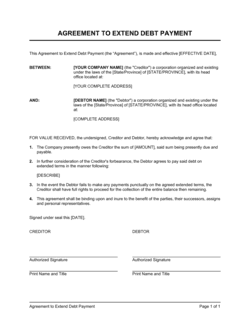

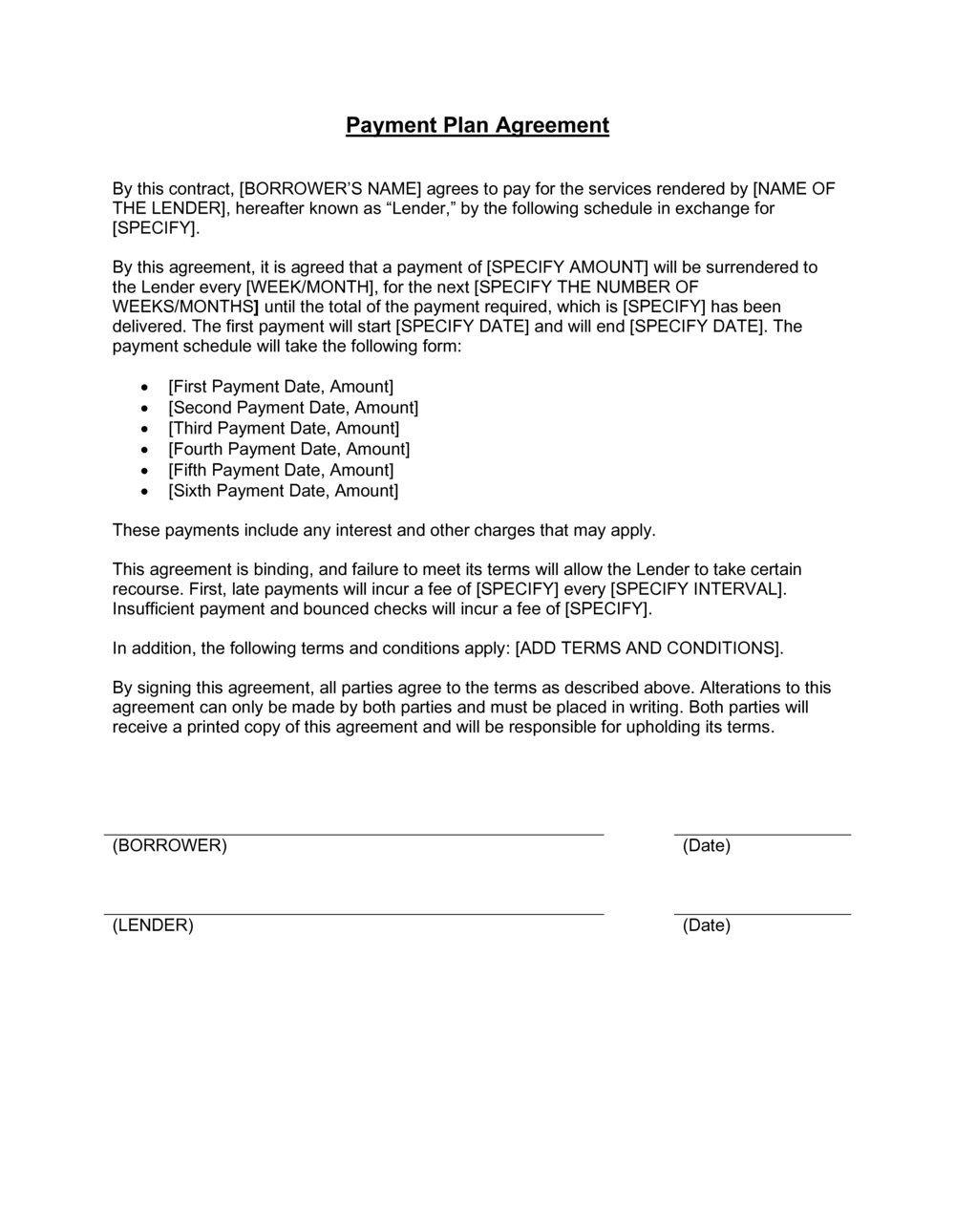

❌ No written acknowledgment of the debt

Why it matters: Without it, the debtor can dispute the amount or claim the debt does not exist, forcing the creditor to produce invoices, contracts, and communications to re-establish the balance in court.

Fix: Include a dedicated acknowledgment clause where the debtor confirms the exact balance and its source in the body of the agreement.