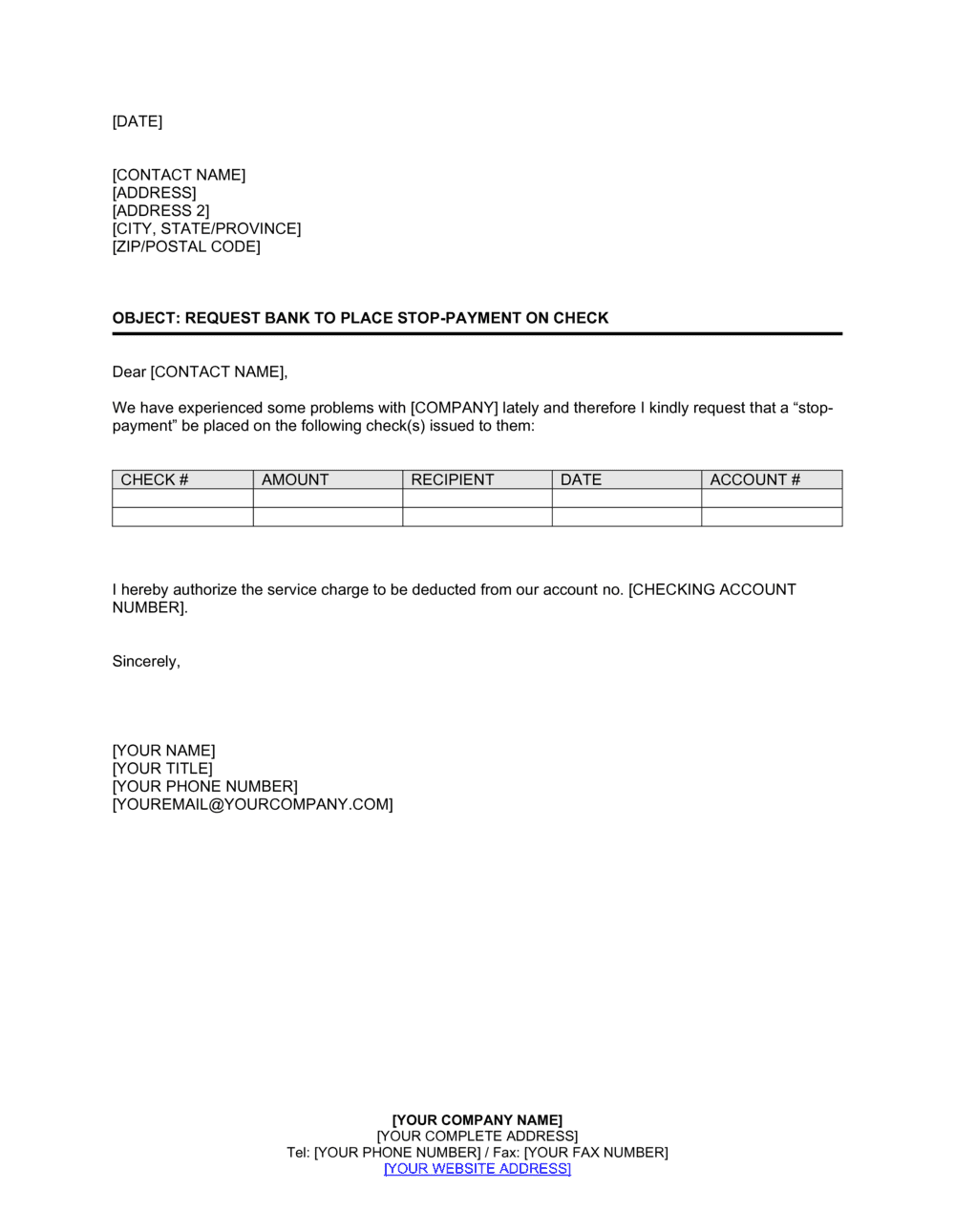

❌ Providing an approximate payment amount

Why it matters: Banks match stop payment orders against the exact dollar amount of the check. An amount off by even one cent means the system fails to identify the instrument and the check clears.

Fix: Locate the check stub or the check image in your online banking portal and enter the precise amount, including cents, before submitting the letter.