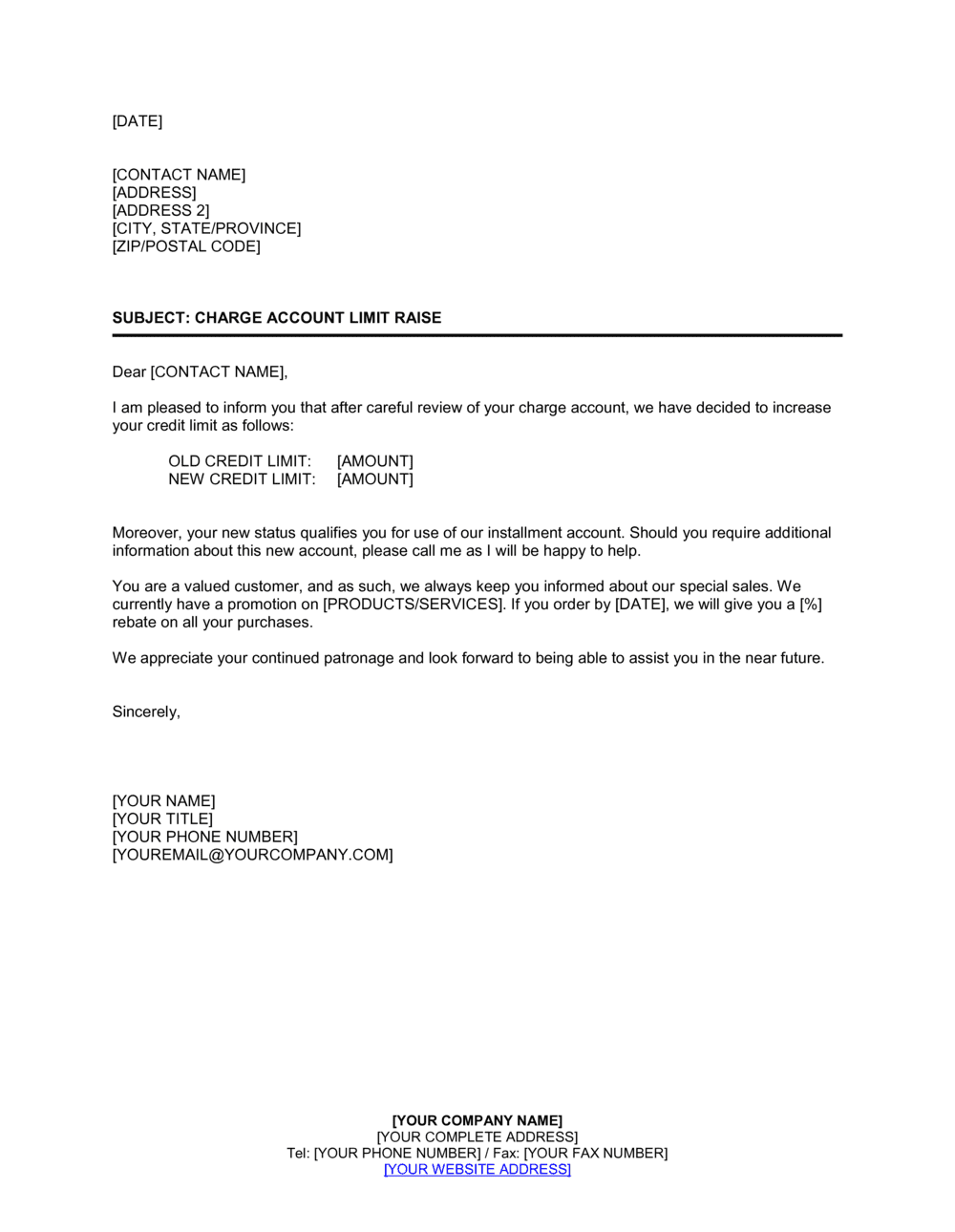

❌ Omitting the previous credit limit

Why it matters: Without the old figure, the customer cannot verify the change against their own records, and any discrepancy between your system and theirs goes undetected until a declined transaction surfaces it.

Fix: Always state both the previous limit and the new limit with a clear 'increased from X to Y' construction so the change is unambiguous.