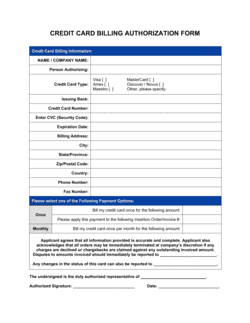

1

Identify the account holder and authorized users

Enter the customer's full legal name or registered entity name, their billing address, and the names and titles of every person authorized to charge against the account. Cross-reference the credit application for accuracy.

💡 For business accounts, verify the entity name against the state or provincial corporate registry before signing — mismatches create collection headaches later.

2

Set the approved credit limit

Enter the credit limit you approved based on the customer's application, trade references, and your internal credit policy. Document the basis for the limit in your internal credit file, not in the agreement itself.

💡 Include a sentence reserving your right to reduce the limit on 30 days' notice — this gives you flexibility if the customer's payment behavior deteriorates.

3

Define the billing cycle and payment due date

Choose a billing period (typically calendar month), state the statement issue date, and set a specific payment due date — not 'upon receipt.' Specify whether net-30 or net-60 terms apply.

💡 Aligning all customer billing cycles to the same calendar date (e.g., the last day of the month) simplifies your accounts-receivable workflow significantly.

4

Disclose the APR and late-fee schedule

Enter the annual percentage rate that will apply to unpaid balances, compute and list the daily periodic rate, and state the flat late fee per overdue statement. Confirm these rates comply with your jurisdiction's usury limits.

💡 In the US, check both federal Regulation Z disclosure requirements and the applicable state usury cap — some states set ceilings as low as 18% APR for commercial accounts.

5

Add the personal guarantee (for business accounts)

For any business customer, include the guarantee clause with the guarantor's full legal name and have them sign it in their individual capacity, separately from the entity signature block.

💡 Require the guarantor to initial the guarantee clause specifically, in addition to signing the full agreement — this reduces the risk of a later claim that they did not read or agree to the personal liability.

6

Specify the default events and remedies

List every event you intend to trigger default — non-payment past X days, exceeding the credit limit, and insolvency — and confirm that the acceleration clause makes the full balance immediately due upon any trigger.

💡 Build in a cure period for first-time non-payment (e.g., 10 days after written notice) to avoid triggering default over a single missed due date from an otherwise reliable customer.

7

Execute before the first charge is made

Obtain the customer's signature — and the guarantor's separate signature — before the account is opened and any purchases are charged. File the signed original in your accounts-receivable records.

💡 Send the executed agreement to the customer via email with a PDF copy immediately after signing — this eliminates later claims that they never received the final terms.

8

File a UCC-1 if taking a security interest

If you included the security interest clause, file a UCC-1 financing statement with the appropriate state office within a few days of execution to perfect your interest in the purchased goods.

💡 Set a calendar reminder to renew the UCC-1 before it lapses at five years — a lapsed financing statement leaves your security interest unperfected as of the lapse date.