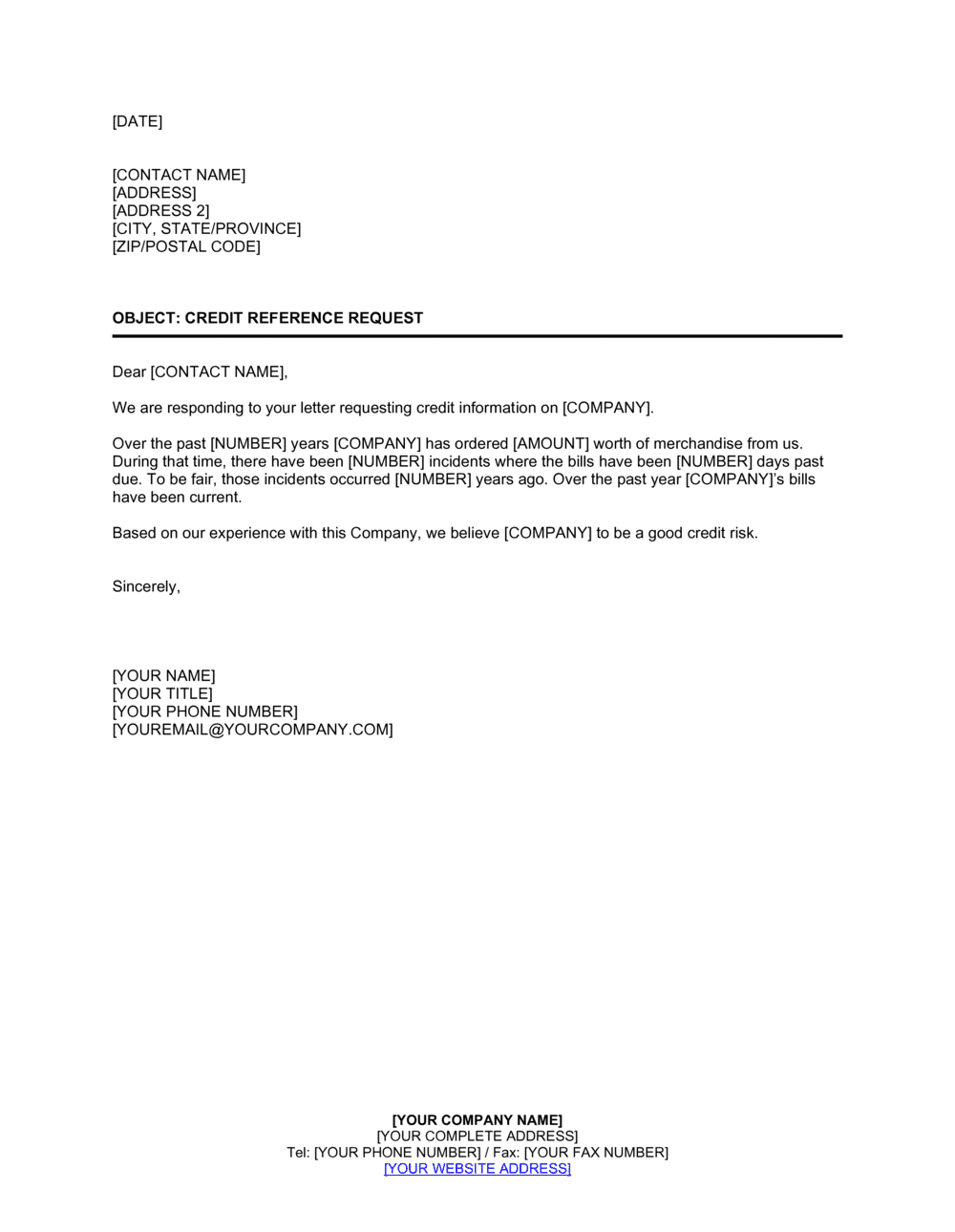

What is a Credit Reference Response?

A Credit Reference Response is a formal written statement issued by a creditor — typically a supplier, vendor, or financial institution — in reply to a third-party request for information about a shared customer's credit history and account standing. It documents the credit limit extended, the payment terms agreed, the customer's actual payment behavior over a defined period, and the current status of the account. Crucially, a properly drafted credit reference response also includes a confidentiality notice restricting the use of the information and a limitation-of-liability disclaimer protecting the responding party from legal claims arising from reliance on the reference.

Unlike a general business recommendation letter, a credit reference response is a narrowly scoped financial disclosure used by the requesting party to make a specific lending or trade credit decision. Because it influences commercial decisions with measurable financial consequences, it carries a higher standard of accuracy and greater legal scrutiny than most routine business correspondence.

Why You Need This Document

Responding to a credit inquiry without a structured, legally protective template exposes your business on multiple fronts simultaneously. A casually worded email confirming that a customer "always pays on time" — without a disclaimer — can form the basis of a negligent misstatement claim if that customer later defaults and the requesting party suffers a loss. Courts in the US, UK, and Canada have found creditors liable in exactly these circumstances when no limitation-of-liability clause was present.

Equally, sharing account data without a confidentiality notice leaves you with no contractual basis to object if the requesting party forwards your reference to the customer being evaluated — damaging a commercial relationship you depend on. And a response signed by someone without authority to bind the company may be legally ineffective precisely when you need it to stand up to scrutiny.

This template gives you a complete, liability-conscious framework: specific placeholders for the factual data that makes a reference useful, a confidentiality clause that restricts onward disclosure, a disclaimer that removes warranty liability, and a signature block that confirms authorized execution. What takes a legally unprotected email minutes to get wrong takes this template under thirty minutes to get right.